Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on July 8, 2015

China Peak Oil: 2015 Is the Year

Domestic production looks set to peak, with some profound implications for the world market.

Intense focus on the North American shale boom, Saudi Arabia, and ISIS obscures an important emerging energy trend: China’s oil production is peaking. This has profound implications for the world oil market, because China is not just a massive importer of crude; it is also among the world’s five largest oil producers, trailing only the U.S., Russia, and Saudi Arabia, and virtually neck-in-neck with Canada.

China’s oil industry has delivered impressive oil and gas production growth over the past decade. Yet a range of data and historical analogies increasingly suggest that, at global oil prices between $50-to-$100 per barrel, China’s oil supply capability is plateauing and may peak as soon as this year. Lower or higher prices would accelerate or extend this timing.

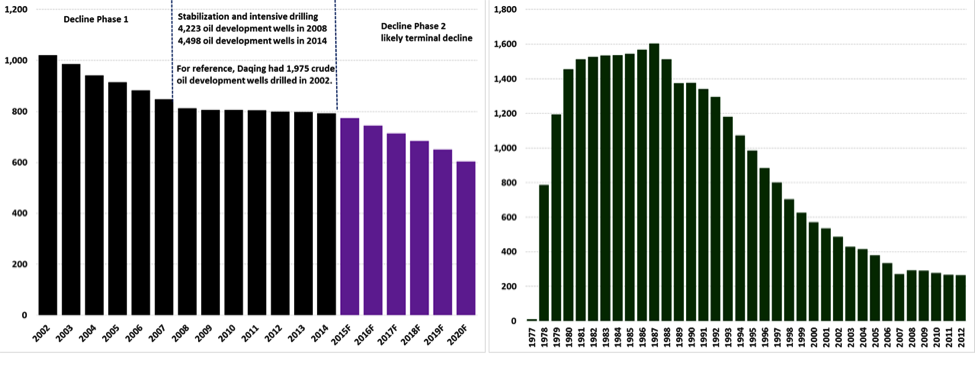

China’s crude oil output has stagnated for the past two years despite intense drilling activity on land and offshore. In late 2014, CNPC essentially threw in the towel on its workhorse field, Daqing, announcing that it would allow the field to essentially enter a phase of managed decline over the next five years. Under this new approach, the field’s oil production will fall from 800,000 barrels per day (kbd) in 2014 to 640 kbd by 2020: a 20 percent decrease. To highlight the importance of PetroChina’s decision, consider that Daqing currently accounts for approximately one in every five barrels of oil currently pumped in China – on par with the role Alaska’s massive Prudhoe Bay field has played in U.S. oil production.

While Daqing’s output has thus far declined less steeply than Prudhoe Bay’s, the Prudhoe experience shows that for even a massive field, once the steep stage of the terminal decline output phase begins, there is generally no turning back (Exhibit 1).

Exhibit 1: Oil Production Trajectories of Daqing and Prudhoe Bay, ‘000 bpd

Daqing Prudhoe Bay

Source: Alaska Oil & Gas Conservation Commission, PetroChina, EIA, Author’s Analysis

Daqing’s oil production has declined relentlessly, despite PetroChina’s significant increase in drilling activity in the field during recent years. This suggests a significant risk that production could fall faster than planned. For reference, PetroChina drilled 1,975 development wells in 2002 when oil production averaged 1.079 million barrels per day, but was forced to boost this to 4,498 development wells in 2014, when oil output at Daqing averaged 792,000 barrels per day. In short, the number of development wells drilled increased by nearly 250 percent while oil production fell by roughly 27 percent.

Unconventional Production

The oil industry consistently deploys ingenuity and technology to break through many geological and economic barriers. China has large potential shale oil reserves, as many as 32 billion barrels of which are technically recoverable, according to the EIA. However, aboveground barriers created by politics and local legal, regulatory, and ownership systems constrain development.

Combine such hurdles and disincentives to innovation with complicated shale geology, and the outlook for commercial-scale development in the next five to seven years becomes dim. The fundamental question is this: Can China bring unconventional oil online in time, and in sufficient measure, to offset terminal oil output declines in its workhorse conventional oilfields?

