Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on February 9, 2015

There Is No Peak Oil–But We Are Approaching Peak Low-Cost Oil

The collapse in oil prices over the last seven months looks to destabilize the world stage by redirecting over $1.8 trillion in spending if current prices hold. While worldwide demand exceeds 92 million barrels per day, the drop in price from over $105 this past summer to under $50 translates into sizable savings for the average American.

Who Gains vs. Who Loses

Spread out across all industries, U.S. consumers could be looking at an extra $300 billion in savings this year, since oil touches just about every aspect of daily life in one form or another.

The working poor, in particular, will be the largest beneficiaries, since energy expenses constitute a greater percentage of household income for them than for any other group. They will likely feel as though they are getting ahead, for a change, rather than continuing to slip further into the abyss.

The impact of “less pain at the pump” is closely correlated to positive confidence figures. When the general public is confident, spending shifts to larger and more discretionary purchases, creating a positive feedback loop. This loss of confidence is a large part of what the Fed has been battling since Depression 2.0 began. In order to begin a real recovery, those with tight wallets must feel that safer conditions merit some loosening. Just how important this development really is becomes evident when recognizing that more than half the working population is making less than $30,000 a year.

Already, sentiment has drastically changed, which can help explain much of the improvement in the President’s recent approval numbers, surging upwards by more than 22 points since the November midterms. Low gas prices make people very happy, and happy people tend to spend money.

There will be huge losers to make up for the public’s big win. Many states heavily reliant on the oil sector—states which for years benefited from the much higher manipulated prices—could now be facing economic and social collapse if the lower prices drag on for any significant period of time. The duration of this downturn is the key to how the geopolitical and economic inversion plays out between consumers and producers. It’s like a hot stove: touch it for a short time and you’ll fare all right, but hold your hand there for a while and you’ll be badly burned.

Large crude oil suppliers, like Saudi Arabia, Russia, Venezuela, Canada, and even the great state of Texas, are now in flux as budgeted revenue streams dry up. Most major Wall Street sources are calling for the excess supply to last for the next 12-18 months. But what if they are wrong, just like they were wrong before the prices began to crash?

Supply and Demand

The world’s current demand is estimated to grow from 91.39 million barrels a day to 92.39 in 2015. This daily overcapacity seemingly will add no more than 800K to 1.5 million barrels to the preexisting record level supplies, for the time being.

Future production numbers are highly suspect now that U.S. and Canadian firms are aggressively reducing new drilling. Since 2005, it has been North America’s horizontal drilling and fracking firms which have been responsible for much of the new supply (thank you, Texas, Canada, and the Dakotas). These roughnecks are quick and nimble operators compared to most national oil companies and private industry giants. Unfortunately, the fracking-enabled oversupply, which is being taken for granted, could easily disappear within six months.

The fact that a small 1 to 2 percent (maximum) oversupply has led to a correction in crude oil prices of more than -50 percent is not normal. Price declines of this magnitude can easily reverse if demand increases by just 2 percent in response. With much of the world’s increased demand coming from third world countries, rather than mature economies, the sensitivity to lower prices is amplified to the upside as poorer people of the world change their day-to-day usage.

Emerging markets’ auto sales could be the canary in the coalmine as to what’s to come. A small percentage change in sales volumes in markets as large as India and China involve millions of potential new drivers with tanks to fill. The real question going forward is this: how long before the next shortage develops, sending prices higher?

Wall Street Pundits are Wrong Again

The tectonic shift in prices has caught the entire world by surprise. Next to no one saw this coming this past summer (watch CNBC YouTube clips if you don’t believe it). No major publicly known player was calling for this type of correction. No one. Many of the so-called “experts” that were paraded out last spring kept forecasting stable or higher prices. No one claimed prices would fall below $45 a barrel, so why would anyone listen to these experts’ predictions now?

Geopolitical Aspects

Many governments around the world owe their very existence to the presence of abundant crude supplies within their borders. Without the constant inflow of oil revenue, their ability to function economically will be severely impaired, as they’re essentially one-trick ponies.

Economists, for decades, have written about the curse of oil wealth and how it creates these dependent societies that have no other means to generate wealth. In fact, over 30 percent of Saudi Arabia’s population is foreign workers who, in many ways, function as serfs. Recently the Kingdom decided to increase the bribes to its citizens by an additional $30 billion to keep the Saudi family in power. There are limits to this official practice, as budget surpluses quickly turn to budget deficits.

Excess is too mild of a word to describe the situation in many Middle Eastern countries; much of their society doesn’t even work in a traditional sense. How will these countries, those which rely on guest workers, pay their bills on half a paycheck? Many could, with time, look like ghost towns, as the Golden Goose of high energy prices stops laying eggs.

