Smooth price with a 12 month moving average, using shadowstats inflator; we've been at the plateau for quite a while, and my guess is we stay on it till increases from shale and tar sands fail to keep US/Can production up, the devaluation of the dollar will then overwhelm the stable price as import percentage rises again. I can't convince myself one way or another whether to expect a moderate, sustained rise, or a spike though.

I voted 10 more years on the plateau... There's a *lot* of shale/tar, there's a *lot* of NG to burn through.

PeakOil is You

When do we fall off the undulating plateau? Pt 2

Re: How much longer will the plateau continue?

![]() by AgentR11 » Fri 05 Jul 2013, 12:44:57

by AgentR11 » Fri 05 Jul 2013, 12:44:57

Yes we are, as we are,

And so shall we remain,

Until the end.

And so shall we remain,

Until the end.

- AgentR11

- Light Sweet Crude

- Posts: 6589

- Joined: Tue 22 Mar 2011, 09:15:51

- Location: East Texas

Re: How much longer will the plateau continue?

![]() by dolanbaker » Fri 05 Jul 2013, 14:45:39

by dolanbaker » Fri 05 Jul 2013, 14:45:39

I'm not really sure if the production "plateau" really matters, it's the per-capita availability that matters to the end users and that has been falling for quite some time (mostly through increases in efficiency), the real crunch will be when the cut backs in use are due directly to lack of supply or too high a price.

Religion is regarded by the common people as true, by the wise as false, and by rulers as useful.:Anonymous

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

-

dolanbaker - Intermediate Crude

- Posts: 3855

- Joined: Wed 14 Apr 2010, 10:38:47

- Location: Éire

Re: How much longer will the plateau continue?

![]() by ROCKMAN » Fri 05 Jul 2013, 15:01:32

by ROCKMAN » Fri 05 Jul 2013, 15:01:32

Rollin – “As I sit here in the greatest civilization on earth…” So you live in Texas, eh? Don’t worry about the flicker…probably just the wind knocking the tree limbs against the power lines. LOL.

But seriously it’s not difficult to imagine all the “plateaus” varying between different economies. Just as countries have passed through their individual production plateaus at different times. That’s one of the weaknesses of a pure price plateau analysis: the same price of oil could have greatly different effects on different economies.

And pstarr – “This is the end, my friend”. Always makes me think of that scene from the movie and that napalm in the morning “smells like victory”. Same effect on some folks when they smell vehicle exhaust.

But seriously it’s not difficult to imagine all the “plateaus” varying between different economies. Just as countries have passed through their individual production plateaus at different times. That’s one of the weaknesses of a pure price plateau analysis: the same price of oil could have greatly different effects on different economies.

And pstarr – “This is the end, my friend”. Always makes me think of that scene from the movie and that napalm in the morning “smells like victory”. Same effect on some folks when they smell vehicle exhaust.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: How much longer will the plateau continue?

![]() by Subjectivist » Fri 05 Jul 2013, 19:48:17

by Subjectivist » Fri 05 Jul 2013, 19:48:17

Que sera sera, whatever will be will be.

I can't garuntee anything, as Pupp used to say I am just some guy on the internet, but I dont think it will be much longer before we fall off the plateau.

I can't garuntee anything, as Pupp used to say I am just some guy on the internet, but I dont think it will be much longer before we fall off the plateau.

II Chronicles 7:14 if my people, who are called by my name, will humble themselves and pray and seek my face and turn from their wicked ways, then I will hear from heaven, and I will forgive their sin and will heal their land.

- Subjectivist

- Volunteer

- Posts: 4705

- Joined: Sat 28 Aug 2010, 07:38:26

- Location: Northwest Ohio

Re: How much longer will the plateau continue?

![]() by ralfy » Fri 05 Jul 2013, 23:19:00

by ralfy » Fri 05 Jul 2013, 23:19:00

$this->bbcode_second_pass_quote('John_A', '

')

Cool graphs. Too bad they don't include all the stuff we are actually making liquid fuels out of, and someone correct me if I'm wrong but even in this censored data, is that yet another peak in this particular subset of stuff we make gasoline and diesel out of, right there at the tail end?

')

Cool graphs. Too bad they don't include all the stuff we are actually making liquid fuels out of, and someone correct me if I'm wrong but even in this censored data, is that yet another peak in this particular subset of stuff we make gasoline and diesel out of, right there at the tail end?