The short answer increasingly appears to be “no.” Four key factors restrain Chinese crude oil output, which will most likely remain at or below the 4.25 million barrel per day mark. The first factor is a global one: low crude oil prices. The breakeven costs of Chinese oilfields vary and data on this important metric are scarce. But what is clear is that China’s core oilfields – especially Daqing and Shengli – are older, suffer from significant reservoir depletion, and require intensive enhanced recovery techniques that eat into profitability. In an uncertain oil price environment, this reduces producers’ incentives to boost drilling to the point necessary to potentially increase production.

The second factor is more specific to China: declining old geology and complex new geology. Even if PetroChina and Sinopec did significantly increase their drilling activity at Daqing and Shengli, production returns would likely be marginal at best. As cited above, Daqing production drilling rose by a factor of nearly 2.5 between 2002 and 2014, yet oil output fell by more than 25 percent.

Factor three is China’s unconventional oil production potential. With the old fields declining, one may ask: Can hydraulic fracturing deliver a Chinese shale boom like what the U.S. has experienced? The long answer is that “it’s complicated” but the short answer is generally “no.” China’s unconventional oil deposits are more challenging to work with than North American ones. North American tight and shale oil plays tend to have been deposited by ancient seas, while China’s hydrocarbon-bearing shales were left behind by prehistoric lakes, leaving rock layers that are more ductile and less “fracable” than brittle marine shales.

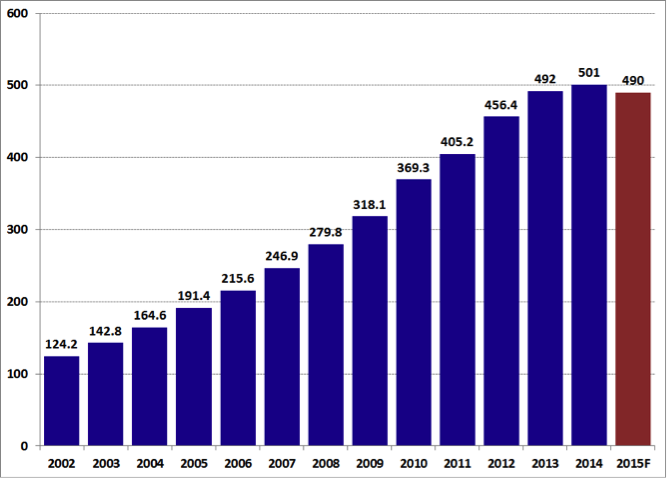

There are some areas with promising tight oil potential. For instance, the Changqing Field in the Ordos Basin of Northwest China – China’s signature tight oil play to date – has seen production grow from 124 kbd in 2002 to 500 kbd in 2014 (Exhibit 2). However, Changqing’s production growth rate has slowed significantly over the past three years and appears poised to decline slightly in 2015, based on first quarter production of 487 kbd, which was lower than the 2014 average production figure despite a relatively mild winter. The drop suggests that low prices slowed drilling activity in the Ordos Basin, although this author has not yet seen explicit confirmation of this.

Exhibit 2: Slowing Changqing Output Suggests Tight Oil Insufficient to Offset Core Fields’ Decline

Source: PetroChina, Author’s Analysis

Despite some recent announcements of additional tight oil discoveries, Changqing’s slowing production growth rate over the past three or four years contrasts sharply with the hyperbolic production growth seen during the booms in world-class tight oil plays like the Bakken and Eagle Ford shales in the U.S. This difference is critically important because to offset production declines and propel significant net growth in a mature oil province like China or the U.S. requires multiple massively robust unconventional fields.

Yet Chinese tight oil plays so far have not reached nearly such a scale. Data from CNPC show that wells from the Zhuang-183 drilling program had an average test production rate of approximately 750 bpd. That is clearly commercial, but top U.S. shale wells in the Eagle Ford and Bakken can yield initial production (“IP”) rates exceeding 4,000 bpd of oil and liquids. Horizontal wells in the highly productive Permian Basin of Texas and Eastern New Mexico often yield 30-day IP rates of 500 bpd of oil, which will typically translate into an initial production test rate in the same range as CNPC’s Zhuang-183 Ordos horizontal wells.

Above-Ground Factors

To boost production on a national level, China’s oil companies will need to employ industrial-scale drilling that brings thousands of horizontal oil wells online each year. This would entail a quantum leap from the 1,610 horizontal wells CPC drilled in China during 2014, particularly because a significant number of these wells aimed to find gas. If they attempt this, Chinese producers will likely crash into systemic barriers that in many ways matter far more for unconventional oil and gas development than oil prices or geology do; namely, factors that promote oil and gas sector innovation. Innovation confers an incredible ability to adapt to volatile commodity markets and challenging geological issues.

