Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on August 6, 2014

Nearly 4% of the world’s oil supply is offline due to wars, unrest, sanction

The world’s oil prices have stayed high since 2010 — bouncing around $100 per barrel— for two basic reasons. Oil demand keeps rising, and production is struggling to keep up.

But why is production struggling to keep up? One big factor has been geopolitical conflict. Wars, unrest, and sabotage have increasingly plagued oil producers like Iraq, Libya, and Syria since 2011. The US and EU sanctions on Iran’s oil industry have also removed a lot of oil from global markets.

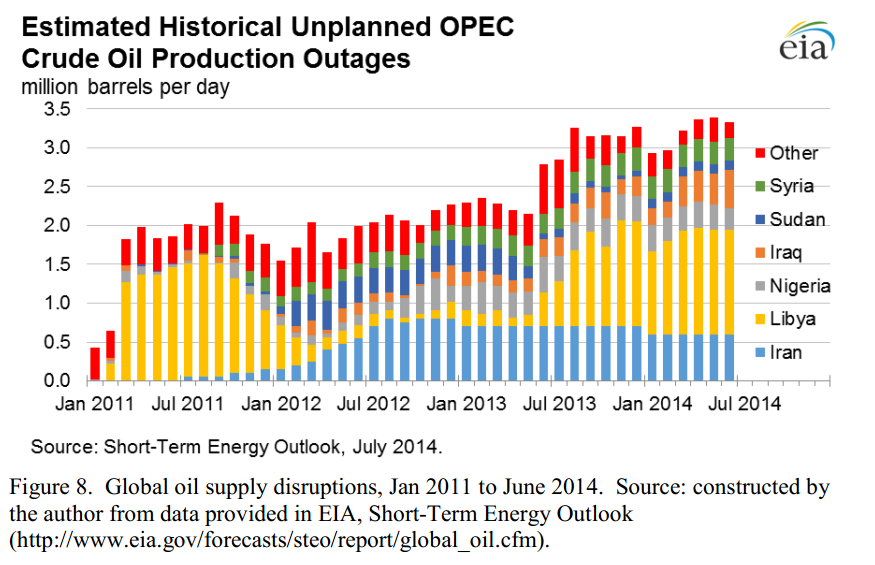

All told, some 3.3 million barrels of oil per day — equivalent to nearly 4 percent of global supply — are currently offline due to “unplanned outages”:

Hamilton, 2014

The chart above comes from a new paper (pdf) by James Hamilton, an economist who studies oil at the University of California, San Diego. He argues that the oil markets have changed dramatically in recent years — and $100 per barrel oil is likely here to stay:

The big stories in the oil market, he says, are:

‘My conclusion is that hundred-dollar oil is here to stay’

1) World oil demand is now being driven by emerging economies. Wealthy countries — including Europe and the United States — have actually been cutting back on their oil use, thanks to improved fuel efficiency and reduced driving. But fast-growing countries like China and India are more than taking up the slack.

2) Most of the new oil since 2005 is lower-quality hydrocarbons. A smaller fraction of the “oil” being produced today is actually crude oil — which is arguably the most useful of all liquid fuels.

3) The fact that oil production has stagnated means higher prices. This one’s pretty obvious. If producers can’t keep up with soaring demand from countries like China, prices will rise.

4) Geopolitical disturbances are holding back production. See the chart above. This includes conflict and war in Syria, Iraq, and Libya. It also includes the effect of US and EU sanctions on Iran’s oil industry.

5) Many oil producers are bumping up against geological limitations. There’s some evidence that Saudi Arabia is having trouble increasing oil production, Hamilton notes. And private companies are investing more and more money but getting less and less oil. A lot of the easy-to-drill oil is already online — what’s left is the hard stuff.

One major exception here is the United States, which is producing more oil these days thanks to improved fracking and horizontal drilling techniques. (That US production has helped mitigate the effects of all those unplanned outages.) but there are lots of obstacles hindering the spread of those technologies elsewhere.

