This is what I woke up to over my bowl of gruel (poached eggs on sourdough toast)

Australian CEOs gloomy about 2016 as world drowns in $200 trillion in debt

$this->bbcode_second_pass_quote('', 'T')he world is burdened by $200 trillion in debt that won't get paid back and will ultimately destroy emerging market economies and global growth, according to ASX chief executive Elmer Funke Kupper.

Mr Funke Kupper's comments come as a new survey shows Australian CEOs are less optimistic about growth in the world economy, as well as their own company's ability to make money in the coming year

PeakOil is You

Has the Great Contraction Begun?

Re: Has the Great Contraction Begun?

![]() by Shaved Monkey » Tue 19 Jan 2016, 20:48:14

by Shaved Monkey » Tue 19 Jan 2016, 20:48:14

$this->bbcode_second_pass_quote('', '&')quot;I think the world is burdened with about 200 trillion dollars' worth of debt which is an amount of money that simply is not going to be paid back."

This was happening in an environment where there were "record levels of quantitative easing and record low interest rates".

"But one day that's going to unwind, and when it's going to unwind, I think we'll see some forces at work that could really damage some parts of the world, particularly emerging markets economies."

http://www.theage.com.au/business/200-t ... m9119.html

The suits can see it, but they cant think its forever,just a temporary blimp.

Im amazed its being reported in the daily paper its going to scare the horses.

Ready to turn Zombies into WWOOFers

-

Shaved Monkey - Intermediate Crude

- Posts: 2578

- Joined: Wed 30 Mar 2011, 01:43:28

Re: Has the Great Contraction Begun?

![]() by MonteQuest » Tue 19 Jan 2016, 21:39:32

by MonteQuest » Tue 19 Jan 2016, 21:39:32

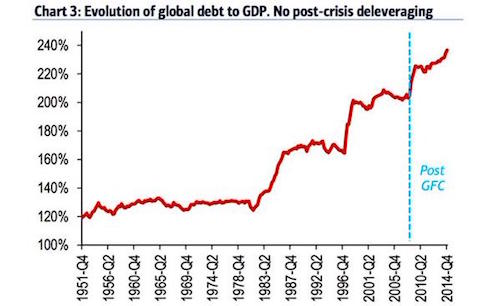

$this->bbcode_second_pass_quote('MonteQuest', 'I') think the real contraction started in the early 70's with we went off the gold standard and the first oil shocks occurred. Since that time, GDP has only grown due to increased debt. Now, more debt doesn't grow GDP, it hinders it.

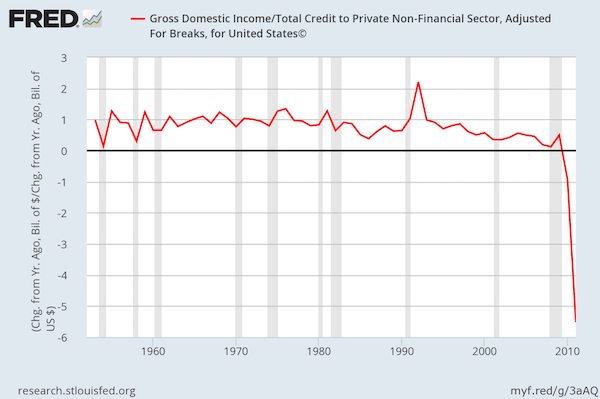

This is the wealth “illusion” I mentioned. We have been addicted to borrowing money, spending it, and passing it off as growth. This chart shows marginal debt, or, in other words, the productivity/growth gained from each additional dollar of debt. This graph shows private non-financial debt only.

The "illusion" has been with us for a while. It's now at 313% of GDP.

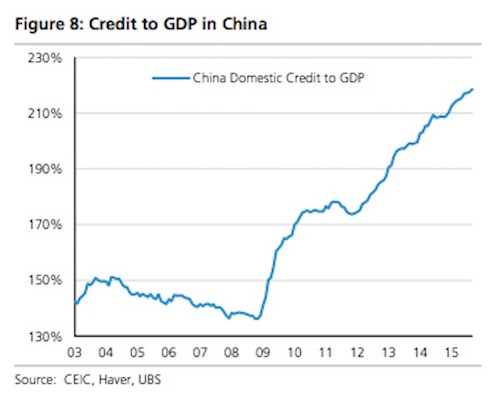

China came to the game a little later.

Save the banks and the rich at the cost of the poor. Right, Pops?

BTW, this is what is known as a Ponzi scheme.

Last edited by MonteQuest on Tue 19 Jan 2016, 22:02:52, edited 1 time in total.

A Saudi saying, "My father rode a camel. I drive a car. My son flies a jet-plane. His son will ride a camel."

-

MonteQuest - Expert

- Posts: 16593

- Joined: Mon 06 Sep 2004, 03:00:00

- Location: Westboro, MO

Re: Has the Great Contraction Begun?

