$this->bbcode_second_pass_quote('PeakOilDebunked', 'I')t's official. Peak oil is a loser. It blew a tire on the curve, and lost the TEOTWAWKI 500 to the ongoing US financial meltdown. Valiant efforts are being made at the peak oil sites to maintain interest and somehow blame the collapse on oil, or at least find some flimsy connection... to no avail. The PO community is looking increasingly like the village idiot who warned everybody about the tornado, just before the big flood hit.

Now that most of Wall Street has been vaporized, peak oil isn't going to be the hot cottage industry it once was. The groupies will now shift to the real rockstars of the global collapse blogosphere -- the finance doomers. Pity the poor peak oil sites... viewers melting away like the Greenland icesheet, page views slumping like WaMu stock...

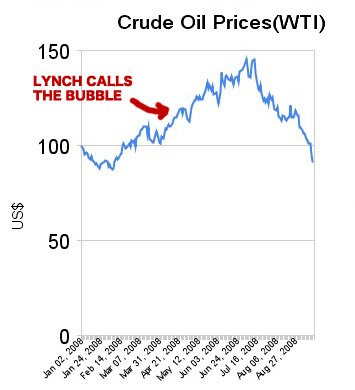

Amidst the carnage, we can single out one man for some well-deserved kudos. That would be Mike Lynch, who called oil "the mother of all bubbles" on April 21.

PeakOil is You

Peak Oil: Who Cares?

Peak Oil: Who Cares?

![]() by Carlhole » Mon 27 Oct 2008, 09:41:59

by Carlhole » Mon 27 Oct 2008, 09:41:59

[align=center]

[/align]

[/align]$this->bbcode_second_pass_quote('', 'N')ice job, Mike. I'll take you out for some octopus balls if you're ever in Osaka. Of course, the peak oilers adamantly refuse to admit that oil was a bubble. They stand ready to defend peak oil at all costs, even if nobody else gives a shit anymore. When Jerome a Paris carefully explains why his "Countdown to $200 oil" series is still relevant, even though oil prices fell off a cliff, and the US banking system imploded, the peak oil die-hards will dutifully nod their heads and hit the +1 button.

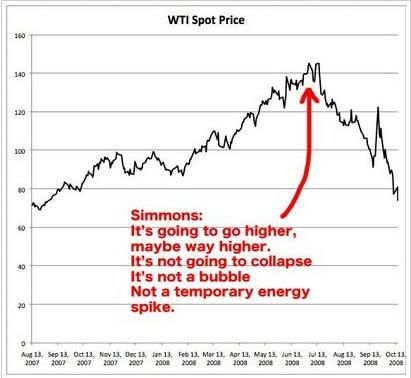

Of course sane regular Joes like you and me know what's up. We know for a fact oil was a bubble because we looked at the fucking picture.

No one's ever going to believe me, but I swear I've only checked John Denver's blog maybe once or twice in the past 4 years. But I just checked it out again now to see what JD might have written about oil's plunge and the world economic crisis, and found that PeakOilDebunked is pretty damn entertaining!

And JD writes in a faintly Onion-esque way about the foibles of the Doomers which makes me chuckle. His whole blog should be part of THIS site IMO.

Don't get me wrong... I'm very much interested in energy and recognize it as fundamental to everything else. But the whole Doom thing never really grabbed me as likely. I was always more keenly interested in the geopolitical goings-on - US motives in Iraq and Central Asia and all that.

The end of civilization dogma around here strikes me as a total juvenile fantasy trip.

[align=center]

[/align]

[/align]- Carlhole

Re: Peak Oil: Who Cares?

![]() by RSFB » Mon 27 Oct 2008, 10:19:30

by RSFB » Mon 27 Oct 2008, 10:19:30

$this->bbcode_second_pass_quote('', 'P')eak Oil: Who Cares?

Those who know that the world will most likely need oil to recover from the recession/depression.

Those who are worried about low investment in renewables and oil exploration / drilling.

Those who are not taking this financial crisis as an excuse to mock peak oil and other related theories and problems.