Those OPEC members that are burdened by higher production costs than the others are already at a breaking point, with Venezuela teetering on the edge of collapse. If just one of these weaker states falls into chaos, the oversupply could quickly become a severe shortage, to say nothing of the risks of ISIS. The President should be topping off the Strategic Petroleum Reserve by adding another 36 million barrels to the existing spare capacity as a precaution. Half-off sales usually don’t last very long.

In the past, when prices were too low for OPEC’s members to pay their sovereign obligations, Saudi Arabia could always be counted on to reduce supply in order to prop up the market. This burden fell on Saudi Arabia because other members could never be counted on not to cheat.

What the Saudis did was outright manipulation, a crime which would land you in jail in the U.S. Arresting the heads of state who currently supply one-third of the market’s daily demand wouldn’t be easy, so they can get away with it.

Economics of Oil Production

The conventional oil fields of the world (which are dwindling in number as well as production totals) deplete at around a 5 percent rate per year, with a 50 percent recovery rate. The new fracking fields deplete at over 50 percent in the very first year, and recover less than 10 percent. This means that over 90 percent of the tight oil freed by fracking and horizontal drilling is left behind. Supply is always available for the right price, but because of the manipulation of the past, no one really knows what the real price would be—until now.

Saudi Arabia’s refusal to decrease production has opened the formerly closed market to price discovery. Having each country and company producing without the safety net of price support should clear out the marginal players very quickly. It appears that $82 a barrel is the industry’s magic number to render added supply economical, given current demand, but no one can really know for sure until producers are put to the test.

Below are the typical production costs for a barrel of oil, taken from various sources:

● Middle East $27

● Offshore Shelf $41

● Heavy Oil $47

● Onshore Russia $51

● Deepwater $52

● Ultra Deepwater $56

● North American Shale $65

● Oil Sands $70

● Arctic $75

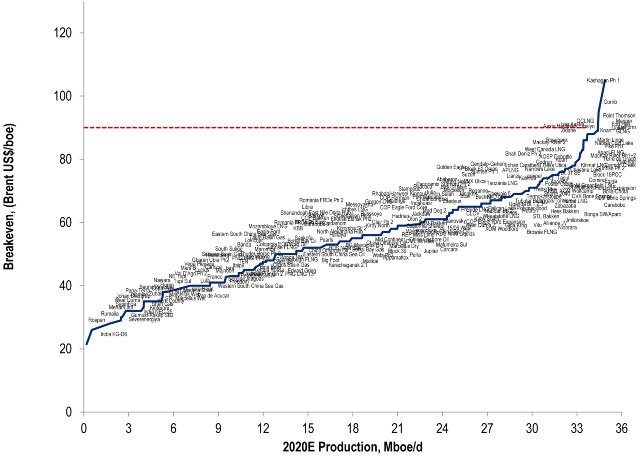

Here is a chart from Citi that is a bit more specific. The key is to understand that those extra barrels cost significantly more as demand increases at the end of the curve.

The new sources of supply that the world is counting on will not last without heavy investment. The flaring rigs lighting up the Dakota nights’ skies burn bright—but have very short lives.

Although technology is forcing the costs of extraction lower, much like Moore’s Law doubles computing power every few years, the days of simply drilling a shallow well and tapping into the next Ghawar for pennies on the dollar are essentially over.

New supply is like the difference between planting an apple tree and planting corn. Conventional apple tree fields have upfront costs and minimal upkeep, but the supply lasts decades. On the other hand, corn and fracking fields require constant high investment in order to maintain supply.

This merry-go-round of constantly having to replenish world demand with fracking rather than conventional sources significantly drives overall costs higher. The Peak Oil believers from a few years ago were not wrong as much as they were off in their assumptions.

There is no Peak Oil, just Peak Low Cost Oil. There will always oil available as new sources are constantly found and technology advances. This reality is best represented by an upward sloping parabolic curve. The variable, once prices reach equilibrium, is what will the next additional barrel cost in the future?

The once bitten, twice shy lenders are well aware of the pricing structure of additional supply, but they are being forced to readjust their models to reflect the higher volatility and added risk.

Much like the Internet crash and housing bubble, what were once viewed as sure things are now seen as a possible financial Ebola, where every cough of borrowers will be seen as a possible death sentence for loans that are souring.

Borrowing costs are going up. A year ago, a bank that would have loaned money to a firm with the market price at $80 a barrel, may today require a $100 price as a condition on the very same project. This added risk premium should lead to much higher future prices, exceeding what saber rattling from Iran ever could. Many firms that were once viewed as prime credit are now seen as junk bond time bombs that could explode at any time. Bankers are nervous.