Actually, the problem is that we included "all the stuff we are actually making liquid fuels out of," thus assuming that the marginal cost of bringing in new production remains steady. That, of course, is not the case:

http://theautomaticearth.com/Finance/oi ... redit.html

and worsened given economic growth chasing at increasing credit.

Thus, your "basic supply and demand" and simplistic views of the world falls apart.

Censored data.

-

ralfy - Light Sweet Crude

- Posts: 5651

- Joined: Sat 28 Mar 2009, 11:36:38

- Location: The Wasteland

Re: How much longer will the plateau continue?

![]() by westexas » Sat 06 Jul 2013, 14:27:20

by westexas » Sat 06 Jul 2013, 14:27:20

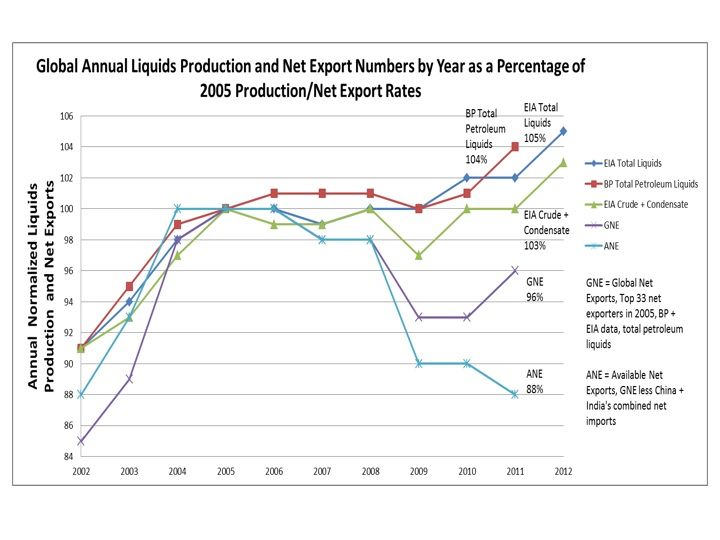

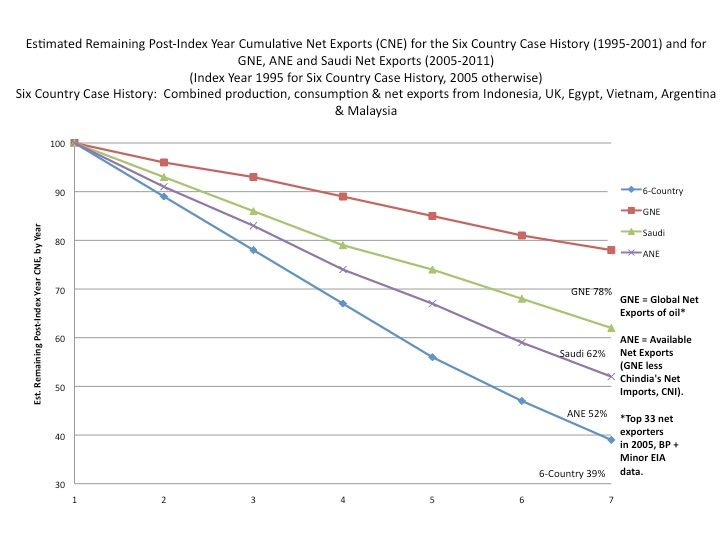

EIA data show Global Net Exports (GNE*) in 2012 were 96% of 2005 rate. Available Net Exports (ANE) in 2012 were down to 86% of 2005 rate:

*Top 33 net oil exporters in 2005

Of course, the real--and almost totally overlooked--story concerns the rates of depletion in post-2005 Global and Available CNE (Cumulative Net Exports). Some estimated post-Index Year CNE depletion rates (Index Year for Six Country Case History is 1995, 2005 otherwise). The Six Country CNE depletion estimate, based on 1995 to 2001 data, was too optimistic.

*Top 33 net oil exporters in 2005

Of course, the real--and almost totally overlooked--story concerns the rates of depletion in post-2005 Global and Available CNE (Cumulative Net Exports). Some estimated post-Index Year CNE depletion rates (Index Year for Six Country Case History is 1995, 2005 otherwise). The Six Country CNE depletion estimate, based on 1995 to 2001 data, was too optimistic.

- westexas

- Expert

- Posts: 248

- Joined: Tue 04 Jun 2013, 06:59:53

Re: How much longer will the plateau continue?

