Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on October 24, 2012

Shale Oil: The Latest Insights

The impact of unconventional fuels like shale oil on the global energy system is still an issue of great uncertainty. Not so much because of the size of the tank (the resource base), but due to the large physical effort necessary to obtain a sizeable supply of this type of fossil fuel. For instance, to exploit tight shale oil formations we need large capital expenditures to obtain relatively low flow rates from many horizontally drilled wells.

The developments of all things shale oil were discussed at a seminar organized by Allen & Overy and their Future Energy Strategies Group in London on 16 October, of which a summary and key take-away points can be found below the fold. With many thanks to both Allen & Overy and the speakers at this event for sharing their knowledge on these important developments in a public setting.

Key take-away points from speakers at Allen & Overy meeting:

- There is a large existing shale oil (and shale gas) resource base but whether the resources can be developed economically at sufficient scale in many countries is still an issue of uncertainty.

- Two promising shale oil plays outside of the US are the Vaca Muerta in Argentina and Bazhenov Shale which both have double digit figures of potentially recoverable resources, with large players like Chevron, Statoil etc. engaging in their development.

- The marginal cost to develop shale oil in the US is around 90 USD per barrel with average cost of most plays around 60 USD per barrel.

- The effects of the abundance of shale gas in the US, which sent natural gas prices plunging, is unlikely to be replicated in the oil market because of its different market structure (globally connected oil market versus fairly closed domestic gas market).

- The US may not produce as much natural gas as currently anticipated in the future, because the industry will be more motivated to drill for shale oil then shale gas, given the availability of drilling rigs, because it is more profitable.

- We already see a shift today from dry shale gas basins being drilled to shale oil basins being drilled, including those with associated gas.

- In the UK a report is about to be released by the British Geological Survey on shale gas resources and reserves. Of the studied basins, the most promising one is expected to be the Lancashire shale basin because geological studies indicate the reservoir to be more than a 1000 feet thick, as opposed to US based shale plays which are in exceptional cases up to a hundred feet in thickness.

- There is a wide spectrum of views on the potential for shale oil production in the United States, with the pessimistic end being a maximum of 1.8 million b/d (of which 0.9 million is already in production) from Corelabs, and the optimistic spectrum expecting 3 to 4 million b/d from shale oil in the longer run (2020s).

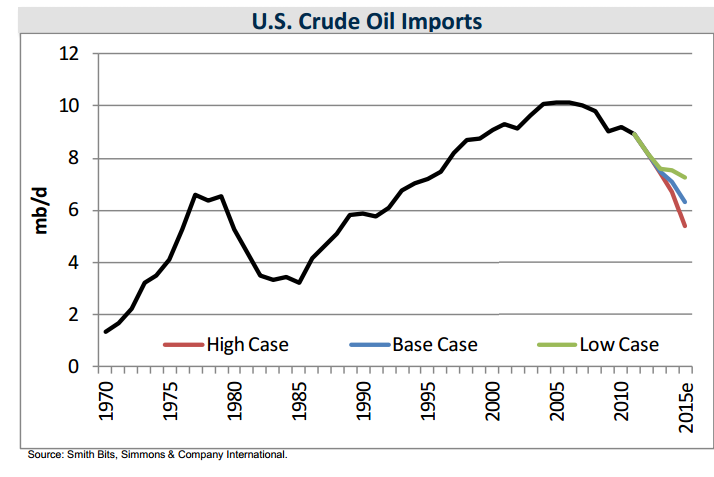

- If the more optimistic scenarios become reality the consequence would be a substantial decline in US oil imports, falling from 10 million b/d to 6 or 7 million b/d from 2008 to 2015.

Presentation (1) Justin Jacobs, Journalist or the Petroleum Economist

The first presentation about the big picture on shale oil was given by Justin Jacobs, journalist at the Petroleum Economist. He highlighted the importance of the US Eagle Ford & Bakken plays (approx. 27% and 63% of total shale oil supply), and emphasized large production expectations in the short term, with the EIA forecasting 1.5 million b/d shale oil production in 2013.