![]() by MonteQuest » Tue 19 Jan 2016, 21:50:04

by MonteQuest » Tue 19 Jan 2016, 21:50:04

It is utterly impossible, as this country has demonstrated again and again, for the rich to save as much as they have been trying to save, and save anything that is worth saving. They can save idle factories and useless railroad coaches; they can save empty office buildings and closed banks; they can save paper evidences of foreign loans; but as a class they cannot save anything that is worth saving, above and beyond the amount that is made profitable by the increase of consumer buying.

It is for the interests of the well to do – to protect them from the results of their own folly – that we should take from them a sufficient amount of their surplus to enable consumers to consume and business to operate at a profit. This is not “soaking the rich”; it is saving the rich. Incidentally, it is the only way to assure them the serenity and security which they do not have at the present moment.-- Marriner Eccles, chairman of the Federal Reserve under FDR.

This is why the growing income in equality is such a threat and why the rich abhor any "socialist" measures to rein it in.

It is for the interests of the well to do – to protect them from the results of their own folly – that we should take from them a sufficient amount of their surplus to enable consumers to consume and business to operate at a profit. This is not “soaking the rich”; it is saving the rich. Incidentally, it is the only way to assure them the serenity and security which they do not have at the present moment.-- Marriner Eccles, chairman of the Federal Reserve under FDR.

This is why the growing income in equality is such a threat and why the rich abhor any "socialist" measures to rein it in.

A Saudi saying, "My father rode a camel. I drive a car. My son flies a jet-plane. His son will ride a camel."

-

MonteQuest - Expert

- Posts: 16593

- Joined: Mon 06 Sep 2004, 03:00:00

- Location: Westboro, MO

Re: Has the Great Contraction Begun?

![]() by Pops » Wed 20 Jan 2016, 10:18:43

by Pops » Wed 20 Jan 2016, 10:18:43

$this->bbcode_second_pass_quote('MonteQuest', 'I')'ve already explained this several times.

No, you just keep saying 'banks don't lend out reserves'

Of course they don't 'lend out' reserves Monte — they are reserves.

Reserves are not lent — they are leveraged — 10 to 1

Required reserves already have deposits attached, the $2.5T excess reserves are sitting there waiting for a loan to be made as soon as interest rises above the Fed's new interest rate.

Basically an inflation time bomb waiting to go off.

From the Minneapolis Fed

$this->bbcode_second_pass_quote('', 'B')anks in the United States have the potential to increase liquidity suddenly and significantly—from $12 trillion to $36 trillion in currency and easily accessed deposits—and could thereby cause sudden inflation. This is possible because the nation’s fractional banking system allows banks to convert excess reserves held at the Federal Reserve into bank loans at about a 10-to-1 ratio. ..

Banks in the United States currently hold $2.4 trillion in excess reserves: deposits by banks at the Federal Reserve over and above what they are legally required to hold to back their checkable deposits (and a small amount of other types of bank accounts). Before the 2008 financial crisis, this amount was essentially zero. To put this number in perspective, the monetary base of the United States (the sum of all currency outside the Federal Reserve System plus both required and excess reserve deposits by banks at the Fed) is $4 trillion. So, 60 percent of the entire monetary base is now in the form of excess reserves compared to roughly 0 percent precrisis....

Bank actions alone could cause a large increase in liquidity (when banks hold substantial excess reserves) because of the nation’s fractional reserve banking system. Since each dollar of bank deposit requires approximately only 10 cents of required reserves at the Fed, then each dollar of excess reserves can be converted by banks into 10 dollars of deposits. That is, for every dollar in excess reserves, a bank can lend 10 dollars to businesses or households and still meet its required reserve ratio. And since a bank’s loan simply increases the dollar amount in the borrower’s account at that bank, these new loans are part of the economy’s total stock of liquidity. Thus, if every dollar of excess reserves were converted into new loans at a ratio of 10 to one, the $2.4 trillion in excess reserves would become $24 trillion in new loans, and M2 liquidity would rise from $12 trillion to $36 trillion, a tripling of M2.

Lots more ...

The public justification may have been to "increase liquidity" and "help homeowners" by that went out the window as soon as congress signed off. What happened in reality was lining the shareholders pockets, making too-big-to-fail even bigger, of course no homeowners helped (LOL), and leaving a huge potential bubble of loans poised to inflate in a sort of reverse bank run.

Oh, and fueling mergers that make too-big-to-fail even bigger.

Here is a great article by Matt Taibbi from 2013

$this->bbcode_second_pass_quote('', 'P')ut another way, banks are getting paid about as much every year for not lending money as 1 million Americans received for mortgage modifications and other housing aid in the whole of the past four years...

Moreover, instead of using the bailout money as promised – to jump-start the economy – Wall Street used the funds to make the economy more dangerous. From the start, taxpayer money was used to subsidize a string of finance mergers, from the Chase-Bear Stearns deal to the Wells FargoWachovia merger to Bank of America's acquisition of Merrill Lynch. Aided by bailout funds, being Too Big to Fail was suddenly Too Good to Pass Up.

The legitimate object of government, is to do for a community of people, whatever they need to have done, but can not do, at all, or can not, so well do, for themselves -- in their separate, and individual capacities.

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

Thanks!

Thanks!