![]() by John_A » Sat 06 Jul 2013, 18:22:33

by John_A » Sat 06 Jul 2013, 18:22:33

So.... is this good.....or bad?

Now that the EIA has seen it, and we know from prior comments that they are using price scenarios in the future upon which to base resource extraction schemes (as Rockman has suggested is a good thing), and they do well level declines and use USGS resource estimates to constrain them, how does this approach help them solve the global "how long will plateau" occur problem?

Certainly their system would seem to be able to predict these kinds of reversals in decline...

so maybe they can now predict the same kinds of things (and accompanying decline) at the world level? Or do they need this estimate of who exports, who imports, how much LESS the US will import in the future because of the kind of production gains shown above, to decide when and if we fall off the plateau?

Now that the EIA has seen it, and we know from prior comments that they are using price scenarios in the future upon which to base resource extraction schemes (as Rockman has suggested is a good thing), and they do well level declines and use USGS resource estimates to constrain them, how does this approach help them solve the global "how long will plateau" occur problem?

Certainly their system would seem to be able to predict these kinds of reversals in decline...

so maybe they can now predict the same kinds of things (and accompanying decline) at the world level? Or do they need this estimate of who exports, who imports, how much LESS the US will import in the future because of the kind of production gains shown above, to decide when and if we fall off the plateau?

45ACP: For when you want to send the very best.

- John_A

- Heavy Crude

- Posts: 1193

- Joined: Sat 25 Jun 2011, 21:16:36

Come off the PO plateau how much gas price increase per year

![]() by mmasters » Fri 20 Jun 2014, 16:17:18

by mmasters » Fri 20 Jun 2014, 16:17:18

When we come off the PO plateau a few years from now how much will we see gas prices increase per year on average?

Factoring in demand destruction my guess is 10-20% per year.

Factoring in demand destruction my guess is 10-20% per year.

-

mmasters - Intermediate Crude

- Posts: 2272

- Joined: Sun 16 Apr 2006, 03:00:00

- Location: Mid-Atlantic

Re: Come off the PO plateau how much gas price increase per

![]() by dolanbaker » Fri 20 Jun 2014, 16:32:52

by dolanbaker » Fri 20 Jun 2014, 16:32:52

Unlikely to happen that way, I expect that prices will stay relatively stable, wage deflation is more likely to happen as things go south. It will be the lack of money that will cause the demand destruction rather than rising prices. Having said that, there will be price spikes that will slam on the "economic" brakes as well.

Religion is regarded by the common people as true, by the wise as false, and by rulers as useful.:Anonymous

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

-

dolanbaker - Intermediate Crude

- Posts: 3855

- Joined: Wed 14 Apr 2010, 10:38:47

- Location: Éire

Re: Come off the PO plateau how much gas price increase per

![]() by farmlad » Fri 20 Jun 2014, 18:12:07

by farmlad » Fri 20 Jun 2014, 18:12:07

with all the excess money that's been printed in the world, and that's a lot a cash, I would just imagine, that as long as people trust in it, it would all be going towards the things that have value/in demand at the time. one being petroleum products. a few more thing that I imagine bringing top prices; anything edible, ammo, sleeping bags, matches, hand tools, machetes. Some things bringing way less than today; real estate, refrigerators, trucks and iphones.

- farmlad

- Peat

- Posts: 94

- Joined: Sun 12 Jan 2014, 21:02:23

Re: Come off the PO plateau how much gas price increase per

![]() by Armageddon » Fri 20 Jun 2014, 19:22:02

by Armageddon » Fri 20 Jun 2014, 19:22:02

Demand destruction will keep happening as the prices continue to rise. Supply is barely keeping up with demand at the current price.

