Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on April 1, 2012

A review of the Citigroup Prediction on US Energy

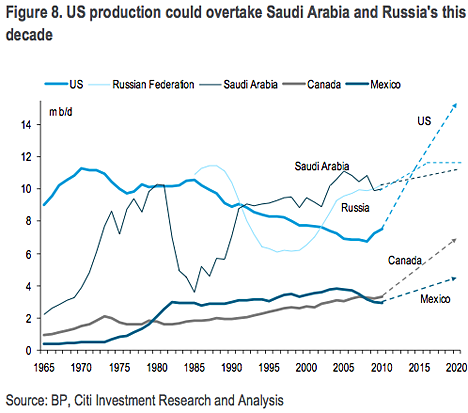

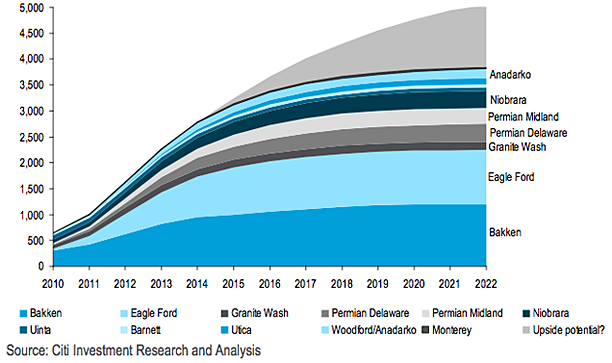

Gasoline prices remain high, and Reuters recently noted that there are enough countries with civil unrest, technical problems, and bad weather with around a million barrels a day of possible supply that are not getting to the market. Yet with Saudi Arabia continuing to reassure that it is willing to pump more oil if needed, there appears to be, superficially, little cause for supply concerns this year. By the same token, concerns over supply in the longer term also seem to be increasingly discounted. For example, Citigroup has just released a new report on Energy 2020: North America as the new Middle East. The report suggests that there is really no concern with future supplies of oil and gas, perhaps most clearly shown with this plot:

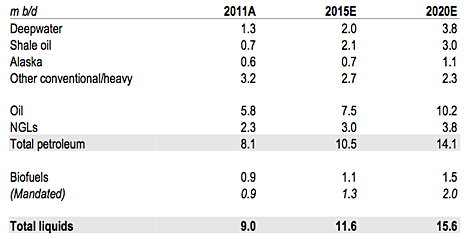

If one examines the prediction for future production, it shows that overall US growth in production of all liquids will rise from some 9 mbd at the end of 2011 to 11.6 mbd in 2015, and then go on to a figure of 15.6 mbd in 2020. Note that this includes natural gas liquids (NGLs), refining gains, and growth in the production of biofuels. The contribution of the various sectors is broken down into:

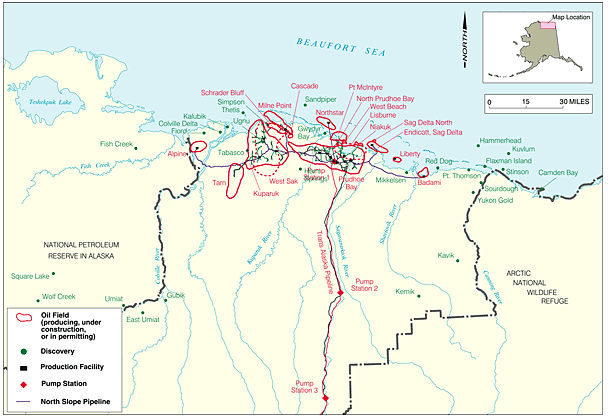

The Citigroup projection for Alaska anticipates possible gains from the Shell activities in the Chukchi Sea, although the exploratory wells have yet to be drilled and the geographical challenges to be met in bringing that oil ashore are not yet fully addressed. The Alaskan pipeline is currently flowing at around 609 kbd, which is high enough to prevent wax and ice build-up, but with ongoing declines in production and problems arising once the flow falls below 600 kbd how long it can continue to perform satisfactorily is open to question. They cite heavy oil operations at Milne Point which has been declining in production, and West Sac, which is a very heavy, cold oil that has raised considerable technical issues in achieving the production of around 15 kbd at present, with existing plans only adding 150 million barrels in total to reserves. The other source that is cited is to produce the light crude is from the National Petroleum Reserve in Alaska (NPRA). Given that the bridge from Alpine into the Conoco-Phillips wells in the NPRA has just been approved suggests that an increase in production from the region is still some time away. Put together, this suggests that the estimates for a 500 kbd increase in Alaskan production within the next eight years is not a reasonably likely occurrence.