Herein lies factor four: aboveground limitations on China’s unconventional oil potential. The U.S. shale boom arose in a very unique setting. This analysis certainly is not about U.S. “energy exceptionalism,” but the unique combination of dozens of operators with stock market capitalizations exceeding one billion dollars who enjoy access to deep capital markets, incentives to take risks, and a land and mineral ownership system that provides strong financial motivations for oil and gas development are major pluses that China largely lacks.

Chinese companies are well-positioned to rapidly fill in gaps in the country’s physical oil and gas infrastructure. However, the institutional and legal structures and corporate ecosystem (especially independent drillers) that have driven U.S. unconventional energy development are much harder to replicate. For a case in point, consider how independent U.S. energy producers have driven the fracking boom while the international majors have largely failed to generate organic unconventional oil and gas growth.

Many independent firms such as EOG Resources grow organically by discovering and developing new shale and tight oil plays. Yet the international behemoths like ExxonMobil and Statoil have had to buy their way into unconventional plays after the fact, often finding less success and lower than expected returns when they do. At this point, no evidence suggests CNPC/PetroChina or Sinopec will fare any better at unconventional oil development than the U.S. and European oil majors have.

Offshore Production

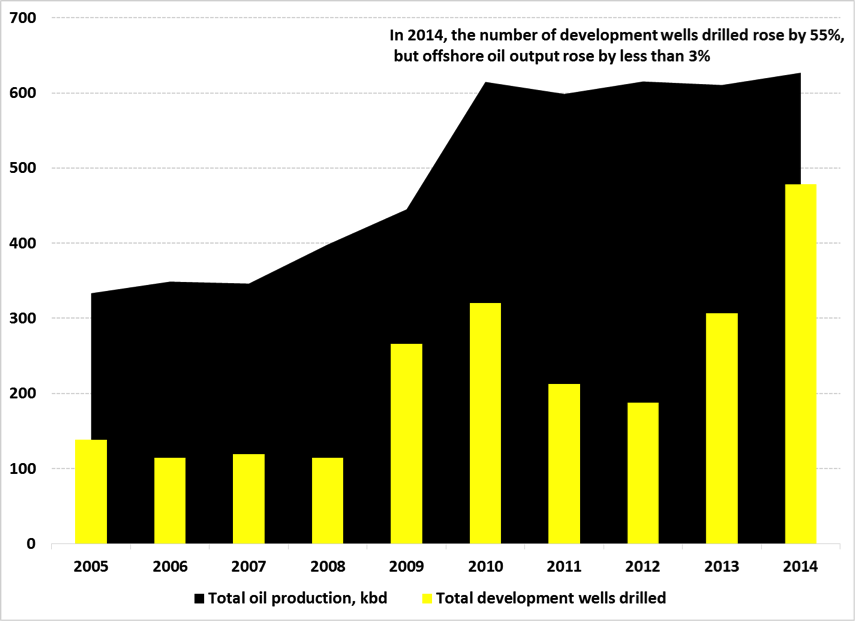

China oil production optimists may point to a handful of offshore projects CNOOC will bring online this year in the Bohai Gulf as evidence that China still has room to expand domestic oil output. For those holding this view, here is the way to put output from new fields in perspective: in 2015, CNOOC plans to activate fields off China that at their peak (likely to come in 2016 or beyond) could produce 108 kbd of oil.

In contrast, assuming a 4 percent natural decline rate in all Chinese oilfields (a conservative assumption), drillers still must bring on nearly 170 kbd of new oil production each year just to compensate for natural depletion and keep production at its current level. CNOOC, which dominates oil production offshore China, forecasts that production of all hydrocarbons will grow very slightly in 2016 and 2017. Because most of China’s large offshore energy discoveries in recent years have been of natural gas field, CNOOC’s reluctance to break down its forecast into oil and gas subdivisions reinforces the growing wave of data suggesting that offshore oil production will not turn the tide of China peak oil (Exhibit 3).