-

Armageddon - Light Sweet Crude

- Posts: 7450

- Joined: Wed 13 Apr 2005, 03:00:00

- Location: St.Louis, Mo

Re: Come off the PO plateau how much gas price increase per

![]() by ROCKMAN » Fri 20 Jun 2014, 21:13:49

by ROCKMAN » Fri 20 Jun 2014, 21:13:49

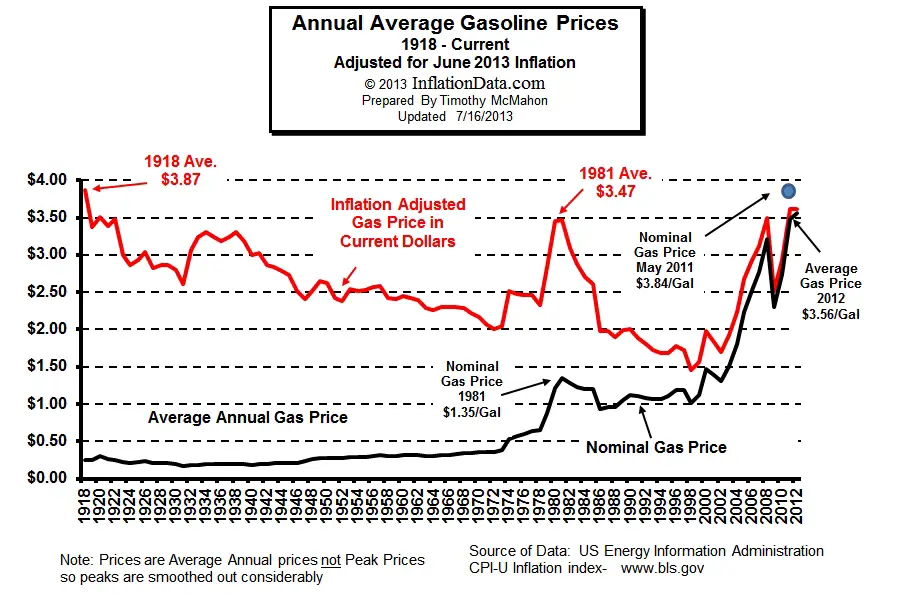

A simpler view: the future price of motor fuel will be more dependent on the condition of the oil consuming economies regardless of plateaus and peaks IMHO. In 1986 fuel prices crashed as oil prices dropped to almost $10/bbl. Adjusted for inflation gasoline prices in 1981 reached about the same level they are today: $3.41/gallon. Does anyone want to argue we were coming off a plateau in the late 70's? And then by 1989 prices fell more than 50% to $1.50/gallon. A surge in oil production above the 80's oil production "plateau"? I think not. And the future? Drive the global economy into another mid-80's recession and we could be looking at gasoline well under $2/gallon. Got a brief taste of that in early 2009 when the adjusted price of fuel dropped to the same level we had in 1952.

One need only gaze at the chart (http://inflationdata.com/Inflation/imag ... ne2013.jpg) a bit to get the point.

One need only gaze at the chart (http://inflationdata.com/Inflation/imag ... ne2013.jpg) a bit to get the point.

{kind=link}

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: Come off the PO plateau how much gas price increase per

![]() by frankthetank » Sat 21 Jun 2014, 00:39:20

by frankthetank » Sat 21 Jun 2014, 00:39:20

I could see where the price spikes, economy plummets, more unemployment/job cuts...less money for the working stiffs..less driving, more demand destruction---price drops some. This would probably be our best bet...a nice slow collapse. If it spikes to $5/$8/$10/gallon in a short time, i think people would just go nuts. Rationing may come back at some point.

lawns should be outlawed.

-

frankthetank - Light Sweet Crude

- Posts: 6202

- Joined: Thu 16 Sep 2004, 03:00:00

- Location: Southwest WI

Re: Come off the PO plateau how much gas price increase per

![]() by vtsnowedin » Sat 21 Jun 2014, 07:15:52

by vtsnowedin » Sat 21 Jun 2014, 07:15:52

I expect the energy corporations to get wise about the decline in supply and stop selling into low demand caused by depressions. Just leaving oil in the ground will be there best investment during such times stretching out their diminishing reserves and only selling product when prices are favorable to them. This should put a hard floor on gas prices say at $4.00 in todays money with no limit on the upper end for military purposes. Consumer prices might well double every five years or so but the trend will be clouded by resource wars and such.

-

vtsnowedin - Fusion

- Posts: 14897

- Joined: Fri 11 Jul 2008, 03:00:00

Re: Come off the PO plateau how much gas price increase per

![]() by Pops » Sat 21 Jun 2014, 08:57:22

by Pops » Sat 21 Jun 2014, 08:57:22

The price can't rise infinitely because there is a finite amount of value that can be generated at any particular time. IOW, money is limited so oil price can't be unlimited.

But there is also switching going on and that keeps the wheels turning for now. Most of the energy switching is to coal and nat gas but there is also switching to automation and little Chinese girls. Global primary energy per capita use had stayed relatively flat at around 1.5 TWH/C from the mid-70's through 2000, but then jumped 15% to 1.75 TWH in the oughties because of increasing coal and nat gas use in China.