Add it all up, and you get pricey oil on the global markets. And Hamilton, for his part, is skeptical that these factors will go away anytime soon. Yes, peace might break out in Libya or Iraq — or a financial crisis might break out in China — and that would cause a dip in prices. But the dip would only be temporary, buying the world a few years’ of extra supply. “My conclusion,” he writes, “is that hundred-dollar oil is here to stay.”

Do other countries use fracking?

A few countries have been using fracking for some time — particularly Canada. But shale fracking hasn’t yet caught on anywhere the way it has in the United States.

Plenty of countries abroad have their own shale gas and shale oil resources. That includes China, which appears to have nearly twice as much shale gas underground as the United States does:

US Energy Information Administration

But fracking has been slow to spread overseas, for a variety of reasons. Some countries, like France and the Netherlands, have banned fracking for fear of water contamination. Others, like Austria, have such strict regulations that drilling is uneconomical.

Even countries in favor of fracking have seen sluggish progress, in part because working with shale can be extremely difficult and complicated. In Poland, there’s still plenty of work that has to be done to understand the region’s geology. And, in China, the spread of fracking has been hampered by a variety of factors — complex geology, a dearth of water supplies in key regions, and a burdensome layer of regulations that hamper innovation.

8 Comments on "Nearly 4% of the world’s oil supply is offline due to wars, unrest, sanction"

Plantagenet on Wed, 6th Aug 2014 6:40 pm

Hundred dollar oil may be here to stay someday, but it hasn’t happened yet. WTI Oil dropped again today to $96/bbl, marking a six month trend of declining oil prices.

Davy on Wed, 6th Aug 2014 6:58 pm

Plant, the world is nearing a time of extreme instability that makes predictions useless. Prices may nose dive and they may have to go up. The scenarios are all over the place. IMO we are going to see economic damage from this developing trade war that will cut growth and drop prices. The financial system is ready for a panic in my mind.

redpill on Wed, 6th Aug 2014 8:05 pm

“marking a six month trend of declining oil prices.”

While we are almost at a 6-month low, I fail to see the “trend” you speak of:

http://www.nasdaq.com/markets/crude-oil.aspx?timeframe=6m

“Hundred dollar oil may be here to stay someday, but it hasn’t happened yet.”

Well, let’s take a peak at the 5-year chart then:

http://www.nasdaq.com/markets/crude-oil.aspx?timeframe=5y

Well, I do see a trend in the 5-year. Perhaps this word does not mean what you think it means?

Craig Ruchman on Wed, 6th Aug 2014 9:22 pm

As an investor in stocks, I like to look at the long term and filter out the day to day noise. The 5 year chart shows WTI on an upward trend, so I am not swayed by a dip to $96.

Makati1 on Wed, 6th Aug 2014 9:29 pm

Need to take another 85% off-line to save the planet. Screw the cost of oil. The higher the cost, the less consumed. We can chose between oil and extinction. But then, some say we have already sealed our extinction. All we can do is moderate the time left. I follow that theory. Bring on $200 oil.

GregT on Wed, 6th Aug 2014 11:10 pm

“Bring on $200 oil.”

Maybe that is exactly what Washington is trying to accomplish in Ukraine. Cause a spike in energy prices, so US oil and gas companies can export to Europe, while at the same time ending BAU sooner than later.

Makati1 on Wed, 6th Aug 2014 11:14 pm

GregT, I don’t expect more than a trickle of US oil to ever be exported anywhere. Ditto for US natural gas. Anyone who listens to O’s BS deserves the consequences.

shortonoil on Fri, 8th Aug 2014 8:04 am

Here is a post that I put up at Peak Oil Barrel a couple of days ago, before it came up in the MSM yesterday.

Ron said,

“This could get really scary.”

If you plot the deaths reported since March it appears that this epidemic is progressing exponentially. If it continues on its present path, there will be over 2 million dead in 18 months. We expect that Nigerian production will be shut in within a year if things continue. The foreign work force now operating these fields will leave. The loss of 2 mb/d of this very high quality crude will have a major impact on the world’s economy. This would amount to 2.7% of the world’s supply.

http://www.thehillsgroup.org/