Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on July 15, 2015

The ‘Oil Supply Glut’ Appears To Be A Myth

Summary

- The media continues to report that the world is greatly oversupplied with oil and this continues to have a negative effect on oil prices.

- The EIA and IEA both appear to be underestimating worldwide demand for oil by nearly 2 million barrels per day.

- The EIA lacks reliable production figures for any state except for Alaska.

- The figure that the EIA adds to actual crude oil stocks before reporting has increased greatly in recent weeks.

- The oil price decline has led to cutbacks in capital spending, which is likely to exacerbate an oil supply shortage going forward.

For quite some time now, the media has been discussing the oil supply glut that has been blamed for pushing down the price of oil from its previous peak in the middle of last year. However, there is now an increasing amount of evidence that the extent of the supply glut has been overstated or may not even exist at all. If this is correct, then it will almost certainly prove bullish for oil prices going forward.

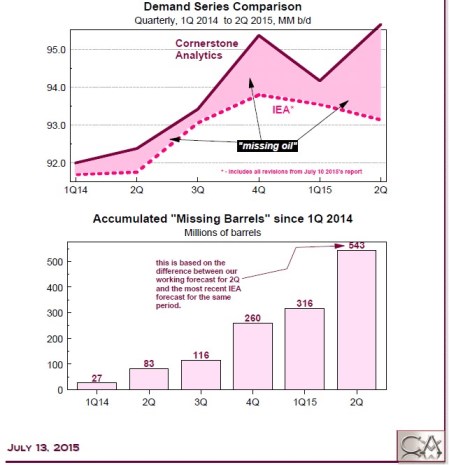

The numbers that support the presence of an oil supply glut in the United States and internationally largely come from two agencies – the Energy Information Administration and the International Energy Agency. However, there are other independent institutions that also track supply, demand, and production trends in the energy markets. One of these is Cornerstone Analytics, founded by Michael Rothman, former head of ISI’s integrated oil research division and International Investor’s top-rated Independent Energy Researcher since 2006. Over the past few years, this firm has published supply and demand figures for oil that directly contradict the official figures from the government agencies.

According to Leonard Brecken of OilPrice.com, the current production of oil worldwide is approximately 95 million barrels per day. There is little dispute about this figure as the IEA Oil Market Report stated that January 2015 worldwide production was approximately 94 million barrels per day. However, according to Cornerstone Research, worldwide demand for oil was in excess of 94 million barrels per day in the first quarter of 2015 and is more than 95.5 million barrels per day today. Furthermore, the firm also states that worldwide oil demand was in excess of 95 million barrels per day in the fourth quarter of 2014. These figures are consistently higher than IEA estimates.

Source: Cornerstone Analytics, OilPrice.com

In other words, if Cornerstone Analytics’ figures are correct, and there is reason to believe that they may be, then not only is there no global oil glut but in fact there appears to be a worldwide oil shortage.

One thing that is important to keep in mind to understand the rest of this article is that the production numbers provided by the Energy Information Administration are only estimates. The only numbers that are not estimates are the real-time production figures for Alaska. As such, there is no guarantee that these numbers are accurate. The Energy Information Administration provides information about the methodology that it uses to derive its production figures. In short, the agency relies on various reports that are provided by the states, which are oftentimes inaccurate, incomplete, and can take years to reconcile. Estimating oil demand is even more difficult as it requires analyzing consumer habits, the weather, and global GDP growth, among many other factors. As can be expected, these factors can be expected to result in numerous reporting errors.

On Tuesday, April 7, 2015, OilPrice.com reported that the Energy Information Administration revised downward its prediction for 2015 crude oil production growth to 550 thousand barrels per day from 700 thousand barrels per day. That is a decline of 21% from the previous estimate. It also revised downward its prediction for 2016 crude oil production growth to 80,000 barrels of oil per day from its previous level of 140,000 barrels per day. That is a 42% reduction compared to the previous estimate. This provides evidence that U.S. oil production will not be growing as quickly as many believed thus casting doubt upon the length of and extent of the oil supply glut.

