PeakOil is You

What's up with the Repo rate?

Re: What's up with the Repo rate?

![]() by GHung » Wed 30 Oct 2019, 13:54:57

by GHung » Wed 30 Oct 2019, 13:54:57

$this->bbcode_second_pass_quote('', 'T')he US government has no problem meeting its debt obligations currently nor do most countries which was why I asked the question which countries were at risk of default. But apparently since you didn't understand the conversation you wanted to change topics.

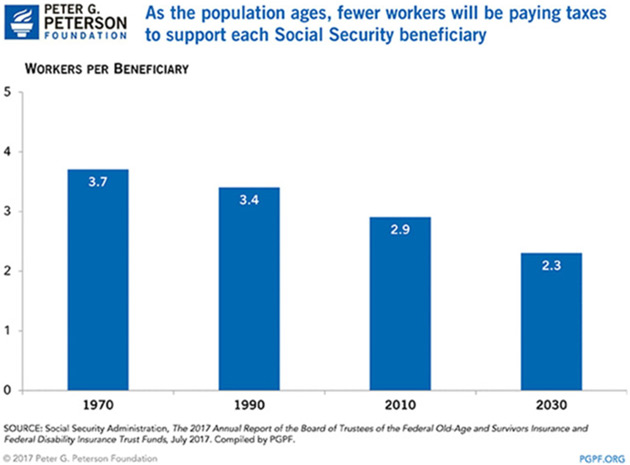

It's all part and parcel of the same economy. If individuals aren't in a position to pay the taxes, where TF will the Federal Government get the revenues to pay the interest on $22+ trillion (and rising) debt???

$this->bbcode_second_pass_quote('', 'N')ot sure why you would want to bring up my own debt situation as I have none, haven't had any for a couple of decades. I buy what I need and what I can afford. If everyone did that they wouldn't have a problem either.

I also have zero debt, but that is not the case for most Americans. Not a problem??? YET. But in your extremely obtuse manner, you choose to ignore the link I provided that shows that debt WILL become a problem for many if things continue as they are (either way in reality) .....

https://www.forbes.com/sites/johnmauldi ... e598f37fc5

Maybe all of these non-geologists are wrong.

.... and that's just a reference to Social Security. The declining work participation rate + an aging populace will affect all sectors of our highly leveraged economy, along with declining overall purchasing power, government services being cut, increasing healthcare costs,,,, I could go on, but methinks your mastery of self-delusion is complete. So go about your business and stop pretending the rest of us are, as you've called so many of us, "morons".

And Billionaires' schemes? Really? They'll suck up your wealth as well because that's all they'll have left to take. You're nothing but a piss-ant to them.

You really are utterly out of touch with how the other ~300+ billion live.

Implying that it's THEIR problem is indicative of deep socioapathy and a lack of systemic thinking.

Blessed are the Meek, for they shall inherit nothing but their Souls. - Anonymous Ghung Person

-

GHung - Intermediate Crude

- Posts: 3093

- Joined: Tue 08 Sep 2009, 16:06:11

- Location: Moksha, Nearvana

Re: What's up with the Repo rate?

![]() by Outcast_Searcher » Wed 30 Oct 2019, 15:20:50

by Outcast_Searcher » Wed 30 Oct 2019, 15:20:50

$this->bbcode_second_pass_quote('GHung', '')$this->bbcode_second_pass_quote('', 'T')he US government has no problem meeting its debt obligations currently nor do most countries which was why I asked the question which countries were at risk of default. But apparently since you didn't understand the conversation you wanted to change topics.

It's all part and parcel of the same economy. If individuals aren't in a position to pay the taxes, where TF will the Federal Government get the revenues to pay the interest on $22+ trillion (and rising) debt???

But there is a painfully obvious solution, which doomers of most stripes steadfastly refuse to consider.

Lower living standards.

Which are NOT doom, by the way, they are simply lower living standards, overall. (Despite the claims of doomers, the vast majority of first worlders are NOT on the edge of starvation or anything remotely close to that).

If it's insane for the average new car transaction price in the US to be over $37K (per Kelly Blue Book), so the average buyer can have a REALLY FANCY ride with numerous bells and whistles, they COULD always buy a good used car in the same class for about half or less, or they COULD buy a smaller and far more practical car with a MUCH less total cost of ownership. (I would say that figure IS insane, BTW. My last new car transaction price (in 2017) including an 8 year extended warranty was about $23K, for by far, the nicest car I've ever had, and all the car I could possibly WANT, much less need).

https://www.boston.com/cars/car-news/20 ... r-may-2019

They might not LIKE it. And politicians might not force it on them until push comes to shove, but it most certainly wouldn't kill them.

Now, multiply that example by quite a few, for the typical first world lifestyle, and there you go.

The irony is that generally, frugal people who make it a lifestyle choice to carry little to no debt and therefore live WELL within their means, already know this. They tend to be FAR richer than they look, and my guess is they tend to sleep far better at night, as one class of American living "problems" (problems with money) is something they don't have to a large extent. (You need food, housing, and medical care. You do NOT need much of the CRAP people think they want).

Taxes could be raised, and pissed off Americans living more frugally by government decree would, perhaps, FORCE government to be far more frugal re things like defense spending and endlessly trying to grow give-away programs, by refusing to vote for politicians who don't behave more in line with what they demand.

Not saying it's likely to be soon, but it sure as hell beats total economic destruction and all the consequences of that -- and despite all the endless doomer ranting, I think it's a FAR more likely outcome, given all the facts on the ground, and the history of economic theory and human behavior.

....

Now I'm sure the fast crash doomers can tell me why this can't possibly be so, and why re THIS, their accuracy will be SO much better than their near zero track record re doom doom doom.

(And be wrong yet again, of course). OTOH, the gradual descent doomers like KJ may well have this sort of thing as part of their vision for a decline on the scale of hundreds of years, which is already underway. One example: Social Security and Medicare have already had small cuts re games with inflation calculations for the COLA's, extra taxes for medicare benefits re MODIFIED adjusted gross income, etc. So it's not like this isn't already happening to some extent -- it's just slow enough thus far that it's not obvious if you're not paying fairly close attention.

Given the track record of the perma-doomer blogs, I wouldn't bet a fast crash doomer's money on their predictions.

-

Outcast_Searcher - COB

- Posts: 10142

- Joined: Sat 27 Jun 2009, 21:26:42

- Location: Central KY

Given that I don't, I prefer to look at the real world data from the experts at the Fed instead.

Given that I don't, I prefer to look at the real world data from the experts at the Fed instead.