The Petroleum Economist recently made a first map of oil & gas unconventional resources across the world, to be found here, which Jacobs used to demonstrate the large number of unconventional resource plays in the world. He picked two of the most important shale oil plays to keep an eye on for the future:

- Vaca Muerta in Argentina, one of the largest discovered outside of the US. Its development cost is 250 billion USD over 10 years (with production potentially amounting to 200,000 b/d by 2020). The Repsol YPF section of the basin holds 22 billion barrels of oil equivalent of recoverable resources according to a Repsol YPF initiatied Ryder Scott assessment.At present development has been slowed by the nationalisation of Repsol YPF by the Argentinian government who took a majority share. Because the investment required is at minimum several billions YPF is trying to find big players who are willing to invest, including Chinese firms and Chevron.

- The Bazhenov Shale in Russia, has drawn interest from ExxonMobil and Statoil who have agreements in place for exploration and geological studies with Rosneft. The first exploratory drilling is to take place in 2013, and the licenses under investigation are expected to contain 15-20 billion barrels of resources. Total resources of the play have been estimated by BofA Merril Lynch at 60 to 140 billion, whereas Jacobs noted that these are wild early stage estimates, but that the shale play’s large size is beyond doubt. He cited Statoil estimating 2014 as an earliest possible production date, however, in his view attractive fiscal terms then currently offered by the Russian government would be necessary for development to take place. The play has also attracted attention from Lukoil, Ruspetro and TNK-BP.

The key issue according to Jacobs is whether the large existing resources can be developed economically at sufficient scale. The development requires thousands of wells due to the steep decline rate, which necessitates the on-going development of a new services sector in the majority of countries with plays. Similar to calculations by Rune Likvern as well as Arthur Berman and Lynn Pittinger published at the Oil Drum, he cited shale oil development to require high oil prices at 80-90+ USD per barrel.

Another relevant point brought forward was that the abundance of shale gas in the US sent natural gas prices plunging. The effect is unlikely to be replicated in the oil market. The reason is the difference in market structure. The oil market is fungible in its imports and exports and requires a high oil price to meet demand. In contrast the US gas market is fairly closed with production being sufficient to meet domestic demand.

Presentation (2) Richard Sarsfield-Hall, Pöyry Management Consulting

The second presentation was given by Richard Sarsfield-Hall from Pöyry Management Consulting, who posed the question “Is shale oil the brave new hydrocarbon frontier?” He reiterated important common points on the US gas market:

- The current low price level of 3 USD per MMBtu.

- The much higher marginal cost as opposed to current price levels.

- The oversupply of gas caused by a over-drilling given the cost-price imbalance.

- The growth of shale oil and shale gas requires more and more wells to be drilled to maintain and grow production (see Rune Likvern and Arthur Berman’s articles linked to above for more details).

The key issue presented by Sarsfield-Hall was about internal dynamics in the US market, as he sees a drilling competition occurring between the developments of dry shale gas reservoirs (Haynesville, Fayetteville) as opposed to shale oil reservoirs with associated natural gas (Eagle Ford) and shale gas reservoirs with associated liquids (Utica). This occurs because of more favourable economics for one versus the other in today’s market conditions (high oil price, low natural gas price in US). This is also possible because exactly the same type of rig is used for shale gas well drilling and shale oil well drilling. According to Sarsfield-Hall we already see this happening in today’s market, a point quantitatively further emphasised by the third speaker Tim Guiness, Founder Guinness Asset Management. He showed that well drilling has been overtly dropping in dry shale gas plays, while it has been constant or increasing in shale oil and shale oil with associated gas plays.

The implications of this competition are primarily affecting the expectations of institutes and market players, as the US may not produce as much natural gas as currently anticipated in the future, because the industry will be more motivated to drill for shale oil than shale gas. As Sarsfield-Hall puts it “There is a definite move of drilling from dry shale gas into shale oil with associated gas, the rush to shale oil potentially means insufficient shale gas delivered, which may result in higher gas prices and/or insufficient volumes to feed potential US LNG exports”. In addition Sarsfield-Hall showed EIA estimates which are primarily dry gas based increases, with little increase in associated gas from the expansion in shale oil. In terms of shale oil we are talking about a 10%-25% production share of total oil production in the coming decades according to EIA projections.