Another very interesting event occurred at the end of May that highlights the problems with the official numbers by the Energy Information Administration. As OilPrice.com reports, for the week ended May 22, 2015, the EIA reported that oil production in the United States increased by approximately 3% compared to the previous week. This follows a nearly three-month period in which oil production remained relatively flat. Furthermore, at the time, rig counts had been declining since October. This makes such an increase in production rather unlikely as oil production typically cannot be increased that quickly and it most certainly cannot without the use of more rigs. Of this production increase, much of it was in the lower 48 states. During that week, Alaskan production increased by approximately 95,000 barrels per day. As already mentioned, Alaskan production numbers are reported in real-time are so are likely to be accurate. However, the remaining 205,000 barrels per day increase took place in the lower 48 states, where production figures are often based on inaccurate numbers, as already discussed. The way that the EIA accounted for this increased production is to increase the March baseline production number by 130,000 barrels per day and then state that production increased again by 75,000 barrels per day during the week of May 22. The agency provided no rationale for either of these numbers and, once again, rig counts were declining over the period. Some on this site and in the media have attributed the production increases in spite of rig count declines to the movement of drilling rigs from marginal production areas to “sweet spots,” where oil production is highest. While it is true that moving rigs to the areas of highest production could offset the production declines that would normally be expected with a declining rig count, it cannot account for all of the discrepancy. Furthermore, there is evidence that per well production in the “sweet spots” of the Bakken shale formation has been declining for quite some time.

“Sweet Spot” Bakken Shale Well Production in First 24 Hours – November 2013 to Today

Source: NDIC Daily Activity Report, OilPrice.com

Even if we accept that the EIA’s figures showing growing oil production are accurate, it has not been sufficient to meet the increased demand caused by the summer driving season. This is evident by the fact that despite the reported production increase, the nation’s commercial crude inventories declined by 2.8 million barrels during the week of May 22. In fact, the nation’s inventories of commercial crude oil began to decline during the week ended May 1, 2015, a trend which has continued through to today. Although the last two oil inventory reports do indeed show rising levels of crude oil in inventories, these inventories have not yet regained their previous levels. This also casts doubt on the various reports that state that the world has a two million barrel oversupply of oil.

Interestingly, one of the things that caused oil inventories to begin to climb again is that during the week of June 12, 2015, the lower 48 states managed to increase production by a remarkable 76,000 barrels per day. As already mentioned, the production figures for Alaska are likely reliable and that state saw its production decline by 61,000 barrels per day. These two figures combined result in an increase of 15,000 barrels per day or approximately 105,000 barrels per week. However, over the course of the next week, inventories declined by 4.9 million barrels of oil and then increased by 2.4 million barrels the following week.

The timing of these production increases has made Leonard Brecken very suspicious as they came at around the same time that inventory draws began. However, even more suspicious is that the “Miscellaneous to Balance” figure used in calculating inventory also increased sharply at around the same time. The Miscellaneous to Balance figure is simply an adjustment used by the EIA when calculating inventory, theoretically used to make crude oil inventories match with production, imports, crude runs, and crude oil demand. Essentially, this is a figure that is added to or subtracted from the actual amount of crude oil in the nation’s commercial inventories before the figures are reported. This chart, courtesy of Cornerstone Analytics, shows how this figure has varied over the past several months with positive numbers indicating that the EIA added barrels to the amount of crude oil actually contained in the inventories and negative numbers indicating the opposite.

Source: Cornerstone Analytics, OilPrice.com

According to Cornerstone Analytics, if the reported numbers were correct, then crude oil stocks should be thirty million barrels higher than they are just since April. As Leonard Brecken points out, this is roughly the entire amount of oversupply in the United States compared to the mean. In other words, this indicates that there is in fact no oil supply glut in the United States and if the earlier oil demand chart was accurate then there may in fact be an oil shortage worldwide.

Unfortunately for both oil companies and investors in the sector, the decline in oil prices caused by the reported glut has had very real consequences. Aside from the obvious declines in revenues, cash flows, and net income incurred by oil companies, the decline in oil prices has also caused major exploration and production companies to scale back on both exploration and capital spending programs. This will ultimately result in fewer oil fields being developed going forward along with the likelihood of eventual production declines as currently producing fields begin to produce lower quantities of oil. Ultimately, this could exacerbate the supply shortage that may already exist worldwide.

