PeakOil is You

Status of dollar as world currency threatened

Re: Status of dollar as world currency threatened

![]() by I_Like_Plants » Mon 28 Jan 2008, 15:19:12

by I_Like_Plants » Mon 28 Jan 2008, 15:19:12

I was talking to some people who'd been in Mexico when 9-11 happened, (remember kids that was in 2001). The Mexicans would not take their dollars, and they had a bit of trouble getting out of there. I get the impression they were kind of stuck where they were until the PPT etc did their job Stateside and the Mexicans could be conned into changing worthless USbucks for good Pesos again.

- I_Like_Plants

- Intermediate Crude

- Posts: 3839

- Joined: Sun 12 Jun 2005, 03:00:00

- Location: 1st territorial capitol of AZ

Re: Status of dollar as world currency threatened

![]() by cube » Tue 29 Jan 2008, 03:55:31

by cube » Tue 29 Jan 2008, 03:55:31

$this->bbcode_second_pass_quote('Petrodollar', '.')..Soros is right, the decline of the dollar will move the world towards a multipolar world order, with 3 major poles of power.

silly Q?

Will the USA be in one of those poles?

Europe, Chindia, Russia?

- cube

- Intermediate Crude

- Posts: 3909

- Joined: Sat 12 Mar 2005, 04:00:00

Re: Status of dollar as world currency threatened

![]() by MrBill » Tue 29 Jan 2008, 05:46:42

by MrBill » Tue 29 Jan 2008, 05:46:42

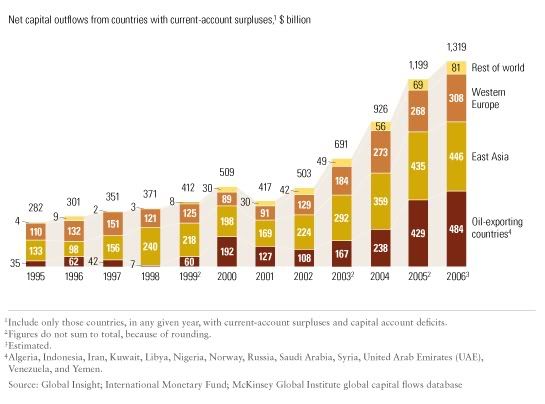

Current Account Surpluses = Current Account Deficits

Global Trade Deficit = Global Trade Surplus

Balance of Payments = Income Earned Abroad - Income Paid Abroad

For all the blather about the end of the US dollar as a reserve currency, I see Total Reserves increasing, and a diversification away from US dollar accumulation, but I see no reduction in the amount of US dollars in central bank reserves.

The informal Bretton Woods II agreement between America and its creditors almost guarantees that anyone who breaks ranks and lets their own currency appreciate faster than others will lose exports and suffer a slowdown of their own. There is no sign of decoupling. Period.

$this->bbcode_second_pass_quote('', ' ')PetroChina's 44% Loss Proves BRIC Premium Is Nonsense

The biggest slide in emerging-market stock valuations in a year and a half is proving that a slowdown in the U.S. economy still matters to Brazil, Russia, India and China.

Shares in the MSCI Emerging Markets Index dropped 12 percent relative to profit this month as the prospect of a U.S. recession pushed two-thirds of the world's equity indexes into so-called bear markets. The last monthly decline as steep was in May 2006, according to data compiled by Bloomberg. Even the price-earnings ratio for the Standard & Poor's 500 Index, the benchmark for U.S. stocks, didn't fall as much.

Companies such as PetroChina Co., the country's biggest oil producer, and Russia's OAO Lukoil show the threat of a global slump is shaking the confidence of investors who viewed developing countries as a haven from the U.S. PetroChina's 44 percent plummet since November erased about $400 billion, more than the market value of Microsoft Corp., the No. 1 software maker. Russian stocks are headed for their biggest loss in 19 months after money managers bought an unprecedented amount in 2007.

``The only way they could decouple would be for them to be on another planet,'' said David Dreman, who oversees $20 billion as chief investment officer at Jersey City, New Jersey-based Dreman Value Management LLC. ``We are the biggest buyer of their products and biggest user of their services, so if our economy slows down their growth rate has to slow down. There's no other plausible way.''

Global Trade Deficit = Global Trade Surplus

Balance of Payments = Income Earned Abroad - Income Paid Abroad

- therefore, if you reduce the deficits you automatically reduce the surpluses - that is a fact!

For all the blather about the end of the US dollar as a reserve currency, I see Total Reserves increasing, and a diversification away from US dollar accumulation, but I see no reduction in the amount of US dollars in central bank reserves.

The informal Bretton Woods II agreement between America and its creditors almost guarantees that anyone who breaks ranks and lets their own currency appreciate faster than others will lose exports and suffer a slowdown of their own. There is no sign of decoupling. Period.

$this->bbcode_second_pass_quote('', ' ')PetroChina's 44% Loss Proves BRIC Premium Is Nonsense

The biggest slide in emerging-market stock valuations in a year and a half is proving that a slowdown in the U.S. economy still matters to Brazil, Russia, India and China.

Shares in the MSCI Emerging Markets Index dropped 12 percent relative to profit this month as the prospect of a U.S. recession pushed two-thirds of the world's equity indexes into so-called bear markets. The last monthly decline as steep was in May 2006, according to data compiled by Bloomberg. Even the price-earnings ratio for the Standard & Poor's 500 Index, the benchmark for U.S. stocks, didn't fall as much.

Companies such as PetroChina Co., the country's biggest oil producer, and Russia's OAO Lukoil show the threat of a global slump is shaking the confidence of investors who viewed developing countries as a haven from the U.S. PetroChina's 44 percent plummet since November erased about $400 billion, more than the market value of Microsoft Corp., the No. 1 software maker. Russian stocks are headed for their biggest loss in 19 months after money managers bought an unprecedented amount in 2007.