Of course in NA & EU primary energy per capita is falling (that is known as the Olduvai Gorge )

)

Check out the BP charting tool

But if supply doesn't grow as fast as the demand increases (the actual population increasing plus the increase in industrial workers entering the oil market, i.e.: China) you have the same unmet demand as if the supply is falling, don't you? Still the oil price has been amazingly stable for three years or more. That argues that the cost is being born somewhere else in the economy. Here is a good picture from Gail showing how US wages flatlined in the '70's and fell outright in the oughties, you can decide the correlation:

There is a price ceiling on this level of oil consumption because the price is completely dependent on the consumers ability to pay. He can conserve and/or switch horses, but he can't pay more for long unless he can increase the utility from each drop and simultaneously maintain his contribution to the economy. One would think some lower amount of consumption would mean a higher possible price. That was the conclusion I came to before: use less-pay more by increasing utility.

But that chart of Gail's seems to say that not only does the worker get to cough up more money to pay for his FFs, he also gets to pay for the increase in his bosses' fuel bill as well. That is the pretty obvious reason (along with free Fed money of course) that GDP and the 1% are doing so well while the average guy ain't. And one more reason the price can't rise indefinitely.

So I guess my point is, "how fast will price rise" is the wrong question. The right question is:

"How long will I be able to pay any price?"

http://ourfiniteworld.com/2013/02/14/th ... to-growth/

But there is also switching going on and that keeps the wheels turning for now. Most of the energy switching is to coal and nat gas but there is also switching to automation and little Chinese girls. Global primary energy per capita use had stayed relatively flat at around 1.5 TWH/C from the mid-70's through 2000, but then jumped 15% to 1.75 TWH in the oughties because of increasing coal and nat gas use in China.

Of course in NA & EU primary energy per capita is falling (that is known as the Olduvai Gorge

)Check out the BP charting tool

But if supply doesn't grow as fast as the demand increases (the actual population increasing plus the increase in industrial workers entering the oil market, i.e.: China) you have the same unmet demand as if the supply is falling, don't you? Still the oil price has been amazingly stable for three years or more. That argues that the cost is being born somewhere else in the economy. Here is a good picture from Gail showing how US wages flatlined in the '70's and fell outright in the oughties, you can decide the correlation:

There is a price ceiling on this level of oil consumption because the price is completely dependent on the consumers ability to pay. He can conserve and/or switch horses, but he can't pay more for long unless he can increase the utility from each drop and simultaneously maintain his contribution to the economy. One would think some lower amount of consumption would mean a higher possible price. That was the conclusion I came to before: use less-pay more by increasing utility.

But that chart of Gail's seems to say that not only does the worker get to cough up more money to pay for his FFs, he also gets to pay for the increase in his bosses' fuel bill as well. That is the pretty obvious reason (along with free Fed money of course) that GDP and the 1% are doing so well while the average guy ain't. And one more reason the price can't rise indefinitely.

So I guess my point is, "how fast will price rise" is the wrong question. The right question is:

"How long will I be able to pay any price?"

http://ourfiniteworld.com/2013/02/14/th ... to-growth/

The legitimate object of government, is to do for a community of people, whatever they need to have done, but can not do, at all, or can not, so well do, for themselves -- in their separate, and individual capacities.

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-

Pops - Elite

- Posts: 19746

- Joined: Sat 03 Apr 2004, 04:00:00

- Location: QuikSac for a 6-Pac

Re: Come off the PO plateau how much gas price increase per

![]() by ROCKMAN » Sat 21 Jun 2014, 13:13:18

by ROCKMAN » Sat 21 Jun 2014, 13:13:18

Vt - "I expect the energy corporations to get wise about the decline in supply and stop selling into low demand caused by depressions. Just leaving oil in the ground will be there best investment during such times stretching out their diminishing reserves and only selling product when prices are favorable to them." As I've said before I wish that were true. But such "wisdom" doesn't change the demand for cash flow. Been doing this 4 decades now and have seen numerous dips in oil/NG prices...some small...some huge. And the industry wide response has always been the same: reduce spending and do whatever possible to INCREASE production. When NG fell a few years ago my company was one of the few that voluntarily cut production. Being private and owned by a billionaire we could handle the decrease in revenue. Few companies, especially pubcos with big debt burdens to satisfy, could deal with lower revenue levels.