35 Comments on "The ‘Oil Supply Glut’ Appears To Be A Myth"

Nony on Wed, 15th Jul 2015 7:29 pm

I think trying to track the storage balances is a mug’s game. Obviously there will be times when supply is greater than demand and storage increases and the converse. But over time, production has to equal consumption.

Just having “more production than producers like” is not a glut. A glut is a temporary imbalance of supply versus consumption. It will result in an extreme contango structure and pressure on storage capacity. Instead of trying to look at every tank (and forgetting about crude tanks getting 10 year API inspections that can take them out of service for a year). What is easier is to just look at the PRICE of oil storage. It jumped in JAN-MAR to about 5 times normal. That was sign of a glut. It is now pretty close to normal. Also the extreme contango structure has gone away and we have a very small contango (not that much more than inflation…little bit…but not much).

Northwest Resident on Wed, 15th Jul 2015 7:31 pm

Plant, is this true? Have you been lying to us all along?

Nony on Wed, 15th Jul 2015 7:32 pm

The chart of IP decline (of Ron’s) got pretty much eviscerated by his FELLOW PEAKERS (but the better analysts amongst them). It lacks a zero reference, cherry picks the start time. Lacks the confidential wells. Etc. Etc. Also IP is not that great of a metric (first few months production means much more).

Nony on Wed, 15th Jul 2015 7:54 pm

Here is a chart of first few months of well production.

http://peakoilbarrel.com/the-eias-short-term-guessing-game/comment-page-1/#comment-526235

No obvious trend.

Nony on Wed, 15th Jul 2015 8:02 pm

Actually I just looked at the futures curves. Seems like the contango in WTI has increased lately. We’re over $4 (8%) for a one year out futures price change. I thought it had gone down to less than that a while ago. Not as bad as early in the year when it was double that, but still little more than it had been when oil was at 60. Need to sweat off some more shale producers.

We got mildly glutty again. But nothing like the start of the year.

Nony on Wed, 15th Jul 2015 8:06 pm

Here is a chart showing the average production of a 2015 well versus 2014, etc.

http://peakoilbarrel.com/the-eias-short-term-guessing-game/comment-page-1/#comment-526224

No significant change and really a slight improvement from a few years ago to now. Probably competing effects between

*drilling up the sweet spots

-moving to the fringe

-infilling (with some interference)

and

*longer laterals

*better completions (more sand and water)

*knowing the geology better

*improved skill of the operators

*improved gathering systems

*Increased drilling in sweet spots (HPB for fringe leases taken care of)

apneaman on Wed, 15th Jul 2015 8:30 pm

Nony marm is getting frantic again……worldview continues to crumble.

Plantagenet on Wed, 15th Jul 2015 9:20 pm

Anyone who believes the oil glut is a myth or the oll glut has just ended should buy oil futures betting on a higher oil price and you’ll make money as the price of oil goes up.

Of course, if the oil glut is real then you’ll lose all your money.

OK—anyone prepared to buy oil futures? nrodent? apey? Anyone else?

I thought not. Hah!

CHEERS!

Nony on Wed, 15th Jul 2015 9:39 pm

Plant:

1. A glut is a temporary imbalance. Not a low or high price itself. It is represented by a large contango structure in the futures curve.

2. A small contango structure is normal, non glut, given that we have a some Hotelling effect of oil depletion as well as the time value of money.

3. To trade on a glut (the contango trade), you can’t just buy futures. That is trading on the price itself. You have to physically take possession of oil, store it and SELL the futures contract.

4. Simply speculating on the futures themselves is a 50-50 bet (minus brokerage and margin costs), given markets are efficient and highly traded. And WTI definitely is.

5. Saying that the market view of oil price (now or future) is different from reality…and then trading on that is different than the idea of a glut (a temporary supply/demand mismatch). You can trade on the market being wrong (go long or short) regardless of any inventory crunches or the converse.