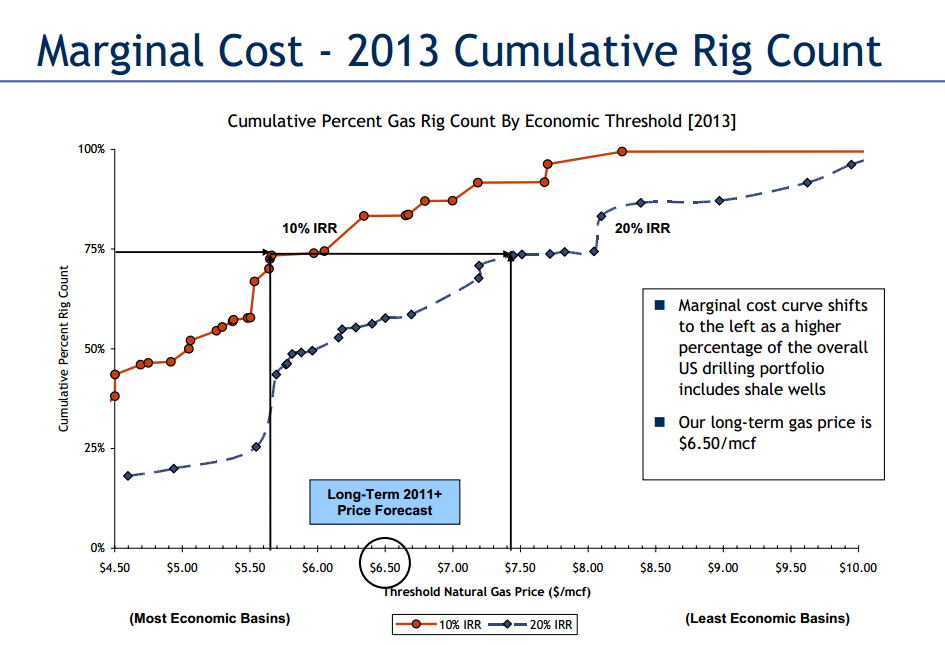

There were some numbers displayed. One key projection was for dry shale gas production, from a firm called ARC Financial, which showed decline expectation of 0.6 bcf/d up to 2013 from a current level of 23 bcf/d for dry shale gas production. Also some US associated gas production numbers were presented as per table 1, which is gas produced from oil fields (either free gas or dissolved in oil as a solution).

In using Cuadrilla’s scenario for production POYPRY found that UK natural gas imports could be reduced by 21% by 2020-2025 through shale gas developments. Their conclusions were that this could drive natural gas prices in the UK 4-6% lower which would save consumers 810 million pounds per annum. It would not in his view impact the UK achieving its 2020 renewable targets and alter its power generation at the volumes discussed.

Presentation (3) Tim Guinness, Founder Guinness Asset Management.

The last presentation was from an investors’ perspective, with Tim Guinness, chairman and founder of Guiness Asset management, and lead manager of their Global Energy Fund, presenting his views. He began by reiterating the reasons why the US has been able to develop their shale plays as:

- Improvement in ability to steer the drill bit.

- Development of ability to drill horizontally.

- Discovery of how to use hydraulic fracturing.

- US land and mineral rights.

- Relatively low population density.

- Adequate access to water.

- Existence of large successful oil & gas service industry and independent exploration & production sector.

He confirmed the switch from dry gas to shale oil/liquid rich shales with associated gas that is occurring, displaying rig figures per type of shale basin (predominantly shale oil, shale gas, and liquid rich with oil + associated gas). In addition he noted that the growth in gas supply has stopped in the US and is on a plateau, whereas oil production is growing substantially due to shale oil. He cited an onshore production estimate for December 2012 at 4.8 million barrels per day, which has been growing since 2008 after 38 years of decline since the peak in the 1970s, of which about 1.2 million b/d is from shale oil.

In his synthesis he compared three different estimates for shale oil production.

