Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on January 4, 2016

BAKKEN – Single Well Economics

This is a guest post by Ciaran Nolan

Disclaimer

The opinions and views expressed in this presentation are solely those of the author and not necessarily those of any organisation.

Introduction

This presentation builds upon earlier work carried out by the author in May 2015 on the North Dakota (ND) Bakken / Three Forks Light Tight Oil (LTO) Play – ‘Bakken – the bubble has burst’*.

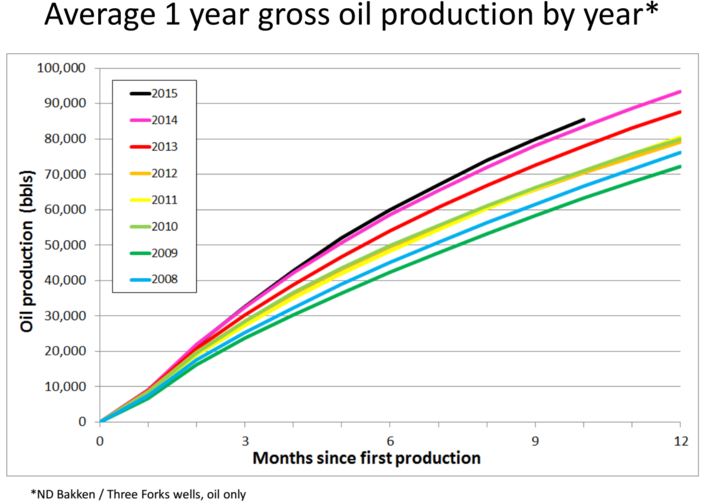

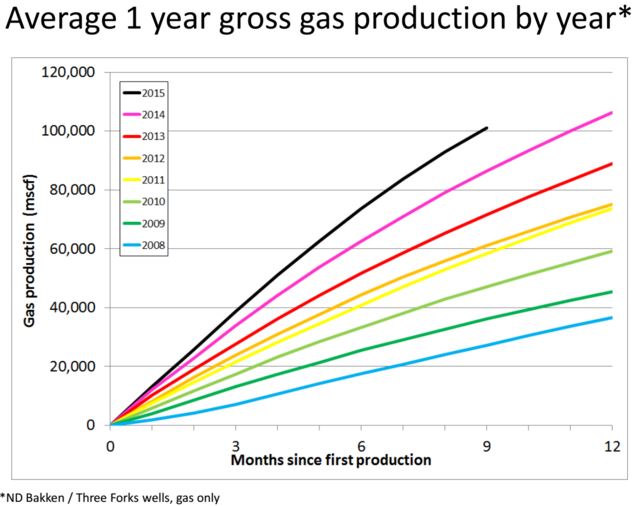

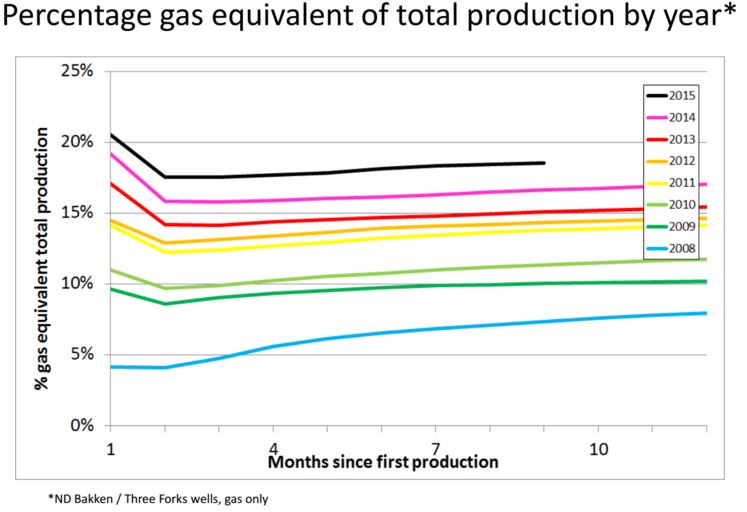

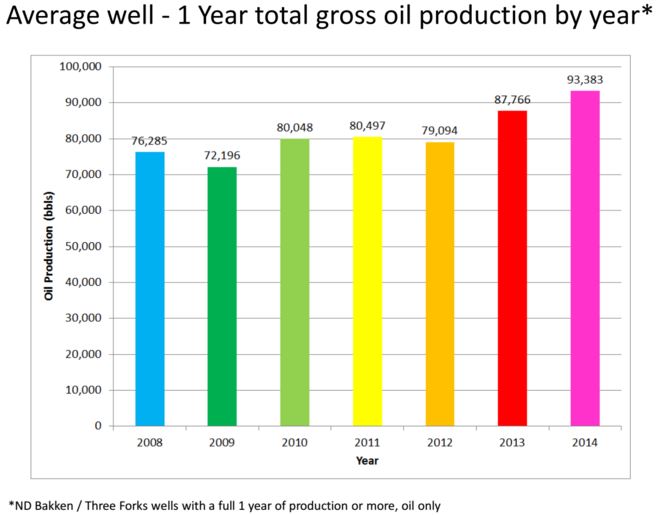

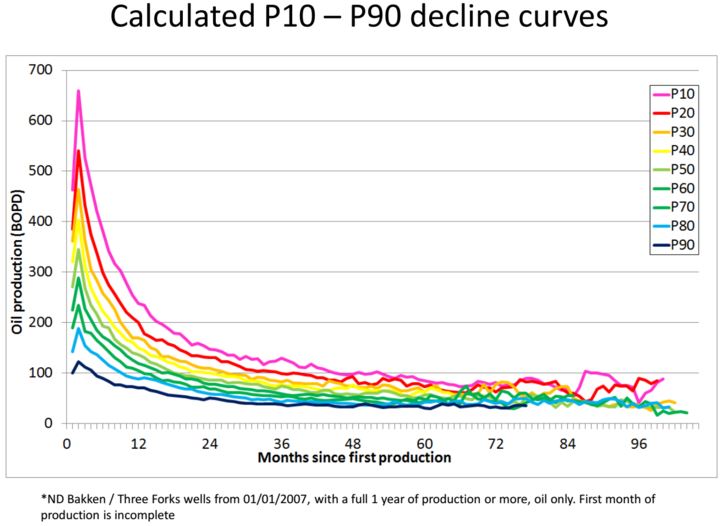

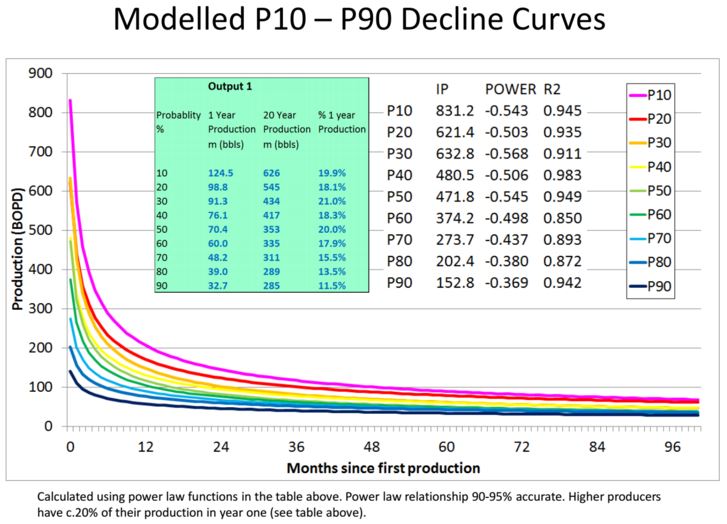

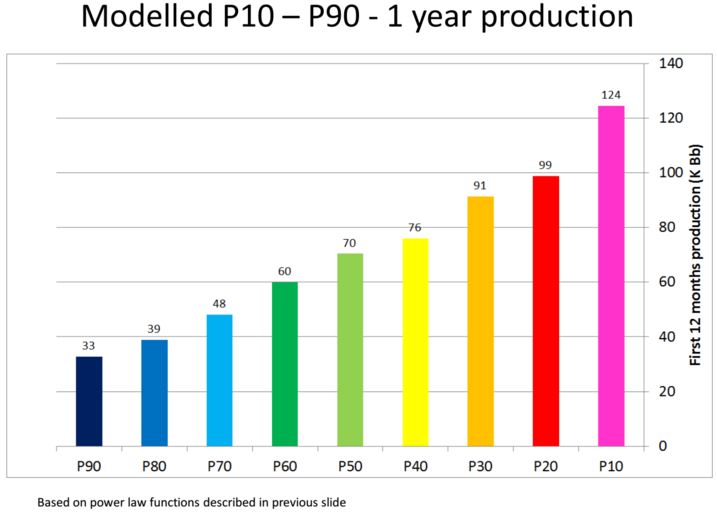