BobInget on Wed, 15th Jul 2015 11:33 pm

China reported ‘only a 7% growth rate”.

China’s reported consumption up 3% year over year. China, the world’s second-largest oil consumer, raised crude imports by nearly 10 percent last year, or an additional 530,000 bpd, largely to boost government and commercial reserves as oil companies took advantage of the more than 50 percent fall in global benchmark prices from mid-June. [O/CHINA1][O/R]

India reports 6.5% GR oil consumption 3.3%

n.reuters.com/article/2015/03/04/india-oil-demand-idINKBN0M01H620150304

None of these articles mention widely estimated military consumption of around a million barrels per day. Those are your ‘missing’

barrels. That oil was never imported.

In case you missed it Russia is also deeply involved in Ukraine. Tank diesel consumption

is measured in tons per mile;-)

Korea imports highest in 14 years.

http://www.bloomberg.com/news/articles/2015-06-15/south-korea-buys-most-crude-in-14-years-as-saudi-imports-jump

China continues gearing up to defend its little China Sea oil patch. No one seems to care.

Even the fact that we burned up 6+% more gasoline last week then a year ago makes not a wave.

BC on Thu, 16th Jul 2015 12:34 am

One glut that is not a myth is that there has been one person on this site saying for months that there is an oil glut.

It’s more like a glut of cheap junk credit to fund unprofitable extraction of shale at a price that is still too high to permit the global economy to avoid stagnation.

Northwest Resident on Thu, 16th Jul 2015 1:26 am

BC — That fact has been pointed out to the clueless Glutster several times, with no effect. The Glutster is illogical, obnoxious and asinine, persistently. Someday the Glutster will stop consistently, monotonously repeating the phrase “oil glut”, but not soon enough.

Plantagenet on Thu, 16th Jul 2015 1:30 am

Hi Nony

I’m glad you finally figured out what a glut is —congrats—- but why are you posting your simplistic definition of a glut here?

The definition of a glut has already been endlessly here…..

Cheers!

Plantagenet on Thu, 16th Jul 2015 1:32 am

@BC

Again, if you don’t think there is an oil glut, then go long on oil futures…..

Won’t do it? Then obviously you don’t believe yourself what you are saying.

Hahahahahahahahahahah!

Boat on Thu, 16th Jul 2015 2:44 am

The problem with going long on oil even when there is a glut. You don’t know what crazy Putin is going to do to disrupt the markets. You don’t know if Iran is a stable actor. The world is still to volatile and prices can turn on a dime through fear even if if there is a glut.

Davy on Thu, 16th Jul 2015 7:00 am

Gullible Bob said “China reported ‘only a 7% growth rate”. China’s reported consumption up 3% year over year.” Bob when are you going to get a grip that your China consumption engine is a paper dragon dissolving in the rain! It is a country of make believe economics.

China Defends Data: GDP Figures Are “Objective”, Reflect “Real Situation”

Early last month in, “China’s Deficient Deflator Math Is One More Reason To Distrust Data,” we highlighted an FT piece which suggested that thanks to a lack of “robust statistical systems,” Beijing may habitually overstate GDP during periods of falling commodity prices by failing to completely account for changes in import prices in the calculation of its GDP deflator.

http://www.zerohedge.com/news/2015-07-15/china-defends-data-gdp-figures-are-objective-reflect-real-situation

WSJ Notes “Chances That China’s Data Is Real Is Very Low” Then Promptly Scrubs It

Ironically, none other than the Chinese economic data aggregator and reporter, the NBS, essentially confirmed the data is fabricated when it said, and we quote:

CHINA’S GDP ‘NOT OVERESTIMATED’, NBS SHENG SAYS

Because there is nothing quite like an official denial to confirm what everyone has known for years. But that was not what caught our attention in the overnight data, and its broad coverage. What did was the original WSJ summary report on the Chinese data, which contained the following rare admission of just how rigged not only China’s stocks are, but its entire economic reporting:

http://www.zerohedge.com/news/2015-07-15/wsj-notes-chances-chinas-data-real-very-low-then-promptly-scrubs-it

BC on Thu, 16th Jul 2015 9:15 am

Plant, 😀

Actually, I expect a global recession and oil back into the $40s, even $30s, as historically a price of oil above $40 has reduced the 9-year rate of real GDP per capita to ~0% to negative.

