rockdoc, rockman, this is an interesting exchange, but I'm wondering one thing, it's not clear to me. When rockdoc talks about profitability it sounds to me like he's talking about your basic yearly income / costs, the extra being 'profit', but it sounds to me like rockman is talking about the bigger picture, ie, what did the company cost, what income has it generated, and can that income ever match the actual full cost of the company, even with yearly operating 'profits', particularly within the fairly short time period that the company has to get back its costs, including the purchase price of the company.

This is as near as I can come to getting what you are both saying and having it make sense, it sounds to me like rockman, having lived in this world a long time, has learned to ignore yearly income/cost statements that ignore the actual cost of the company.

To put it simply: I decide, wisely, to give up my current career, and to open up a lemonade stand. Because it's a hot location, both in terms of traffic and temp, I pay the kid down the block 150k for the rights to the location, and for the physical stand. Now I'm set, and I get ready to make my fortune, so I sell $1 cups of lemonade which cost me only 28 cents each. This gives me excellent profits in terms of my income/costs, but I will never actually pay for the true cost of the enterprise, so the stuff I dutifully file with the SEC after incorporating and doing everything right, correctly notes that my income is much greater than my costs, and thus makes my stock a very attractive option for those wishing to break into this niche of the lemonade stand market, except that they, too, when they try to buy me out, at $225k, will also never actually make any money in any real sense, though their SEC filings will also consistenly show high profits from their lemonade sales.

I'd have to get into the specifics of what rockdoc is talking about in terms of the actual papers and what they do and do not include when they value a company, but my feeling is that this is roughly what is being said as to why these companies for the most part are in fact frauds that will never recoup their actual price/costs.

That would be perfectly in tune with the true scum that run wall street, their public track record is filled with such games and manipulations and lies, so citing those industries as anything other than mere data points is not something I would trust at all as a source, it's not valid and the so called 'regulation' was routinely mocked and openly scorned by wall street, so rockdoc I'd have to say you slightly discredit your point by actually citing those sources as truly reliable, they simply are not. You are aware that ratings agencies were total frauds, still are, right? And stock / bond prices were directly governed by those fake ratings, not by some seriously great regulations that prevented fraud from happening.

So I think pulling away from general statements that rely on stock manipulations etc and reporting standards that are still not fixed does not do anyone's argument or point any credit at all, in fact, it makes it suspect. Now, if you have worked at a company, and can state, our company cost this much to purchase or build up, it generates this cash flow per well, and our total costs / income have long since paid for our company purchase price, etc, then it's a different story.

It's always interesting to see different viewpoints exchanging views, from their perspective, but then you have to at some point go, how credible is the source of the data? Wall street, SEC, is not credible, otherwise 2008 would never have occurred, and those issues have not been fixed, which you as the person citing those types of sources, should be well aware of, and if you aren't, then you'd have no credibility at all. This is not saying that one can't make money flipping stocks, mind you, that's an unrelated game, funded by free gov money at this point, also totally unreal of course...

PeakOil is You

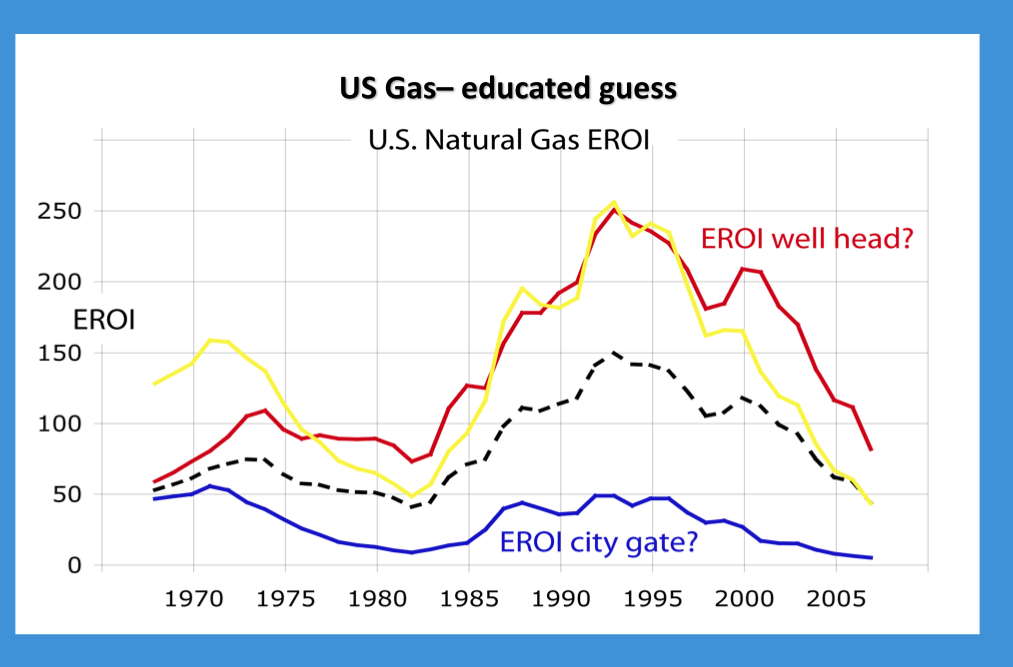

Study: EROEI on Marcellus Shale is 85:1!!!!