It's like you getting a pay cut and deciding you'll adjust by not sending your mortgage company full payment. You might skim by for a while but not for years waiting for your next raise. And if your grocer is like mine you're not going to negotiate with the checkout lady what you'll pay for that basket of food. LOL.

It's like you getting a pay cut and deciding you'll adjust by not sending your mortgage company full payment. You might skim by for a while but not for years waiting for your next raise. And if your grocer is like mine you're not going to negotiate with the checkout lady what you'll pay for that basket of food. LOL.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: Come off the PO plateau how much gas price increase per

![]() by Pops » Sat 21 Jun 2014, 13:46:22

by Pops » Sat 21 Jun 2014, 13:46:22

$this->bbcode_second_pass_quote('ROCKMAN', 'I')t's like you getting a pay cut and deciding you'll adjust by ...

... cutting back on your hours.

The legitimate object of government, is to do for a community of people, whatever they need to have done, but can not do, at all, or can not, so well do, for themselves -- in their separate, and individual capacities.

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-

Pops - Elite

- Posts: 19746

- Joined: Sat 03 Apr 2004, 04:00:00

- Location: QuikSac for a 6-Pac

Re: Come off the PO plateau how much gas price increase per

![]() by ROCKMAN » Sat 21 Jun 2014, 14:29:07

by ROCKMAN » Sat 21 Jun 2014, 14:29:07

Pops - My personal experience is just the opposite. When the 80's bust hit the oil patch I was working 80+ hours a week and still couldn't keep up with debt service. Waited till I had less than $300 left before filling bankruptcy. The only comment the judge made was that I should have filled sooner when I had more resources. Told him I just wanted to pay my debts as long as had some money. Of course he looked at me like I was nuts. LOL.

So young geologists do the same as the gov't does: borrow money thinking the good times will keep rolling along. Thank Dog I'm no longer a young geologist. LOL.

So young geologists do the same as the gov't does: borrow money thinking the good times will keep rolling along. Thank Dog I'm no longer a young geologist. LOL.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: Come off the PO plateau how much gas price increase per

![]() by vtsnowedin » Sat 21 Jun 2014, 17:33:29

by vtsnowedin » Sat 21 Jun 2014, 17:33:29

$this->bbcode_second_pass_quote('ROCKMAN', '&')quot; As I've said before I wish that were true. But such "wisdom" doesn't change the demand for cash flow. Been doing this 4 decades now and have seen numerous dips in oil/NG prices...some small...some huge. And the industry wide response has always been the same: reduce spending and do whatever possible to INCREASE production. When NG fell a few years ago my company was one of the few that voluntarily cut production. Being private and owned by a billionaire we could handle the decrease in revenue. Few companies, especially pubcos with big debt burdens to satisfy, could deal with lower revenue levels.

It's like you getting a pay cut and deciding you'll adjust by not sending your mortgage company full payment. You might skim by for a while but not for years waiting for your next raise. And if your grocer is like mine you're not going to negotiate with the checkout lady what you'll pay for that basket of food. LOL.

I've watched the same thing happen a couple of times from the consumers point of view and understand what your saying. But in all those previous recessions and depressions there were other sources to explore and develop. The North Sea, The north slope of Alaska, Deep water GOM etc. I think soon they will run out of places to look that hold any real promise and the reserves they have in hand will be recognized as being all there ever is going to be. With that realization will come a change in thinking and strategy.It's like you getting a pay cut and deciding you'll adjust by not sending your mortgage company full payment. You might skim by for a while but not for years waiting for your next raise. And if your grocer is like mine you're not going to negotiate with the checkout lady what you'll pay for that basket of food. LOL.

-

vtsnowedin - Fusion

- Posts: 14897

- Joined: Fri 11 Jul 2008, 03:00:00

Re: Come off the PO plateau how much gas price increase per

![]() by Pops » Sat 21 Jun 2014, 19:01:46

by Pops » Sat 21 Jun 2014, 19:01:46

LOL, my point was if oil cos saw a drop in price, reducing production would be like a wage earner cutting hours in response to a wage cut.

The legitimate object of government, is to do for a community of people, whatever they need to have done, but can not do, at all, or can not, so well do, for themselves -- in their separate, and individual capacities.

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-

Pops - Elite

- Posts: 19746

- Joined: Sat 03 Apr 2004, 04:00:00

- Location: QuikSac for a 6-Pac

Who is online

Users browsing this forum: No registered users and 3 guests