The “glut” of unprofitable US and Canadian shale and tar is an unambiguous sign of Peak Oil.

US and world real final sales/GDP per capita averaging ~0% since 2007 is an unambiguous sign of LTG.

None of these coincident factors is incongruous to the Peak Oil narrative.

BC on Thu, 16th Jul 2015 9:21 am

China’s data are fiction. Period.

Labor productivity is no faster than 1%.

The labor force is contracting three years running.

Population is growing 0.5%.

Therefore, China’s potential real GDP per capita is less than 1% to 0% or negative.

And this is precisely the same trajectory for the US, EZ, and Japan.

Thus, 70-75% or more of global real GDP per capita is decelerating to ~0%, i.e., LTG or the end of growth of the Oil Age epoch.

It was a fabulous run of cheap energy-induced good times, but now it’s over. Period. Full stop. No need to turn out the lights when you leave the room.

“So it goes” . . .

penury on Thu, 16th Jul 2015 11:00 am

China lies about their economy? guess what? The U.S. lies, the E.U. lies (in fact it is official policy (see Mario Dragi)) Canada lies etc etc. Everyone trying to cover up the decline in the world GDP. There will continue to be an “oil glut” as the price people can afford to pay will continue to drop. The cost of production will continue to rise faster than the price of the product. IMHO the good times are over, and the decay while slow will continue.

Davy on Thu, 16th Jul 2015 11:58 am

Pen, agreed but China takes the lying to new level the thieves in the west could only dream of. China’s lying is a lying about lying. It pervades the society in the realm of business. Surprisingly at a family and individual level the Chinese are quite honest.

apneaman on Thu, 16th Jul 2015 3:12 pm

Seems like the airline industry is producing a positive feedback loop (climate) and is also an energy Red Queen. Keep flying those friendly skies apes.

Climate Change Brings Ill Winds for Airline Industry

“LONDON—Global warming may already be taking its toll of air miles. As jet planes burn fuel and release carbon dioxide, the atmosphere warms and causes head winds to build up. Tail winds do too, but round trip journey times are nevertheless creeping up—and so are fuel costs.

A team of US scientists say the cumulative effect of the longer flight times that they think may have resulted from climate variation would have added millions of dollars to airlines’ costs, and perhaps a billion gallons of extra fuel.”

http://www.truthdig.com/report/item/climate_change_brings_ill_winds_for_airline_industry_20150716

Long-haul flights are taking longer – and the effect is worse fuel consumption

“Calculations suggest that even small increases in return-flight times caused by changes in wind speed and direction could have major implications for increased fuel consumption by the airline industry, which already accounts for about 3.5 per cent of greenhouse gas emissions.

The researchers believe that the effect may be the result of rising global temperatures and have warned that longer aircraft flights will lead to more fuel being used, more carbon dioxide being emitted and more global warming in a “feedback” that could accelerate climate change.”

http://www.independent.co.uk/news/science/longhaul-flights-are-taking-longer–and-the-effect-is-worse-fuel-consumption-10385952.html

Boat on Thu, 16th Jul 2015 4:18 pm

penury… Everyone trying to cover up the decline in the world GDP. There will continue to be an “oil glut” as the price people can afford to pay will continue to drop

Yet another conspiracy theory. As the price of gasoline drops you can buy more of the same product for less money. So how do people decide to consume less if the price is cheaper. Check your incense, it may be opium.

shortonoil on Fri, 17th Jul 2015 5:50 am

“Yet another conspiracy theory.”

It was definitely a conspiracy that the petroleum industry continually extracted the best of the world’s reserves for the last 100 years; so that what now remains is almost not worth taking out of the ground. No doubt about it, they all got together each year, and decided to only take the best.

