PeakOil is You

Crude oil prices: Energy Bubble?

Re: The great oil bubble has burst

![]() by Dreamtwister » Fri 08 Aug 2008, 01:47:21

by Dreamtwister » Fri 08 Aug 2008, 01:47:21

Don't get me wrong, I'm gobbling up this buying opportunity like there's no tomorrow. But it does beg the question "Which hedge funds (Yes, plural) are having the fire sale to stave off bankruptcy?"

The whole of human history is a refutation by experiment of the concept of "moral world order". - Friedrich Nietzsche

-

Dreamtwister - Intermediate Crude

- Posts: 2529

- Joined: Mon 06 Feb 2006, 04:00:00

Re: The great oil bubble has burst

![]() by Novus » Fri 08 Aug 2008, 01:59:17

by Novus » Fri 08 Aug 2008, 01:59:17

$this->bbcode_second_pass_quote('Arsenal', 'H')a!! Problem solved. Time to go and buy a new SUV.

Arsenal

Arsenal

I am sure many will buy new SUVs. Cheap oil is a self correcting issue that will lead to more expensive oil in the next cycle.

-

Novus - Intermediate Crude

- Posts: 2450

- Joined: Tue 21 Jun 2005, 03:00:00

Re: The great oil bubble has burst

![]() by Micki » Fri 08 Aug 2008, 02:34:07

by Micki » Fri 08 Aug 2008, 02:34:07

Did they just rehash an article from 2006?

Sorry, I just have heard this news so many times the last few years. I am sure one of these times they'll get it right.

Sorry, I just have heard this news so many times the last few years. I am sure one of these times they'll get it right.

- Micki

Re: The great oil bubble has burst

![]() by TreebeardsUncle » Fri 08 Aug 2008, 03:03:15

by TreebeardsUncle » Fri 08 Aug 2008, 03:03:15

Well, when talking about global warming, oil price rises, and housing price drops words such as may, might, can, and could (subjunctive mood) is used. TPTB demand the following that global warming is not considered to be a problem, housing prices go up, and oil prices go down. Physical and economic realities will overwhelm official fantasies that most people buy into and present good buying opportunities. Note it is premature to buy into oil. Wait until it drops below 100 in the second week of October.

Lates.

g

Lates.

g

- TreebeardsUncle

- Tar Sands

- Posts: 683

- Joined: Thu 15 Jun 2006, 03:00:00

Re: The great oil bubble has burst

![]() by Carlhole » Fri 08 Aug 2008, 05:22:29

by Carlhole » Fri 08 Aug 2008, 05:22:29

$this->bbcode_second_pass_quote('Graeme', '[')b]The great oil bubble has burst

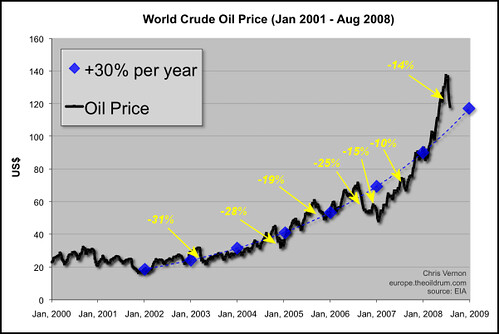

If the trend continues into September at anything like the same rate of descent, most of the inflationary spike of the past 12 months will miraculously have been sliced away. This is a dramatic reversal, and it is worth trying to work out why it is happening and what it means.

If the trend continues into September at anything like the same rate of descent, most of the inflationary spike of the past 12 months will miraculously have been sliced away. This is a dramatic reversal, and it is worth trying to work out why it is happening and what it means.

Jerome a Paris has got the best reply to this:

Countdown to $200 oil (10) - oil at $120!!

[align=center]

[/align]

[/align]$this->bbcode_second_pass_quote('', 'O')ne point that needs to be made again is that demand destruction in the US (or even in Europe, where it is hapoening too) is not enough on its own to bring prices down, because it needs to be larger than the supply growth in the rest of the world to limit the requirement for further demand destruction and price rises, given that production is still largely stagnant. And the problem is that demand is not growing just in China and India, thanks to rapid growth, it is also growing massively in oil producing countries themselves (Saudi Arabia, Iran, Russia, Venezuela), which often subsidize gas and which can afford it given that they have a natural hedge against (the subsidy gets bigger when oil prices are higher, ie when their own income is bigger, and the income growth is larger than the subsidy growth for those that export any volumes). In fact, most of the demand destruction happens in price sensitive places, like the poorest oil-importing countries (but they weren't burning much of it anyway), and the rich world (which can still afford oil, but consumes lots of it). But we can't be sure it happens fast enough to actually cause prices to go down because of what's going on in the rest of the world.

Anything that encourages demand reduction elsewhere (like lower subsidies) helps to bring prices down, but it's by no means obvious that we've reached price levels that are sufficient to cause overall demand stagnation in the face of flat or quasi-flat production. Oil producers have little or no incentive to boost their production if they expect prices to keep on creeping up (and they can help that trend by, precisely, investing less), and it's not clear what substitutes are available in any meaningful volumes.

So, at this point, I'm still happy to continue my "Countdown to $200 oil series" and see no reason why the recent lull in prices would be a sign of a serious trend change in the market.

Just from experience, looking at the chart above, it seems almost classical that we will see prices fall perhaps a bit more and then the upward trend will resume - but more slowly. In other words, the chart's future shape, by my guess, will look similar to the famous long-term oil production chart - which is sensible because no economics could withstand the exponential patterns exhibited.

- Carlhole

Re: The great oil bubble has burst

![]() by ROCKMAN » Fri 08 Aug 2008, 08:32:13

by ROCKMAN » Fri 08 Aug 2008, 08:32:13

I agree Carl. I don't follow daly or even weekly trends. Average MONTHYLY oil prices have risen for the last 7 months including July. Aug may be another matter. I'm an even bigger beleiver in the 6 month running average.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: The great oil bubble has burst

![]() by jlw61 » Fri 08 Aug 2008, 08:53:25

by jlw61 » Fri 08 Aug 2008, 08:53:25

Use this bursting bubble, and the stupidity it will bring, to your advantage. It was a good fire drill, and I've identified some definite weaknesses in my situation. Use this gift of time to identify and fix the perceived problems in your situation.

When somebody makes a statement you don't understand, don't tell him he's crazy. Ask him what he means. -- Otto Harkaman, Space Viking

-

jlw61 - Tar Sands

- Posts: 623

- Joined: Mon 03 Sep 2007, 03:00:00

- Location: Sunny Virginia, USA

Re: The great oil bubble has burst

![]() by Nickel » Fri 08 Aug 2008, 08:57:46

by Nickel » Fri 08 Aug 2008, 08:57:46

$this->bbcode_second_pass_quote('Concerned', 'R')emember in 2007 when people were wondering if we would BREAK through $100 BBL and now oil is "falling" to $118

Please reality check

Please reality check

Exactly.

-

Nickel - Heavy Crude

- Posts: 1927

- Joined: Tue 26 Jun 2007, 03:00:00

- Location: The Canada of America

That being said, there's a pretty big lag between short and long run elasticity, and I think the recent drop in demand and price has to do w/ long run elasticity that some were not counting on, or at least were speculating wouldn't happen.

That being said, there's a pretty big lag between short and long run elasticity, and I think the recent drop in demand and price has to do w/ long run elasticity that some were not counting on, or at least were speculating wouldn't happen.