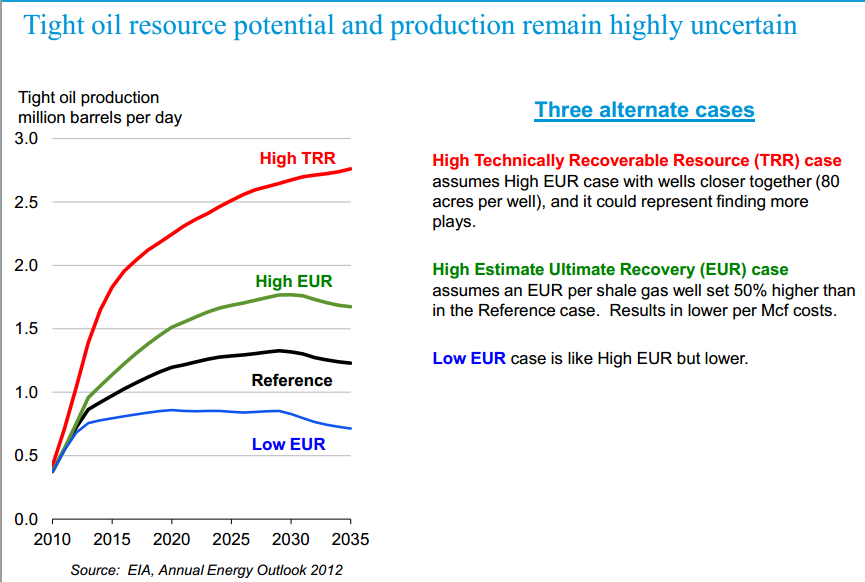

- Sandford Bernstein Oil Shale Forecasts, who expect 3 million b/d in 2016, maintained up to 2024, and peaking around 3.7 million b/d, which would come mainly from Bakken (1.5 million b.d), Missippi Lime (0.9 million b/d), and Eagle Ford (0.7 million b/d). With a cautionary note from Guinness that the forecast by now is 9 months out of date.

- Corelabs, who expect 1.8 million b/d at maximum from shale oil, of which 900.000 was already in production at the time of forecast (1.2 mb/d at present). In other words we can expect about a 600.000 b/d increase yet to come. The reason is that the sweet spots according to Corelabs are much smaller than people think (too much extrapolation of the good areas).

- Simmons & Co, who see US shale oil production growing to 1.9 mb/d in 3 years, and 8.3 million b/d of total oil production in 2015. The consequence of the Simmons & Co scenario would be for US oil imports to fall from 10 million b/d to 6-7 million b/d from 2008 to 2015. (see details in this presentation).

Table 2 – US oil production forecast for 2015 from Simmons & Co. Expectation based on 85 USD per barrel of oil and 3.50 USD per McF of natural gas.

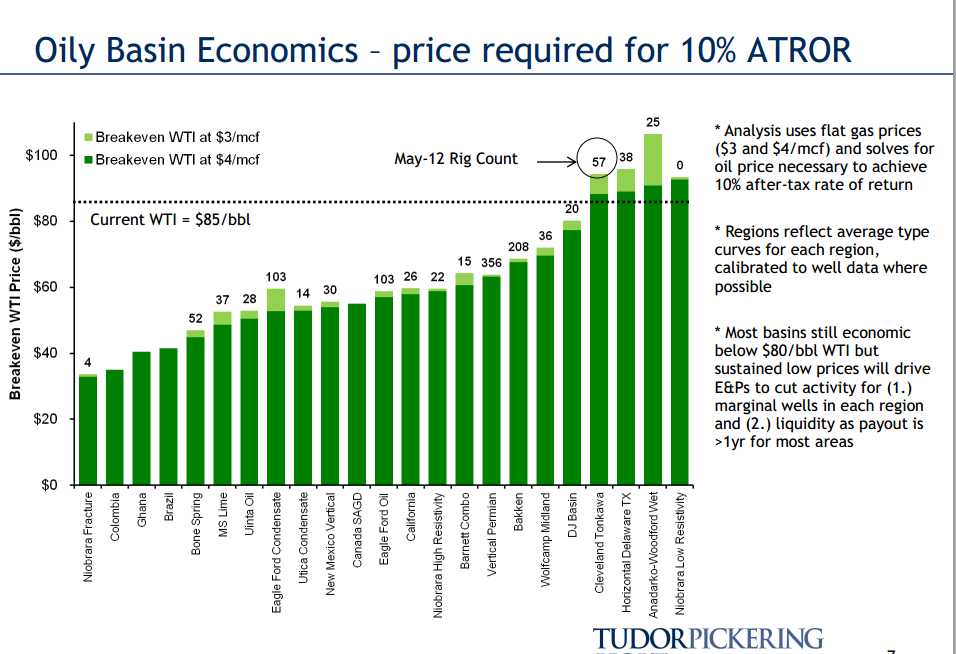

The final point Tim Guinness discussed was marginal cost, which according to Tudor Pickering for the majority of shale oil plays requires 60 USD, with the highest costing ones amounting to 85-90 USD (see figure 9 for details). He also cited Bernstein Energy research which shows cumulative resources of 30 billion barrels of US shale oil to be available at a cost below 150 USD per barrel. Some of the plays have a very low cost range, such as the Eagle Ford, where a figure of 40 USD per barrel was cited (Tudor Pickering shows this play around 60 USD).