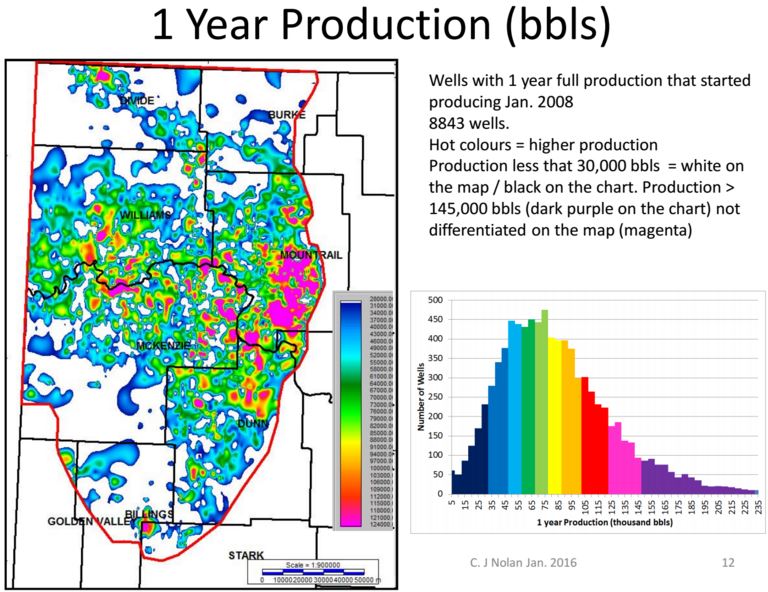

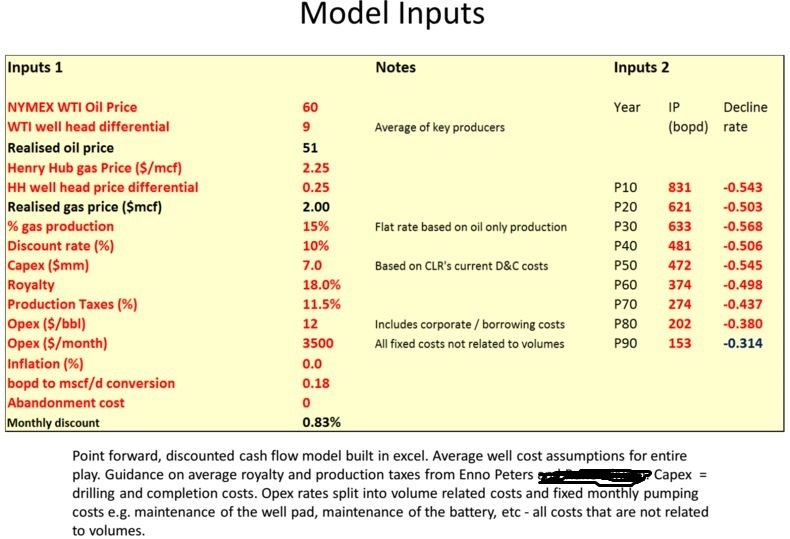

North Dakota Industrial Commission (NDIC) production data (up to November 2015) kindly supplied by Enno Peters. Feedback from Enno Peters and Rune Likvern. Data analysed in Excel and IHS Kingdom. Production decline curves generated for P10 – P90 type wells, based on 8843 wells with 1 year full production (January 2007 – October 2014).

