$this->bbcode_second_pass_quote('bantri', 'T')o my current knowledge there´s none.

(just sharing a little 2+2=4 here:)

Just assume that separate areas of knowledge (financial, physical and energy related, in this case) connect at some point, and keep researching.

PeakOil is You

M. King Hubbert on

Re: How Reliable is the Hubbert Linearization Method?

![]() by khebab » Mon 09 Jan 2006, 13:11:12

by khebab » Mon 09 Jan 2006, 13:11:12

Thanks for the hints, I know that P/Q vs Q have been used aslo for population study. By the way, do you have a link for the first image you posted before.

$this->bbcode_second_pass_quote('bantri', 'E')xtra Hint:

The simulation using the sum of a hubbert curve and a constant amplitude cosine wave is useful to reach the conclusion that the linearization process narrows along time, but, when comparing with real models, it´s possible to conclude that this simulation doesn´t narrow as fast as the real ones.

i suggest a simulation using a DAMPED cosine wave, where it´s possible to adjust the damping factor to fit the curve better for comparison with true and real measurements (like Norway´s) without "human adjusted" factors.

more on this later....

Ok but it seems that the damping occurs naturally in P/Q because of the division by an increasing Q. I'm not sure I fully understand your comment.

______________________________________

http://GraphOilogy.blogspot.com

http://GraphOilogy.blogspot.com

- khebab

- Tar Sands

- Posts: 899

- Joined: Mon 27 Sep 2004, 03:00:00

- Location: Canada

Re: How Reliable is the Hubbert Linearization Method?

![]() by khebab » Mon 09 Jan 2006, 13:23:30

by khebab » Mon 09 Jan 2006, 13:23:30

$this->bbcode_second_pass_quote('Raminagrobis', 'b')ut one could object than you take as guaranted that production is generally hubbert-shaped, with some random variations around the base hubbert curve.

Yes it is the main assumption here.

$this->bbcode_second_pass_quote('Raminagrobis', 'T')here are countries where production is not Hubbert-shaped at all, for one of the following reasons :

# Production quotas (opec countries)

# disruption by war, embargo (Iraq), political collapse (FSU)

# several distinct production zones with large time lag, then production can be modelled as the sum of two or more hubbert cycles.

# production is constrainbed by pipeline capacity (Chad, Ecuador...).

Agreed, production modeling is really difficult for some countries especially when production is immature and the YTF is still important (ex: Nigeria) with possibly multiple Hubbert cycles involved.

$this->bbcode_second_pass_quote('Raminagrobis', 'N')ow, according to your results, if the production is "free" (no constraint => hubbert shape), we can have a reasonnably good estimation of URR even with only the 20% first percents of it gone. Then perharps we could get some rough estimation of Middle East's ultimate using figures up to 1980, before the quota were established ?

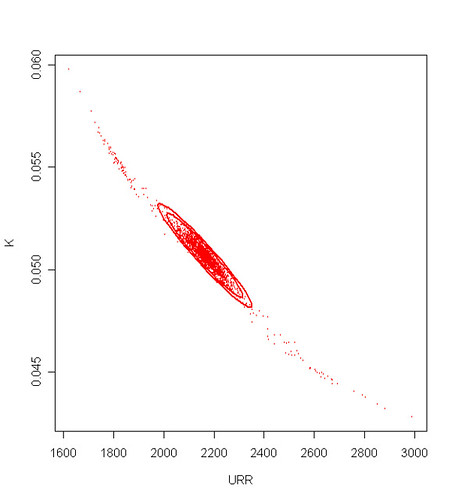

hmm... the confidence level at 20% of Qinf is rather low (~20%).

$this->bbcode_second_pass_quote('Raminagrobis', 'W')here could I find historical figures excludin refinery gain? It would be even better to have a split into crude, NGL's, and non-conventionnal production.

______________________________________

http://GraphOilogy.blogspot.com

http://GraphOilogy.blogspot.com

) has a bootstrap library called 'boot' that implements almost all the standard techniques. I won't go into the details of the Bootstrap theory, a lot of details about the techniques and the R language implementation used in this post can be found in the following document:

) has a bootstrap library called 'boot' that implements almost all the standard techniques. I won't go into the details of the Bootstrap theory, a lot of details about the techniques and the R language implementation used in this post can be found in the following document:

[/align]

[/align]

[/align]

[/align] [/align]

[/align]

[/align]

[/align]

{kind=link}

{kind=link}

{kind=link}