PeakOil is You

Peak?

Re: Peak?

![]() by Pops » Fri 18 Sep 2015, 12:29:09

by Pops » Fri 18 Sep 2015, 12:29:09

$this->bbcode_second_pass_quote('Subjectivist', 'W')hat do you think about the shale loan crisis that seems to be shaping up?

I think the resource and capital assets don't go away. The company may go away, it's debts may be assumed or restructured or just written off (trump says bankruptcy is the American way, LOL) but the assets are still in the ground and capital improvements still on top.

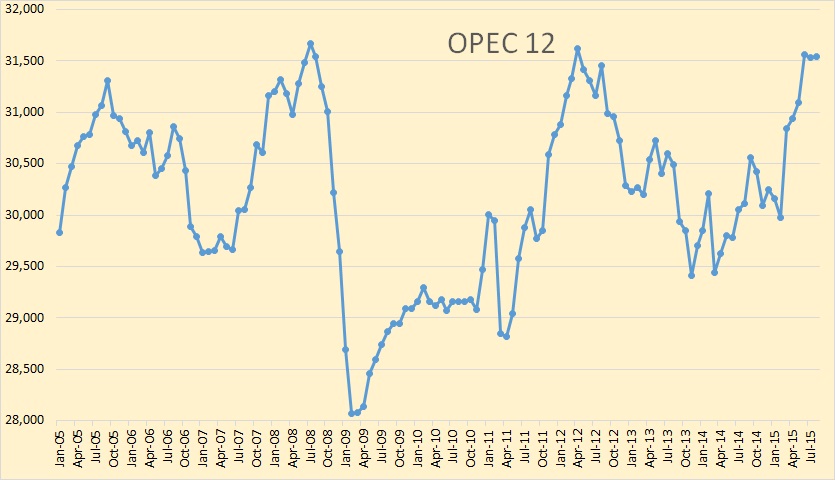

The current surplus is from overproduction. Once the excess clears and the price recovers, some new guy will come along and take up where the last guy left off unless we miraculously decided we don't want oil any more.

My copyrighted rule of thumb is $1/mbd of total supply, so if we want 95mbd we will need to pay $95/bbl. If we want something less we can pay less, I don't see that happening without a recession.

The hitch in that scenario is still, just the same as ever, geologic constraints in conventional oil. 4 years of the highest oil prices and investment ever barely replaced C+C depletion - and likely mostly of the replacement is due to an increase in the second C, condensate. Which ain't nothin' but ain't crude.

When investment can't replace conventional depletion, that is peak.

The legitimate object of government, is to do for a community of people, whatever they need to have done, but can not do, at all, or can not, so well do, for themselves -- in their separate, and individual capacities.

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-- Abraham Lincoln, Fragment on Government (July 1, 1854)

-

Pops - Elite

- Posts: 19746

- Joined: Sat 03 Apr 2004, 04:00:00

- Location: QuikSac for a 6-Pac

Re: Peak?

![]() by Tanada » Fri 18 Sep 2015, 15:55:46

by Tanada » Fri 18 Sep 2015, 15:55:46

$this->bbcode_second_pass_quote('Pops', 'M')y copyrighted rule of thumb is $1/mbd of total supply, so if we want 95mbd we will need to pay $95/bbl. If we want something less we can pay less, I don't see that happening without a recession.

The hitch in that scenario is still, just the same as ever, geologic constraints in conventional oil. 4 years of the highest oil prices and investment ever barely replaced C+C depletion - and likely mostly of the replacement is due to an increase in the second C, condensate. Which ain't nothin' but ain't crude.

When investment can't replace conventional depletion, that is peak.

The hitch in that scenario is still, just the same as ever, geologic constraints in conventional oil. 4 years of the highest oil prices and investment ever barely replaced C+C depletion - and likely mostly of the replacement is due to an increase in the second C, condensate. Which ain't nothin' but ain't crude.

When investment can't replace conventional depletion, that is peak.

Personally given that the big oil companies were cancelling projects left and right even when oil was $100/bbl it sure seems like conventional has peaked, but what do I know I am just a typed messages floating around the internet.

$this->bbcode_second_pass_quote('Alfred Tennyson', 'W')e are not now that strength which in old days

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.

- Tanada

- Site Admin

- Posts: 17094

- Joined: Thu 28 Apr 2005, 03:00:00

- Location: South West shore Lake Erie, OH, USA

Re: Peak?

![]() by PeakOiler » Fri 18 Sep 2015, 18:54:43

by PeakOiler » Fri 18 Sep 2015, 18:54:43

I selected "How should I know?" since I think the "rear view mirror" should be a duration of about 10 years.

There’s a strange irony related to this subject [oil and gas extraction] that the better you do the job at exploiting this oil and gas, the sooner it is gone.

--Colin Campbell

--Colin Campbell

-

PeakOiler - Intermediate Crude

- Posts: 3664

- Joined: Thu 18 Nov 2004, 04:00:00

- Location: Central Texas

Re: Peak?

![]() by zoidberg » Fri 18 Sep 2015, 20:27:43

by zoidberg » Fri 18 Sep 2015, 20:27:43

2016 might be early. Iran is going to ramp up as is the rest of Opec looking for money. Don't be so impatient lol. Shale and oil are looking to be resilient enough to keep going for a long while yet. Id be reluctant to hazard a guess, but since it scarecly matters im going to say around 2020. All bets are off if war gets into saudi Arabia though and odds of that are increasing.

-

zoidberg - Tar Sands

- Posts: 635

- Joined: Wed 23 Feb 2005, 04:00:00

- Location: Center of north america

Re: Peak?

![]() by Subjectivist » Fri 18 Sep 2015, 21:11:35

by Subjectivist » Fri 18 Sep 2015, 21:11:35

$this->bbcode_second_pass_quote('zoidberg', '2')016 might be early. Iran is going to ramp up as is the rest of Opec looking for money. Don't be so impatient lol. Shale and oil are looking to be resilient enough to keep going for a long while yet. Id be reluctant to hazard a guess, but since it scarecly matters im going to say around 2020. All bets are off if war gets into saudi Arabia though and odds of that are increasing.

Two things to keep in mind before you count on Iran flooding world oil markets. First we know they have been cheating, selling oil despite sanctions that America and the EU said they couldn't sell.

Second they have the highest population of any Persian Gulf country and burn a lot of their oil domestically already. The ELM says they will be burning even more domestically by 2020 than they do today.

Given these two facts it seems like other than a very brief blip from whatever they have put in storage the increase in world supply will not be very large or very long lasting.

II Chronicles 7:14 if my people, who are called by my name, will humble themselves and pray and seek my face and turn from their wicked ways, then I will hear from heaven, and I will forgive their sin and will heal their land.

- Subjectivist

- Volunteer

- Posts: 4705

- Joined: Sat 28 Aug 2010, 07:38:26

- Location: Northwest Ohio