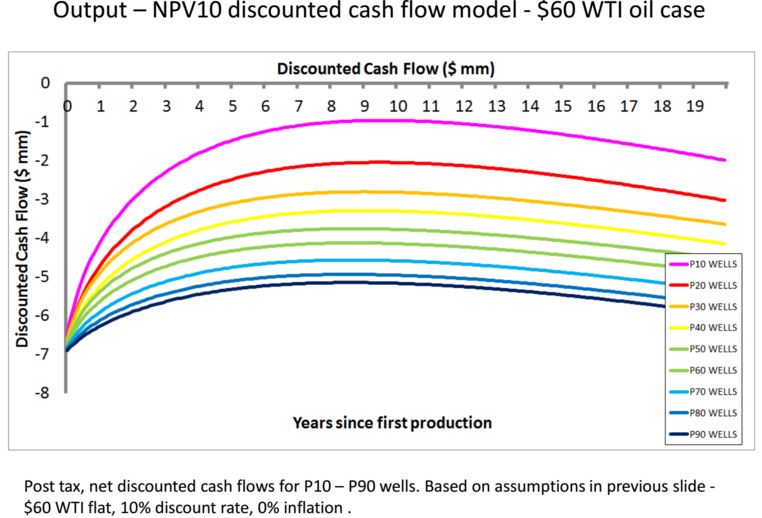

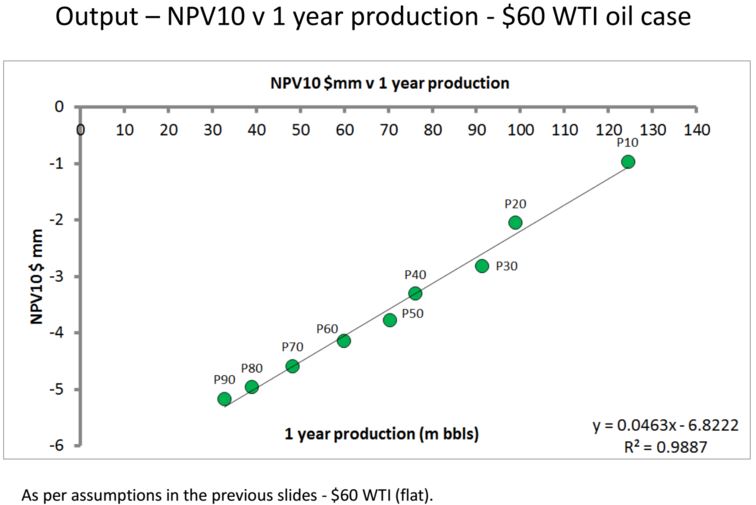

Discounted cash flow (DCF) models were generated by the author for single wells in the ND Bakken / Three Forks Play.