Exhibit 3: Offshore Oil Production Will Not Turn the Tide of Oil Production Declines

Source: CNOOC, Author’s Analysis

Strategic Implications

The latest IEA data estimate that China’s crude oil output in 2015 will average 4.3 million barrels per day. This is likely to be the high-water mark for China’s domestic oil production, as oil price uncertainty and disruption from anti-corruption investigations trim oil executives’ risk appetites in 2015. CNPC and CNOOC, in particular, are very upstream focused and will not drill as aggressively with investigators sniffing around while oil trades at a bit more than half the price it fetched a year ago. But such tactically driven activity declines should not obscure the underlying strategic story: China would still very likely be at peak oil production this year even if oil prices were closer to $100 per barrel.

Looking out to 2020, tight oil output may well increase if drillers can “crack the code” of China’s ductile lacustrine shales. But this oil would simply slow the stasis and impending decline in national crude oil output. The Chinese oil patch does not appear to have any world-class unconventional oil plays like the Bakken, Eagle Ford, or Vaca Muerta poised to emerge within the next five years in a way that would reverse the emerging peak production situation.

It is increasingly likely that if new unconventional oil resources become commercially productive in China, by that time their output will simply compensate for depletion of existing conventional oil resources, rather than actually boosting net oil output as has been the case in the U.S. As things stand, the evidence increasingly points to a future where China’s national oil companies will preside over a gradual crude oil production decline that begins now, in 2015.

12 Comments on "China Peak Oil: 2015 Is the Year"

BobInget on Wed, 8th Jul 2015 8:55 am

OTOH China has done a bang-up job securing

overseas imported crude. In no time China and India could easily sponge up every available export barrel. Why else would China risk war with

its China Sea neighbors? For the first time NPR

admitted China Sea is all about oil and gas.

(will the Arctic be the Next China Sea?)

Its always been a certainty, China’s domestic production could never keep pace with demand.

Ultra deep water, shale (tight oil) E&P are dancing as fast as it can. Doubtless China and others will improve technology but there are limits.

As usual attention is drawn to China when India’s

population, energy demands are growing faster.

In doing a search for India’s peak oil situation I came across this : http://www.wolfatthedoor.org.uk/mainpages/countries.html

Mark Bucol on Wed, 8th Jul 2015 8:57 am

Two possible limitations of China’s shale oil production:

Transportation to refineries may be a problem with fewer rail lines in the interior. China has built many new high speed rail lines but these cannot be used for freight rail.

Also, does China have infrastructure for fracking, such as the high pressure pumping equipment and disposal well drilling available? Maybe they will just dump the solvent laden salt water in the backyards of the peasants.

Hello on Wed, 8th Jul 2015 9:01 am

There is no reason to frantically drill for oil when oil can be bought for cheap on the world market.

Deja vu?

Yes, when in 1970 the US peaked it did not peak because it was not possible to get more oil out of the ground, but it peaked because it was cheaper to buy oil from the ragheads.

BobInget on Wed, 8th Jul 2015 9:31 am

Hello is pointing to why the US started importing ME crude in the first place. China, like the US will be forced to fight wars to protect those imports from all comers.

Today, EIA releases “petroleum status report”

here are a few educated guesses:

API crude oil inventories: -958,000 barrels

Crude stocks at Cushing rose by 262,000 barrels

Gasoline stocks fell by 2.041 million barrels

Distillate rose by 4.2 million barrels

The expectation for the data from EIA tomorrow is -488.89K bbls for US Crude Oil Inventories

Analysts Forecast 1 Million-Barrel Drop in Crude Stocks

Nicole Friedman, WSJ: Jul 07, 2015

NEW YORK–

Estimates from 12 analysts surveyed by The Wall Street Journal project that U.S. oil inventories have fallen by 1 million barrels, on average, in the week ended July 3.

Eight analysts expect stockpiles to fall, while another three expect a rise and one analyst sees stocks unchanged in the week. Forecasts range from a rise of 2.8 million barrels to a decline of 3.5 million barrels.

Gasoline stockpiles are expected to be unchanged in the week, according to analysts. Six analysts expect an increase, with three expecting a decline and three seeing no change. Estimates range from a rise of 1.5 million barrels to a drop of 1.5 million barrels.

Stocks of distillates, which include heating oil and diesel, are expected to rise by 1 million barrels. Eleven analysts expect a rise, while one sees no change. Forecasts range from unchanged to a gain of 2.5 million barrels.

Refinery use is seen rising 0.1 percentage point to 95.1% of capacity, based on EIA data. Six analysts expect a gain, three expect a drop, one sees no change and two didn’t provide an estimate. Forecasts range from a rise of 0.5 point to a decline of 0.6 point.