-

RSFB - Lignite

- Posts: 309

- Joined: Sun 03 Aug 2008, 03:00:00

Re: Peak Oil: Who Cares?

![]() by seahorse2 » Mon 27 Oct 2008, 10:21:17

by seahorse2 » Mon 27 Oct 2008, 10:21:17

1. World oil production essentially peaked/plateaued at about 85mbpd. Do you think that plateau was geologic limit?

2. World oil production essentially peaked/plateaued in 2005 at about 85mbpd while world GDP was growing (increasing demand for energy). Do you think that plateau in oil production was a cause of the high oil/energy prices or do you think it was just speculation?

3. There are questions on this forum about the effect of lower oil prices on oil production. As you know, existing fields are in decline. Those declines have to be offset by new production, unless of course, world oil demand drops faster than declines in existing fields. Do you think world oil demand will drop faster than declines in existing fields?

4. I personally wonder whether lower oil prices will exacerbate the oil production limits we seemed to be reaching. My own beliefs were that a geologic peak in oil production would not occur until about 2012 - 2014, assuming demand increased at the predicted rates. The problem with dropping demand and dropping oil prices seems to be that necessary investment in new oil production in offshore fields and harder to reach develop places will not occur, and thus, oil production will in fact decline bc existing fields will decline. It seems plausible to me we could get a feedback loop where demand for oil and declines in existing fields "race for the bottom" causing serious economic harm.

5. You assume that the recession or developing depression is not related to energy prices and a plateau in oil production. Assuming this is true, you then draw the conclusion that the "doomer fantasies" have been avoided. How is that? The classic doomer arguments always argued that a drop in world oil production would cause a depression. A depression is a depression is it not? How is a recession or a depression ever a good thing?

2. World oil production essentially peaked/plateaued in 2005 at about 85mbpd while world GDP was growing (increasing demand for energy). Do you think that plateau in oil production was a cause of the high oil/energy prices or do you think it was just speculation?

3. There are questions on this forum about the effect of lower oil prices on oil production. As you know, existing fields are in decline. Those declines have to be offset by new production, unless of course, world oil demand drops faster than declines in existing fields. Do you think world oil demand will drop faster than declines in existing fields?

4. I personally wonder whether lower oil prices will exacerbate the oil production limits we seemed to be reaching. My own beliefs were that a geologic peak in oil production would not occur until about 2012 - 2014, assuming demand increased at the predicted rates. The problem with dropping demand and dropping oil prices seems to be that necessary investment in new oil production in offshore fields and harder to reach develop places will not occur, and thus, oil production will in fact decline bc existing fields will decline. It seems plausible to me we could get a feedback loop where demand for oil and declines in existing fields "race for the bottom" causing serious economic harm.

5. You assume that the recession or developing depression is not related to energy prices and a plateau in oil production. Assuming this is true, you then draw the conclusion that the "doomer fantasies" have been avoided. How is that? The classic doomer arguments always argued that a drop in world oil production would cause a depression. A depression is a depression is it not? How is a recession or a depression ever a good thing?

-

seahorse2 - Expert

- Posts: 2042

- Joined: Mon 18 Oct 2004, 03:00:00

Re: Peak Oil: Who Cares?

![]() by VMarcHart » Mon 27 Oct 2008, 10:36:58

by VMarcHart » Mon 27 Oct 2008, 10:36:58

$this->bbcode_second_pass_quote('PeakOilDebunked', 'T')he PO community is looking increasingly like the village idiot who warned everybody about the tornado, just before the big flood hit.

That may be a fair comparison. I don't know. But wasn't the flood, like the tornado, caused because of bad weather which was caused excessive use of oil?

Granted, the PO community had an emphasis on oil, but the PO community was right on saying things will change for worse, and they did, ie, the financial bubble.

On 9/29/08, cube wrote: "The Dow will drop to 4,000 within 2 years". The current tally is 239 bold predictions, 9 right, 96 wrong, 134 open. If you've heard here, it's probably wrong.

-

VMarcHart - Heavy Crude

- Posts: 1644

- Joined: Mon 26 May 2008, 03:00:00

- Location: Now overpopulating California