Finally in his conclusion, as per recent Bernstein Energy research, Tim Guinness stated that shale oil is not a game changer for these specific reasons:

- Quality drilling locations are finite.

- Shale oil cost structure is high.

- Drilling efficiency gains harder to obtain than in gas shales.

- The industry structure (OPEC) is better for oil.

- Scale of US shale oil find relative to the oil market is small.

In Tim Guinness’ words: “It is akin to something like the discovery of the North Sea, Alaska or GOM. A useful addition but not a game changer, as the world needs 5 new North Seas every 20 years to provide enough oil to meet growing demand.”

17 Comments on "Shale Oil: The Latest Insights"

dsula on Wed, 24th Oct 2012 10:05 pm

Funny conclusion, shale oil is not a game changer. It already changed the game. The 2005 oil peak was surpassed, The US is on it’s way to pump 7MB/d, NG is cheapr than hell. Doom was postponed.

It’s not a game changer. LOL.

Beery on Wed, 24th Oct 2012 10:12 pm

In what way does a few more months of oil change the game? This is like your football team is down 30 points with a minute of game time left and you kick a field goal. There might be time on the clock, but let’s face it, the game’s over and you lose.

MrEnergyCzar on Thu, 25th Oct 2012 12:04 am

We need high EROEI transport fuels…shale isn’t it…

MrEnergyCzar

BillT on Thu, 25th Oct 2012 1:17 am

Well, dsula and SOS will not like the facts presented here. Too many bubbles burst and dreams wrecked. Too many ifs and maybes to make a real statement. A lot of dreams. And the article admits that the low hanging fruit is being pick now with only the scraps for future years after these companies have suckered in all the fools …er… investors, they can find who still have a few bucks to waste.

Bottom line, take out all the moonshine, and semi-fuels added recently to the charts and we are in a NET energy decline and always will be.

Why is there never an article that discusses NET energy from all of these finds, only sales hype and hope? Is it because it would blow the dream out of the water? EROEI is ALL that matters boys, dollars have nothing to do with it. You cannot bribe Mother Nature.

DMyers on Thu, 25th Oct 2012 1:49 am

As the article suggests, shale oil and gas are currently a low hanging fruit phenomenon. Unconventional oil has its harder and easier target zones. They’re taking these rich regions and projecting into the future. The trajectory will not meet the projections, as it descends rapidly. The difficulty of extraction will grow exponentially, as the project goes deeper into the shale substrate.

SOS on Thu, 25th Oct 2012 11:09 am

Please explain, outside of oppressive gov regulation that is, what makes oil and gas hard to get? it’s easy to get and Cheap to develop.

SOS on Thu, 25th Oct 2012 11:13 am

The reason nobody talks about net energy is because it is a false concept. Net energy is not driving this production, net profits are. Profits don’t have the luxeries given to EROEI. They are not subjective. They are real.

BillT on Thu, 25th Oct 2012 11:58 am

Hahahaha…SOS, you make my day.

You ignore EROEI because it is the killer of your ideas and dreams. Net energy is ALL that is important, not regulations or money. The government does not shut down a well because it is producing, the company does because the EROEI is not profitable. Huge profits were made when oil was $2 per barrel because the EROEI was high and oil was easy to get. Now EROEI is low and most sources are not profitable.

Blame who you want, but the age of petroleum is drawing to a close and when it does, there will still be billions of barrels in the ground because EROEI was too low. End of story.

And, I might add, I hope it is soon so there is still some of the good parts of the earth left for my grand kids and their grand kids. Capitalism needs to die and soon.

SOS on Thu, 25th Oct 2012 4:46 pm

Im wondering how its possible oil companies are now producing record profits and record production and record proven reserves and record significant reserves with such a terrible and civilization crushing EROEI?

I have no idea what you mean by profitable. Profits are being produced in record amounts all up and down the production chain. The drillers, royalty holders, working interest investors, brokers, refiners and dispenderies suppliers of all sorts and cooperative goernments are all doing very well indeed yet they have a terrible EROEI that predicts their doom?

GregT on Thu, 25th Oct 2012 6:50 pm

Sounds eerily familiar.