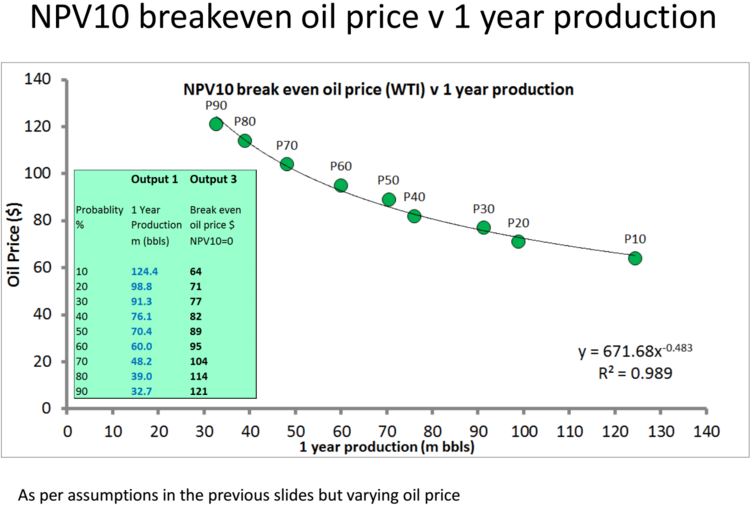

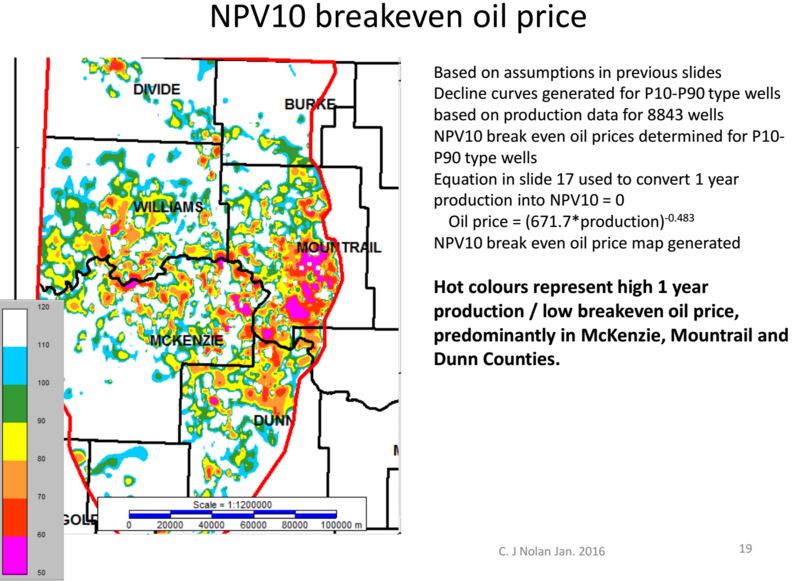

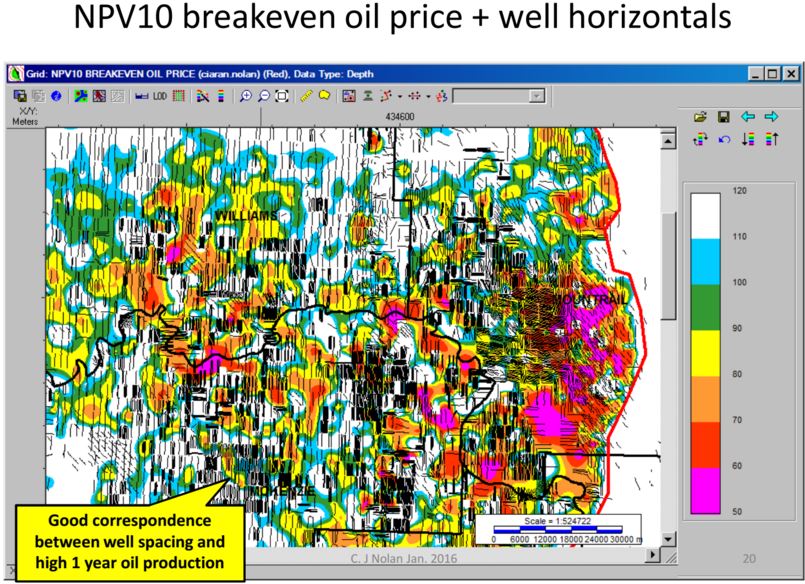

Break even oil prices for Net Present Values with a 10% discount rate (NPV10) determined for P10 – P90 type wells. NPV10 break even oil price map generated. Historical NPV10 generated for average wells for 2008 – 2015. NPV10 breakeven oil price determined for top ten Bakken Producers in 2014, for 2014 wells.

ND – Bakken / Three Forks

Single Well Economic Model

Whiting Petroleum (WLL)