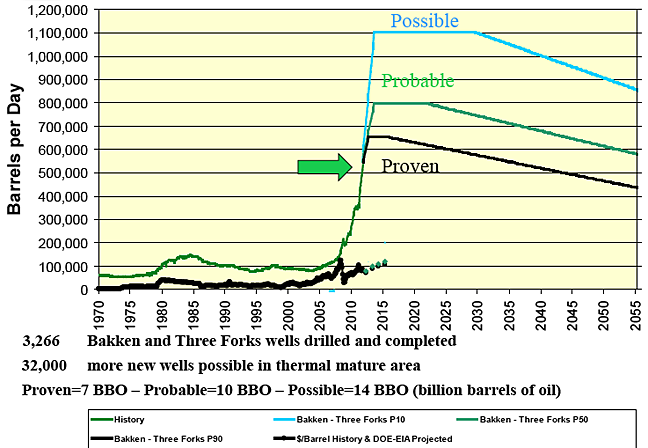

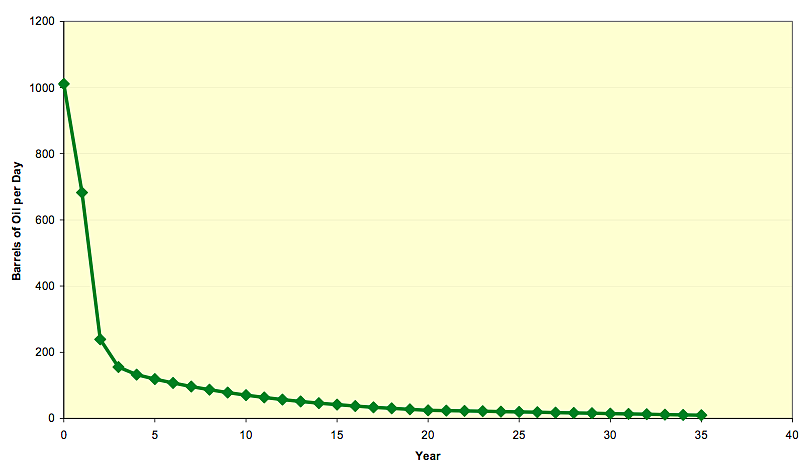

Current plans anticipate that the Niobrara may reach 250 kbd of production by 2020. The problem, however, as Art Berman has skillfully pointed out, is that as the ND plot above shows, the current wells have a high decline rate, and production levels drop dramatically once the wells are brought on line. Art has explained the background to this for gas wells drilled into shale but the impact for oil wells, where the oil has a higher viscosity than the natural gas, can be significantly greater. Given that well costs are in the order of $10 million per well (depending on location DMR gives the ND price at around $8.5 million, and numbers for the Eagle Ford have been quoted at $8 million) the amount of oil that must be produced over the first few years to justify investment is significant. There are, for example, some 1,400 wells producing in the Eagle Ford play. The play produced 30.4 million barrels of oil in 2011, and is anticipated to add 200 kbd of production this year with the potential to reach 1.2 mbd by 2015. But the high decline rates mean that wells must be replaced rapidly to sustain those levels of production.

It is this disregard for the declining production from existing and future wells that appears to be neglected in the Citigroup study. Those plays which will yield rapidly in generating high initial well production will, in turn, be the first that decline significantly and need replacement. Yet replacement will, over time, have to be in poorer parts of the formation, requiring that multiple wells replace the initial producer, and so bounds on production will be reached, likely before the end of the decade. Citigroup anticipates that the risks in development of the shale plays, whether in Texas or California, come as much from an inability to transport the oil generated and from environmental policy; they see few geological risks – which is a pity, since it is the geology that will control production and its decline, and the ultimate profitability of these ventures.

And finally, Citigroup sees that cellulosic ethanol will come into its own this decade, and that it will provide half the 2 mbd of biofuels produced in 2020. Unfortunately the economics of large-scale production that have led to failures of ventures to date have over-ridden the mandated production levels that the group cites as their foundation, and there is no indication that this will change in the next eight years.

In short, though this is an interesting exercise, it is too full of “could” and thus will not make much of a useful contribution to meaningful discussion of future production.

3 Comments on "A review of the Citigroup Prediction on US Energy"

MrEnergyCzar on Mon, 2nd Apr 2012 2:12 am

U.S. energy resources aren’t reserves…

MrEnergyCzar

BillT on Mon, 2nd Apr 2012 2:18 am

Coulda, woulda, shoulda…nothing but guesses, smoke, and hope. Not going to happen. Too many realities in the way. Like a collapsing financial system, pollution lawsuits increasing, unexpected problems, etc. Hype…

pete on Mon, 2nd Apr 2012 3:04 am

As soon as I saw citigroup I puked knowing it’s propaganda or strait out lies.

PLEASE DON”T SEARCH: SANDY ACT GLASS STEAGAL

PLEASE DO NOT GO TO THIS PAGE:

https://en.wikipedia.org/wiki/Robert_Rubin

If any of you saw my SOS smack down on march 31 “chinese firm surpasses exxon in oil production” then you would have seen the comment about “the warning”

but please, ignorance is truly bliss!