The price of oil is going down because the value of oil is going down. What remains is almost not worth extracting. As long as there are people who want to focus on barrels (as something that Nature made all equivalent) like She makes all things exactly equivalent, you will be left scratching your head as to why prices are declining. The oil age ends when the rest of the world’s 4,200 Gb of resource is not worth pumping. That is, when it is not worth as much to the economy as what it will cost the producers to produce it. It is called depletion, and seems to be an incompressible concept to most people. But, don’t worry about it; Nature could care less about what people are capable of understanding. Regardless, the world’s oil supply will continue to deplete until there is nothing left but black goo that no one will want!

http://www.thehillsgroup.org/

Boat on Fri, 17th Jul 2015 6:53 am

Short,

Omen is building a 750 acre solar plant to create steam to remove thick oil from their field. They now use Nat gas to do the same thing. This will allow them to sell and use more nat for more productive uses at a cheaper price. Now how is this oil any different than the oil that hits the market now. Your claim that the value is going down dosent compute as long as they can acomplish production and make money at the market price. Seems to me they have figured out a way to add value to their oil.

Davy on Fri, 17th Jul 2015 8:04 am

Come on Boat do the math. How much did the 750 acres solar cost? I am doing an off the top of my head here. Ivanpah Solar Electric Generating System in California cost $2.2BIL for 3500 acres. This means they are spending up front $400BIL or so to be used through solar to extract heavy oil. I don’t have any details on this project I am only dealing with your comment. Boat you act like there is no cost to this change. Think before you type. You are a nice guy and contribute good stuff but this is “what?”

http://www.gizmag.com/ivanpah-fully-operational/30862/

Boat, what is this? “This will allow them to sell and use more nat for more productive uses at a cheaper price.” Why does a changeover to solar make nat gas cheaper for other uses? Why would it be more productive? Boat, this heavy oil you are referencing is still heavy oil. Heavy oil is more expensive to produce than light sweet crude. What is so hard to understand about that?

Boat said “Your claim that the value is going down doesn’t compute as long as they can accomplish production and make money at the market price.” Boat if a resource is more expensive to extract its energy value is less period. There is no doubt about that. That is part of the laws of nature and non-disputable. Market value for the producer is less. The consumer does not care.

Energy value is different than economic value but they are not exclusive. Both dwell together in our system at different levels. It does not matter one iota about what people pay for crude in an energy value sense because all crudes have a quality per energy value. In a market sense if a customer is willing to pay more because he needs heavy oil for some reason that is an individual difference. Heavy oil’s value has changed per the consumer because of its utilitarian quality. That situation does not happen with oil because oil has a commodity spread in an international market.

In a Market POV is a producer better off selling easy to produce light sweet crude at the same price as harder to produce heavy crude? Yes. The consumer does not care if both crudes become the equivalent in the end product. The producer cares and the economic system cares in a macro sense because more resources are available for other uses. Market value is a whole other animal for a different discussion. The economics of the market place can be divorced for the macro realities of resource depletion and energy value but only so long and only to a point at the system level

Boat on Fri, 17th Jul 2015 8:42 am

Davy. I don’t live in Omen. I wasn’t asked to do the calculations. I would just hazard a guess they did and came up with a way for the sun to water to steam and do that cheaper than using Nat Gas to do the same thing. If it was more expensive to use solar, why would they do that?http://www.forbes.com/sites/christopherhelman/2015/07/08/oil-giant-to-build-worlds-largest-solar-project/

Nony on Fri, 17th Jul 2015 10:16 am

Brent is not in a “glut” (a temporary excess of supply over demand). It’s just a market view that oil will be cheap for a long time. See the second comment and chart in the attached:

https://twitter.com/gst_economists/status/622014079008415744

WTI is a little glutty, but that has to do with the export restrictions isolating the market and then the time required to “turn off” shale.

Ian Cooper on Fri, 17th Jul 2015 10:22 am

Take cover folks, Planty’s brain is about to explode.

Nony on Fri, 17th Jul 2015 10:44 am

We’ve left Hamilton’s “hundred dollars here to stay”* and gone to some sort of “50s-60s here to stay” world. Or at least that is the betting line.