December 2015 Presentation

Single Well Economics – 2015 Type Well

ND – Bakken / Three Forks

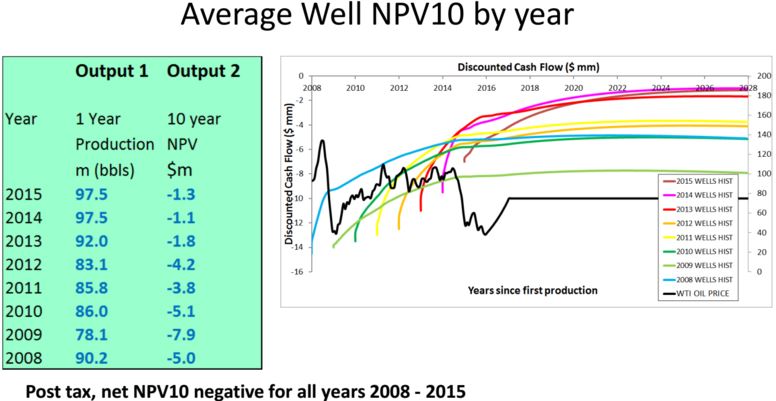

Historic Economics

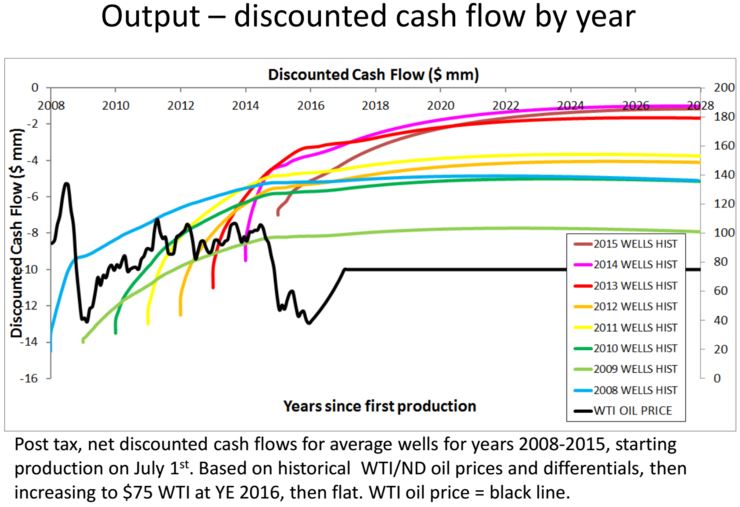

ND Bakken / Three Forks Average

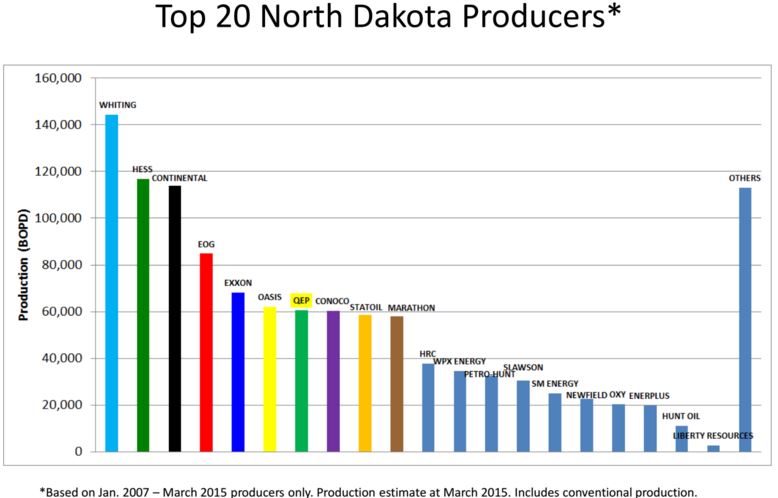

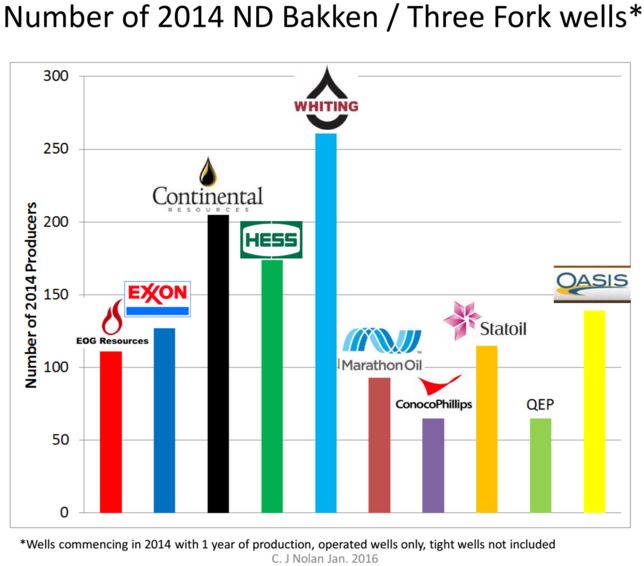

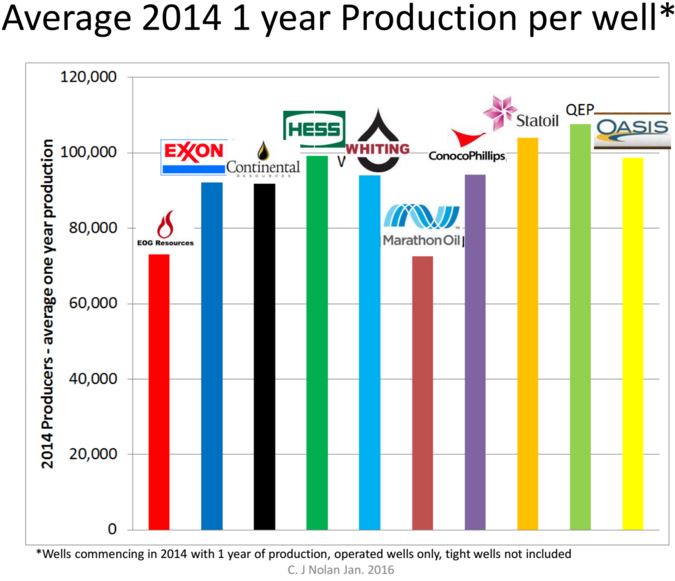

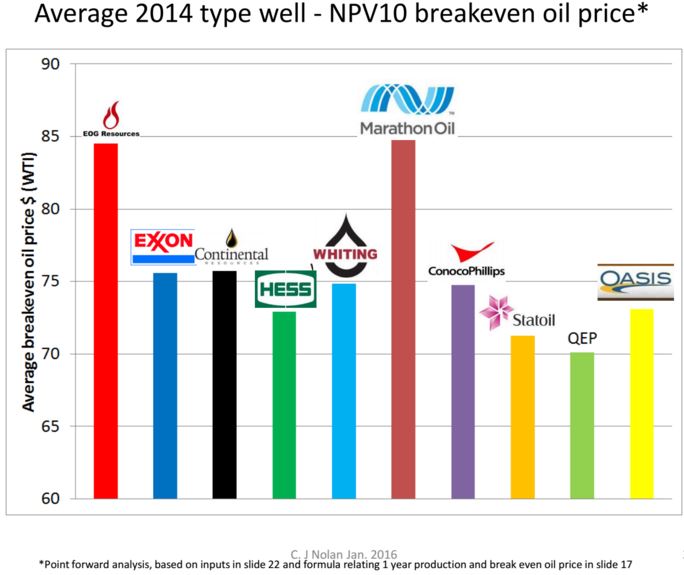

2014 production by company and

breakeven oil price

Conclusions

Discounted cash flow models were generated by the author on a single well basis, for the North Dakota (ND) Bakken / Three Forks Light Tight Oil Play.

Breakeven oil prices for Net Present Values with a 10% discount rate (NPV10) determined for P10 – P90 type wells. NPV10 break even oil price map generated based on established relationship between NPV10 and 1 year oil production. Historical NPV10 generated for average wells for 2008 – 2015. NPV10 breakeven oil prices determined for the top ten producers in 2014, for 2014 wells only.

Pre-tax and post tax comparison made with Whiting Petroleum (WLL) 2015 type well. Good correspondence with WLL pre tax numbers.

Point forward economics (net, post tax, based on average cost assumptions) indicate that at $55 (WTI) none of the ND Bakken / Three Forks is NPV10 positive. At $89 (WTI) 50% is NPV10 positive, at $121 (WTI) 90% is NPV10 positive. Historical NPV10s are negative for all years.

Using Whiting Petroleum 2015 well assumptions and $50 WTI oil price, model results are pre tax NPV10 = $3.43MM per well (Whiting Petroleum = $3.17MM), post tax = $-1.5MM

For an average 2014 type well, the majority of the top ten Bakken / Three Forks producers have forward breakeven oil prices of $70-75 (WTI).