Crude Gasoline Distillates Refinery Use

Again Capital 1.1 -0.9 1.8 0.3

Citi Futures Perspective -1.5 unch unch 0.2

Confluence Investment Management -3.0 unch 1.0 0.5

EBW AnalyticsGroup -3.5 1.5 1.0 unch

Energy Management Institute -1.5 0.3 1.0 0.2

Excel Futures 2.8 -1.4 0.9 -0.6

Frost & Sullivan -2.0 1.0 1.5 -0.25

IAF Advisors -2.0 unch 0.5 n/a

Ritterbusch and Associates unch 0.3 1.2 0.2

Schneider Electric 0.8 -1.5 0.5 0.5

Tradition Energy -2.5 1.0 2.5 -0.5

Tyche Capital Advisors -1.0 0.25 0.2 n/a

AVERAGE -1.0 unch 1.0 0.1

(Figures in millions of barrels except for refining capacity, which is reported in percentage points. For analysts providing forecasts in a range, the average of the upper and lower ends of the range is used.)

The following is the actual report;

Summary of Weekly Petroleum Data for the Week Ending July 3, 2015

U.S. crude oil refinery inputs averaged 16.6 million barrels per day during the week

ending July 3, 2015, 65,000 barrels per day more than the previous week’s average.

Refineries operated at 94.7% of their operable capacity last week. Gasoline production

decreased last week, averaging about 9.9 million barrels per day. Distillate fuel

production increased last week, averaging 5.1 million barrels per day.

U.S. crude oil imports averaged over 7.3 million barrels per day last week, down by

197,000 barrels per day from the previous week. Over the last four weeks, crude oil

imports averaged about 7.2 million barrels per day, 1.6% below the same four-week

period last year. Total motor gasoline imports (including both finished gasoline and

gasoline blending components) last week averaged 852,000 barrels per day. Distillate

fuel imports averaged 164,000 barrels per day last week.

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum

Reserve) increased by 0.4 million barrels from the previous week. At 465.8 million

barrels, U.S. crude oil inventories remain near levels not seen for this time of year in at

least the last 80 years. Total motor gasoline inventories increased by 1.2 million barrels

last week, and are in the upper half of the average range. Both finished gasoline

inventories and blending components inventories increased last week. Distillate fuel

inventories increased by 1.6 million barrels last week and are in the middle of the average

range for this time of year. Propane/propylene inventories rose 2.2 million barrels last

week and are well above the upper limit of the average range. Total commercial

petroleum inventories increased by 10.6 million barrels last week.

Total products supplied over the last four-week period averaged 19.9 million barrels per

day, up by 4.7% from the same period last year. Over the last four weeks, motor gasoline

product supplied averaged over 9.5 million barrels per day, up by 5.3% from the same

period last year. Distillate fuel product supplied averaged about 3.9 million barrels per

day over the last four weeks, up by 1.5% from the same period last year. Jet fuel product

supplied is down 6.5% compared to the same four-week period last year.

BobInget on Wed, 8th Jul 2015 9:43 am

This report is seen by traders as bearish because markets are well supplied. Note, estimates were for a one million barrel draw.

I always look at the last paragraph first.

That jet fuel number (down 6.5%) is concerning.

Jet fuel is a leading economic indicator. Jet fuel has been going lower for weeks, but never negative. Since crude has dropped substantially

airlines may be waiting for an even bigger tumble.

19.9 Million barrels p/d still looks bullish. I don’t know what to make of this report.

BobInget on Wed, 8th Jul 2015 10:23 am

CNBC Headline:

Saudi Arabia to invest $10B in Russia – CNBC.com >>> means Oil price to rise

Saudi Arabia & Russia are the largest oil exporters.

As such these countries don’t have natural ties. And in many cases (e.g. Syria) there is a clear conflict of interest.

However, both countries are strongly dependent on the price of oil.

Now it looks like that SA and Russia have found each other. So, that we may expect that there is a common interest to increase the oil price.

So, we may well get here a nice bounce of the PoOil. BTW Today already a nice intraday reversal.

Let us wait and see….

Saudi Arabia to invest $10B in Russia – CNBC.com

http://www.cnbc.com/id/102813525

– Saudi Arabia’s sovereign wealth fund is to invest up to $10 billion in Russia over the next five years, in a move signalling a thawing in relations …

Above a screen shot, swiped from energy board.