``The only way they could decouple would be for them to be on another planet,'' said David Dreman, who oversees $20 billion as chief investment officer at Jersey City, New Jersey-based Dreman Value Management LLC. ``We are the biggest buyer of their products and biggest user of their services, so if our economy slows down their growth rate has to slow down. There's no other plausible way.''

Source: Jan. 28 (Bloomberg)

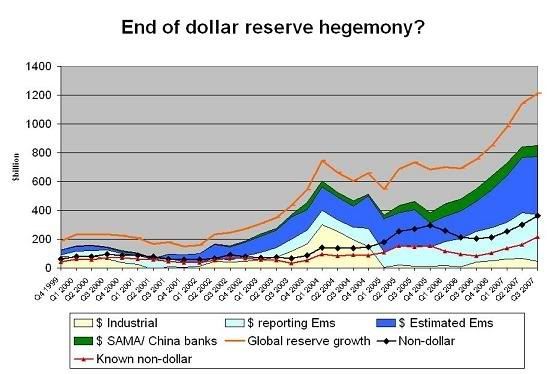

The fact that China and others are diversifying into the euro just shifts those exports of goods AND capital onto the backs of European manufacturers. Not politically acceptable to European Finance Ministers and politicians. Also not sustainable in the long-run.

What would be sustainable in the long-run is if these exporters were truly willing to let their own currencies appreciate - as opposed to just verbally criticizing a weak US dollar, which their own currency manipulation has enabled - and repatriate those export receipts into their own domestic economies and local capital markets.

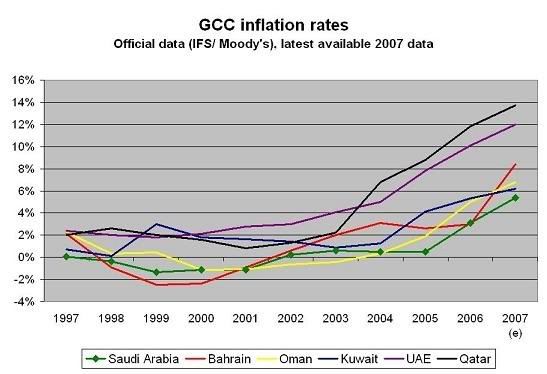

GCC domestic inflation

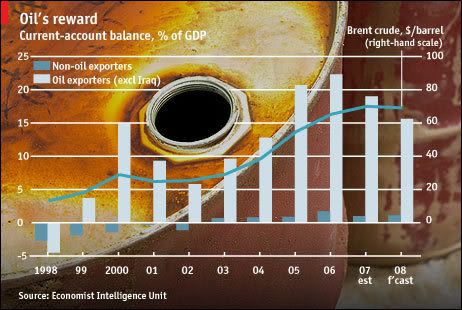

The fact is that the US needs a weaker US dollar to close its trade and budget deficit gap. However, due to the perverse effects of the informal Bretton Woods II agreement, instead of the US dollar losing ground against stronger currencies to address those imbalances, it is actually forced to devalue against currencies that are already artificially weak - on a trade-weighted basis - as OPEC and non-OPEC oil producers and Asian manufacturers try vainly to keep their own currencies down and export competitive through foreign currency sterilization. That is inflationary for the global economy in the medium to long-term. As is clearly visible from this graph on money supply growth.

The same old tired, one-sided arguments every single time. Your data does not match your rhetoric - as usual!

The organized state is a wonderful invention whereby everyone can live at someone else's expense.

-

MrBill - Expert

- Posts: 5630

- Joined: Thu 15 Sep 2005, 03:00:00

- Location: Eurasia

Re: Status of dollar as world currency threatened

![]() by Euric » Fri 15 Feb 2008, 01:47:24

by Euric » Fri 15 Feb 2008, 01:47:24

$this->bbcode_second_pass_quote('MrBill', '

')

The same old tired, one-sided arguments every single time. Your data does not match your rhetoric - as usual!

')

The same old tired, one-sided arguments every single time. Your data does not match your rhetoric - as usual!

I see Mr. Bill thinks that posting a few fictional charts makes him right and everyone else wrong. What Mr. Bill fails to understand is that those who provide the "data" to make those charts don't always provide truthful information. Also data can be manipulated to provide any desired result.

The Chinese and others who wish to divest of their dollar reserves can do so quietly so as not to arouse attention by the US or world markets. If you want to dump your dollars and not cause a panic too early before you get rid of your last cent, you don't announce it and you continue to tell everyone you are not divesting of existing reserves.

-

Euric - Tar Sands

- Posts: 622

- Joined: Sat 04 Dec 2004, 04:00:00

Re: Status of dollar as world currency threatened

![]() by Plantagenet » Fri 15 Feb 2008, 02:01:21

by Plantagenet » Fri 15 Feb 2008, 02:01:21

$this->bbcode_second_pass_quote('Euric', '')$this->bbcode_second_pass_quote('MrBill', '

')

The same old tired, one-sided arguments every single time. Your data does not match your rhetoric - as usual!

')

The same old tired, one-sided arguments every single time. Your data does not match your rhetoric - as usual!

I see Mr. Bill thinks that posting a few fictional charts makes him right and everyone else wrong.

Mr. Bill is a valuable source of current information on both economic data and its interpretation.

There is no point in pretending his charts are "fictional" when Mr. Bill clearly shows the sources of his data.

THANKS Mr. Bill!!!!

-

Plantagenet - Expert

- Posts: 26765

- Joined: Mon 09 Apr 2007, 03:00:00

- Location: Alaska (its much bigger than Texas).