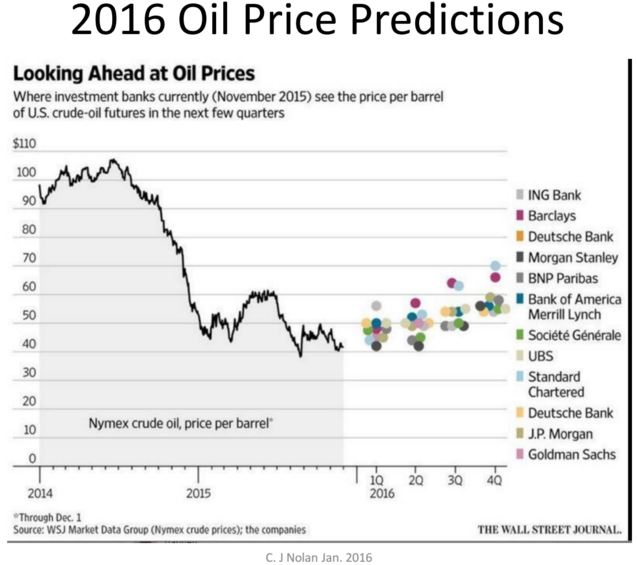

Most Investment Banks are predicting oil prices below $60 (WTI) in 2016.

7 Comments on "BAKKEN – Single Well Economics"

Nony on Mon, 4th Jan 2016 1:48 pm

Borrowing costs should not be included in OPEX. They are a financing cost. Are accounted for by the 10% return. [This is a fundamental concept, not an opinion. See Copeland Valuation or any book on DCF modeling.] As done now, the author is double counting the cost of capital.

Rest of the work looks decent and big effort. Didn’t check it all for flaws though.

Agree that Bakken is in bad news at sub $40.

Ralph on Mon, 4th Jan 2016 6:20 pm

Bakken is in bad news sub $70

Other plays are probably in worse news.

Nony on Mon, 4th Jan 2016 10:28 pm

Looked at it a bit more. Certainly a lot of work and some of it decent. My comments more to help the author fix some things:

1. (as before) including charges for interest in OPEX AND requiring 10% return on investment is double counting.

2. Even if you did some form of equity DCF NPV (and don’t, calculation should be more impartial to capital structure), you still shouldn’t have the interest cost as part of a “per barrel” flat $12. After all, the amount of financing is the same but is distributed over more barrels for the prolific wells. [fixed with correcting item 1, but think this is an important teaching point.]

3. The whole variable cost $12 looks fishy. Need to show that buildup (sources, assumptions, breakdown). It’s a big part of what is driving the result here. So go into more detail.

4. $2.25 for gas (going forward for next several years) seems low. HH shows strip climbing to ~3 in a couple years.

5. Discussion needs to address the price of oil by year (after all, we have a structure that shows different amounts of production of oil per year). There is a strip. Could consider to just copy it (don’t have to go month by month, just approximate). Or at least make some simple structure like a ramp or the like.

6. Yes, the IBs predict low oil prices for 2016:

http://www.reuters.com/article/us-oil-prices-poll-idUSKBN0UI0XZ20160104

but the strip is even lower (~$41 average price). In any case, don’t make the mistake of thinking only of 2016 though. After all you have a model that goes 20 years out. And producers make decisions based on the total NPV, not the initial year.

I would be more inclined to use the 2015 or 2014 first year productions. After all, the cums do seem to have gone up. What matters is immediate decisions, not old well choices or situation years from now when the rock runs out.

The EOG results are interesting. Wonder if they throttled production or did something strange with pad developments in 2014-5. They have some of the best rock in the basin (at the anticline in Montrail), so was expecting them to look better than they did.

———-

Again nice work and extensive. Take the comments as areas for improving something salvageable.

GregT on Mon, 4th Jan 2016 10:39 pm

“My comments more to help the author fix some things:”

I’m sure that Ron would love to hear your fixes Nony.

No need to register on Peak Oil Barrel. Just you, and Ron.

Nony on Wed, 6th Jan 2016 10:53 am

Come on, man. Don’t put yourself into a position of being the message board boss who tells people where they can/can’t comment. Talk the content, not the person.

It’s a headpost with a comments section. The comments section exists to let people make comments. There is no requirement to shuffle off somewhere else to post. If I choose to comment or not and where that’s with me. And take care of yourself, not me.

P.s. Ron banned me. So he’s NOT interested. But so what. We are here. Discuss the DCF. Nolan did a huge amount of work on it. And I had some relevant crits.

ghung on Wed, 6th Jan 2016 11:25 am

While Ron posted it, it’s a guest post by Ciaran Nolan.

funny shooter 2 on Thu, 6th Apr 2023 9:22 pm

Do not place yourself in a position where you have to tell other people where they may comment and where they can’t comment on the message board. Discuss the topic at hand rather than the individual.