*The futures curve never believed in Hamilton’s hundred dollars to stay since it was heavily backwarded when oil was 100+. But Hamilton ignores classical micro and Bayesian insights.

shortonoil on Fri, 17th Jul 2015 11:54 am

“The consumer does not care if both crudes become the equivalent in the end product. The producer cares and the economic system cares in a macro sense because more resources are available for other uses.”

In our report “Depletion: A determination for the world’s petroleum reserve” we demonstrate that it takes 28% more energy to refine Mayan API 21° than it does conventional (API 37.5°). That is why heavy crude is heavily discounted. It is also why the world will never run on heavy crude. The percentage of its energy content delivered to the economy is too small to power that economy. Only oil that lies in the 30 to 45° API range can supply a net positive amount of energy. Extraction of non conventional relies on the energy supplied by conventional to support its production. Once conventional is gone, non conventional will become unprofitable to produce. The barrels produced concept, rather than the energy supplied concept has disguised the true depletion state of the world’s reserves.

http://www.thehillsgroup.org/

Nony on Fri, 17th Jul 2015 12:08 pm

Nothing wrong with 47 API oil from the Eagle Ford. See sales prices here.

https://www.platts.com/IM.Platts.Content/ProductsServices/Products/crudeoilmktwire.pdf

And this is even with the headwinds of differentials created by the export restrictions.

GregT on Fri, 17th Jul 2015 12:36 pm

“Nothing wrong with 47 API oil from the Eagle Ford.”

Other than the annoying little fact that it costs more to produce than what the economy can afford. Other than that, it’s ‘mighty”!

http://www.reuters.com/article/2014/10/23/idUSL3N0SH5N220141023

BC on Fri, 17th Jul 2015 2:17 pm

@shortonoil: “The price of oil is going down because the value of oil is going down. What remains is almost not worth extracting. As long as there are people who want to focus on barrels (as something that Nature made all equivalent) like She makes all things exactly equivalent, you will be left scratching your head as to why prices are declining. The oil age ends when the rest of the world’s 4,200 Gb of resource is not worth pumping. That is, when it is not worth as much to the economy as what it will cost the producers to produce it. It is called depletion, and seems to be an incompressible concept to most people. But, don’t worry about it; Nature could care less about what people are capable of understanding. Regardless, the world’s oil supply will continue to deplete until there is nothing left but black goo that no one will want!”

Precisely! I estimate that fewer than 10% of the population ACTUALLY understands Peak Oil and its implications. Perhaps no more than 1% ACTUALLY understands net energy, exergy, entropy, and depletion per capita as it relates to the energy cost of energy extraction and the implications for LTG and the end of growth.

It should also be said that depletion per capita is occurring in the context of the economic and geopolitical implications of peak Anglo-American empire, “globalization”, and the end of growth of “trade” (parity for GDP PPP between the three major trading blocs).

But eCONomists, politicos, banksters, CEOs, and Establishment mass-media intellectuals are not paid to tells us the facts, let alone provide the facts within a realistic narrative that would permit the masses to respond intelligently in their collective interest.

Instead, it has been decided that we need to focus on guns, gay (not necessarily happy) marriage, abortion, angry, violent, genocidal, tribal desert sky gods, allowing prayer to those gods while teaching Creationism in public schools, Caitlyn Jenner’s dress size, and Kim Kardashian’s fat a$$.

https://www.youtube.com/watch?v=afam2nIae4o

https://www.youtube.com/watch?v=4naoVjdFxCA

The kids are alright, but they’re all insane . . . waiting for the (El Nino-induced) summer (or winter) rain.

Nony on Fri, 17th Jul 2015 2:17 pm

US rig count is down. Nothing like a drop from 60 to 50 to make people take things more seriously…

http://www.reuters.com/article/2015/07/17/energy-oil-rigs-baker-hughes-idUSL2N0ZX0TJ20150717

shortonoil on Fri, 17th Jul 2015 3:59 pm

@ BC

“It should also be said that depletion per capita is occurring”

That may be a very informative way of looking at it. When I get a chance I’ll run some numbers on it. Thanks for the suggestion.