Re: Study: EROEI on Marcellus Shale is 85:1!!!!

![]() by h2 » Sat 22 Jun 2013, 19:47:02

by h2 » Sat 22 Jun 2013, 19:47:02

- h2

- Peat

- Posts: 111

- Joined: Fri 31 May 2013, 16:15:15

Re: Study: EROEI on Marcellus Shale is 85:1!!!!

![]() by rockdoc123 » Sun 23 Jun 2013, 11:53:41

by rockdoc123 » Sun 23 Jun 2013, 11:53:41

$this->bbcode_second_pass_quote('', 'r')ockdoc, rockman, this is an interesting exchange, but I'm wondering one thing, it's not clear to me. When rockdoc talks about profitability it sounds to me like he's talking about your basic yearly income / costs, the extra being 'profit', but it sounds to me like rockman is talking about the bigger picture, ie, what did the company cost, what income has it generated, and can that income ever match the actual full cost of the company, even with yearly operating 'profits', particularly within the fairly short time period that the company has to get back its costs, including the purchase price of the company.

When I talk about profits it is in the frame of full cycle economics or point forward economics. When someone is starting out an operation (say acquiring land for shale drilling) full cycle economics are looked at which includes all of the costs including land, drilling, facilities, transportation, people etc. Decisions made during the middle of an operation are usually based on point forward economics given previous costs are sunk. In that case a decision to drill a well is based on payout of the well ignoring previous land and facilites capital expenditures. My comments regarding profitiability in the Eagle Ford are based on full-cycle economics as I have been directly subject to reviewing those particular numbers in the past. As well the break-even cost point I made is in terms of full-cycle economics as that cost includes all costs related to the project historically.

$this->bbcode_second_pass_quote('', 'I')'d have to get into the specifics of what rockdoc is talking about in terms of the actual papers and what they do and do not include when they value a company, but my feeling is that this is roughly what is being said as to why these companies for the most part are in fact frauds that will never recoup their actual price/costs.

This is all included in the annual financial reports. Write downs, impairments, long term debt are all captured. Any money spent in making acquisitions, income from sale of assets, depreciation of assets etc are captured in those statement. If you don’t know how to make heads or tails of financial statements (it’s a bit more difficult with ISFR reporting standards) there are a few decent books out there that explain it in language someone without an accounting background can understand. Using the case that ROCKMAN suggested BHP would have recorded the purchase of the Eagle Ford acreage as capital outlay for asset acquisition. That would have shown up directly against their bottom line. If they were in a position that income from other operations could not offset that capital outlay then they would have recorded a loss and that would be carried forward. If they needed to acquire bank loans or issue additional shares to increase operating capital as a result then that would have shown up as debt in their financials and would create share dilution which is easily measured by EBITDA/share.

$this->bbcode_second_pass_quote('', 'S')o I think pulling away from general statements that rely on stock manipulations etc and reporting standards that are still not fixed does not do anyone's argument or point any credit at all, in fact, it makes it suspect. Now, if you have worked at a company, and can state, our company cost this much to purchase or build up, it generates this cash flow per well, and our total costs / income have long since paid for our company purchase price, etc, then it's a different story.

I think you are confused somewhat. What you are suggesting should be stated is actually submitted every quarter by public oil and gas companies to the SEC. It has even more detail than that. False submissions to the SEC are punishable under law. I’ve pointed out in another thread sometime ago that there are numerous SEC investigations ongoing that are reported to the public but there are countless queries and questions for clarification being asked by the SEC to companies all the time. Just try submitting a 10K that is even slightly out of compliance, you won’t have to wait very long for the official call from the SEC.

$this->bbcode_second_pass_quote('', 't')'s always interesting to see different viewpoints exchanging views, from their perspective, but then you have to at some point go, how credible is the source of the data? Wall street, SEC, is not credible, otherwise 2008 would never have occurred, and those issues have not been fixed, which you as the person citing those types of sources, should be well aware of, and if you aren't, then you'd have no credibility at all. This is not saying that one can't make money flipping stocks, mind you, that's an unrelated game, funded by free gov money at this point, also totally unreal of course...

I’m sorry but it seems you are completely confused here. Are you blaming the SEC for the crash in 2008? The problems that lead to the crash from the banking standpoint were well known, many financial analysts were warning about the potential issues well in advance. The information was all there, people just chose to ignore it. As to controls being in place all the SEC can do is require reporting to certain standards, which they do. Companies that lie in their reports are caught, it isn’t a matter of will they be caught but when.

-

rockdoc123 - Expert

- Posts: 7685

- Joined: Mon 16 May 2005, 03:00:00