What I found most interesting.. KSA anticipated

the coming OPEC revolt and decided to use cash

to buy Russia’s compliance.

Perhaps, even more important… KSA is looking to Russia, not India, not China, not Canada not internally, for additional oil.

KSA is committing 20 Billion over five years..

that’s the key. OVER FIVE YEARS.

Russia needs to go along with KSA, not support

Iran, not give military aid to Syrian or current Yemeni governments.

Who knows who or what else Putin betrayed to get his mitts on the first 20 billion?

A very important story. Here’s hoping we all live to see the outcome. Smell a double cross? I do.

rockman on Wed, 8th Jul 2015 11:20 am

As posted elsewhere:

“China’s crude oil output has stagnated for the past two years despite intense drilling activity on land and offshore.” As of just yesterday Reuters would disagree. From http://www.reuters.com/article/2015/07/ … 4G20150707

China’s crude oil output looks set to rise this year from a record in 2014 as new production from third largest producer CNOOC helps to counter reductions from its two bigger rivals.Output growth from China would add to a global glut even as exporters such as OPEC and Russia produce at near record highs and U.S. shale producers keep ramping up output.

With the global oversupply as much as 2.6 million barrels per day (bpd), international crude prices have been nearly cut in half over the past year.

While there is no official Chinese production outlook, information from the biggest state oil companies indicates the nation’s output will rise slightly in 2015, largely due to increased production from CNOOC Ltd, the listed unit of state-owned China National Offshore Oil Corporation.

“What we have spent in the last few years has laid the foundation for the production growth this year,” said an employee with CNOOC’s investor relations department who asked to remain unnamed. CNOOC spent $17 billion on capital expenditures in 2014. Despite recent cost cuts, CNOOC has said it has already added at least 40,000 bpd of crude output this year. And it aims to increase daily domestic oil and gas output in China by at least 135,000 barrels of oil equivalent by the end of 2015, according the company’s 2015 outlook.

China, the world’s fourth biggest oil producer, raised its output in the first five months of this year by 1.8 percent from a year ago to 4.25 million bpd, compared with growth of just 0.1 percent over the same period in 2014. In 2014, China produced an annual record 4.2 million bpd. “I think Chinese crude output is going to maintain its current levels … and go higher before the end of the year,” said the director of global research for Standard Chartered. The bank expects China’s production to rise 1.6 percent this year, although growth could stall or decline in 2016.

Plantagenet on Wed, 8th Jul 2015 11:34 am

The suggestion that China’s oil production is peaking ignores the fact that China is in the act of seizing huge expanses of ocean that contain large amounts of oil and gas resources.

China may very well be building islands and military bases in the ocean to seizie the large expanse of ocean territory precisely so they can produce more hydrocarbons.

Nony on Wed, 8th Jul 2015 1:05 pm

Funny how 100/bbl leads to non-OPEC growth. Hmmm…econ 101 works after all.

Apneaman on Wed, 8th Jul 2015 1:30 pm

“econ 101 works after all” Like China and Greece? The more it unravels the louder the corns get. Go long on Ramen noodles Marm-A-noon.

Makati1 on Wed, 8th Jul 2015 9:27 pm

What to believe? Actually, I believe none of it. The spin in the oil/energy industry is reaching category 5 and will soon equal that of the US MSM.

Pop the top on a bottle of your favorite brew, open a bag of beer pretzels, pull your lounge chair into the shade and watch the world disintegrate, like I do. It’s much more interesting than anything on the Boob-tube or at the local theatre.

shortonoil on Thu, 9th Jul 2015 8:34 am

Daqing hit a 98% water cut in 2003. It has only been through the injection of massive quantities of surfactants, and detergents that the field has been able to produce at all over the last decade. It should be evident by now that production from depleted fields can be maintained at a high level until the absolute end. The end of Chinese oil production growth has been in the cards for a long time.

As far as LTO production from Chinese shale it will never be developed by the Chinese. LTO comes from source rock, which is deep, hot and high pressure. It is feed stock material, not fuel producing material. The Chinese need “fuels” not feedstock to produce plastic. Qatar and Russia have an abundance from high permeability condensate reserves which the Chinese can buy for a fraction of what it would cost them to produce their own. The shale methodology just goes on, and on. Shale is not a replacement for conventional crude, it is a liquid hydrocarbon with limited industrial use.