Take a good long look at the cause of the housing bubble.

Natgas on Fri, 26th Oct 2012 12:44 am

“The marginal cost to develop shale oil in the US is around 90 USD per barrel with average cost of most plays around 60 USD per barrel.”

Its still expensive. No idea as how long this price could be maintained. Meanwhile the cost of Solar has plunged so much that even middle eastern countries are considering to invest heavily in that area.

BillT on Fri, 26th Oct 2012 2:39 am

Natgas, even solar depends on oil to exist. you will not replace those panels with the net energy from solar when they wear out. Not even close!

And all SOS can think of is dollar profit, not loss of the environment that he needs to live. Fool.

Arthur on Fri, 26th Oct 2012 10:10 am

Bill, consider this calculation:

You need ca. 0.5 barrel of oil to produde a m2 of solar panel.

You need an area of Spain (500,000 km2) to meet the entire energy demand of the planet.

This implies 0.25 trillion barrel of oil to set this up.

The planet once had 2 trillion barrel, with more than 1 trillion consumed to date. This illustrates that every freaking barrel of oil should be spent setting up a new energy base **NOW** and not wasted in cars.

Pure silicon (I think) can be recycled and used in new panels with far less energy cost, after the life cycle of a panel (30 years) has been completed.

The EROEI of a panel is ca. 7. That is not spectacular but good enough.

Obviously, we not only have oil, but also gas and coal, so it can be done, but the longer we wait the bigger the crash will be.

A sensible energy policy would be to:

1) discourage the use/ownership of the car, arguably the largest desaster happened to mankind.

2) increase tax on carbon to the extent that private individuals are pushed into investing in a solar roof and/or a community windturbine in windy places.

BillT on Fri, 26th Oct 2012 11:04 am

I find it interesting that it only take 1/2 barrel of oil (~21 gallons) to mine, transport, refine, transport, machine, manufacture, transport and install & maintain 2 – 1 meter square panels (~160 watts). But,assuming your figure is correct, then you just proved that it is already too late. Not going to happen. The first world is NOT going to cut their use by 25% to make it possible and then there would be so much political and corporate arguing that it would not happen even if…

But does your calculation also include the many billions of tons of ores needed to provide all of the other needs of the planet? After all, the home we are going to build in a few years requires 70 tons of concrete and 5 tons of rebar steel just for the shell. (140 Sq.M.) The condo tower going up beside mine used many hundreds of times that and it is one of maybe 100 towers going up in Manila alone.

And does that include manufacturing the fertilizers, and pesticides needed to feed 7 billion plus eaters?

You are correct that it ‘could’ work, but reality says we don’t have a chance in hell of it happening in the real world.

Arthur on Fri, 26th Oct 2012 12:11 pm

Yes Bill, I am afraid that it will not pass the ‘could’ level indeed. Not enough foresight available on this planet. But some societies have more foresight & competence than others. They likely will become the nucleus of 0.5-1.0B humanity post 2100.

Arthur on Fri, 26th Oct 2012 3:19 pm

I found more data concerning the amount of energy needed to produce a panel:

http://www.linkedin.com/answers/Sustainability/green-products/SUS_PRD/727874-27005339

The post at the bottom is from a “lenke D., Social Media Manager at Essent”. Essent is a privatised energy producer and (Essent) a client of mine. She says that on average it takes 400 kwh/m2 (multicrystalline solar cell). A barrel of oil contains 1700 kwh, so according to this source it even takes less than a quarter of a barrel to produce one m2 panel. And I would be surprised if the new solar film cells cost even less.

Arthur on Fri, 26th Oct 2012 3:39 pm

Let’s do a more accurate calculation:

http://en.wikipedia.org/wiki/World_energy_consumption

World energy consumption: 142 terawatthour (2008)

Sahara solar panel yield: 300 kwh/m2

Terawatthour = 1000 gigawatthour = 1,000,000 megawathout = 1,000,000,000 kwh

Necessary surface: 473,333 km2

That is indeed Spain, as I said before. Obviously a real installation needs easily three times as much space, but hey, the Sahara is big enough for even that.

In other words, the world ‘only’ needs 0.12 trillion barrel of oil to construct a radical new energy base, based on solar. That is doable (in terms of remaining carbon capital). And in fact, considering the waste, half of that would be enough to still have a somewhat liveable planet.