How much does your home insurance bill go up after a hurricane? This storm of low prices may set in motion a vicious cycle whereby we could be facing a painful rebound as existing supply fails to be replaced. Future financing terms on energy projects will most likely require much higher oil prices, as well as carry much higher interest costs, to compensate for the increased instability. Bankers don’t like to gamble, and taking steps to mitigate as much risk as possible will build in a new higher cost to future production.

Short of some earth-shattering technological energy alternative, the increase in future oil supply will be heavily dependent upon higher and higher investment costs. The world, which will never run out of oil (cheap oil is another story), continues to consume more and more energy each year. The public must remember that in order to keep the supply steady and less volatile, the constant reinvestment merry-go-round must be maintained.

Consumer Behavior is Changing FOR THE WORSE

Consumers should not get comfortable with current pricing. By this December it appears that prices could once again rise above the magic $80 a barrel, as new supply fails to materialize and demand heats up across the globe.

U.S. consumers in December 2014 used over 4 percent more oil daily than they had a year earlier. This increase works out to be an extra 800,000 barrels per day, which, if continued at the same pace through the rest of the year, will make the IEA’s forecast almost a million barrels too low.

Consumers appear to be getting too comfortable with $2.00 a gallon gas. Data shows that $3.00 a gallon is the tipping point for Americans’ choice in vehicle type. With current prices being so low, it should not come as a surprise that SUV sales are increasing and electric vehicle sales are slowing. Unfortunately, these current purchases don’t reflect a scared consumer but instead a naïve one who is assuming low prices will last over the life of their new gas guzzler.

Figures in the next quarter of boat and RV sales, along with airline travel, should be closely monitored. Once these types of purchases start increasing significantly, then you know the public has grown complacent in the face of current tolerable gasoline prices.

What Does This All Mean?

The last seven months have been a financial game of chicken between the old-school crowd in the Middle East, and the roughneck frackers of North America, who are now rewriting the playbook of the last half-century. As commercial hedges fall off, and nimble North American production shuts down, the Invisible Hand of the marketplace will finally be free to disclose the real price of oil that has been hidden by OPEC’s grasp. At the end of the day, it will be the American public that will come out the big winner. We will finally learn, after more than 40 years of not knowing, what the free market supply/demand price of crude truly is. This knowledge will make it harder for secretive governments and corporations to manipulate prices in the future, while strengthening domestic production to weather supply shocks in the future.

28 Comments on "There Is No Peak Oil–But We Are Approaching Peak Low-Cost Oil"

Makati1 on Mon, 9th Feb 2015 7:38 am

The last paragraph is pure Bullshit. The big winners are the ones who do not need much oil in their lives. Those countries that import oil, not export. That do not rely on oil income to run their governments.

It is a boon here in the Ps as gasoline is down under $4/gal. for the first time in 6 years. If it stays low, I expect the taxi and jeepney fares to drop accordingly. But then the average Filipino only uses less than a pint of oil per day as their share of oil energy vs more than two gallons per day for Americans.

Revi on Mon, 9th Feb 2015 7:43 am

The real price of oil is what the market is willing to pay for it. That might not be much, since they are not handing us enough coupons to live the American Dream any more. We are going to see see-sawing gas prices and less and less people working. We’ll never get back to where we were, since even if we used all the oil left we would have less than 210,000 miles per vehicle. We’re on our last cars.

paulo1 on Mon, 9th Feb 2015 8:06 am

Good comments, guys.

The article is a little poofy and couches what Peak Oil is with a redefinition. They say we will never run out of oil…,but, few will be able to pay what it costs to produce. Splitting hairs. In other words, there is a point where the world will never produce as much as we are right now, but that isn’t Peak Oil because we could if the economics worked. Huh?

Remember those school yard fights? “I could have kicked his ass if I really wanted to”? “That Peak Oil deline rate thingy sucker punched me.”

westexas on Mon, 9th Feb 2015 8:29 am

Peak (Crude Oil) in Rear View Mirror?

OPEC dry gas production increased from 41 BCF/day in 2005 to 62 BCF/day in 2012 (EIA, complete 2013 data not yet available), an increase of 21 BCF/day.

Comparing OPEC (crude only) and EIA data bases (C+C) implies that OPEC condensate production increased from 1.2 mbpd in 2005 to 2.3 mbpd in 2012, an increase of 1.1 mbpd.

This was be an observed increase of 52,000 barrels of condensate (BC) per BCF/day increase in gas production, for OPEC.

The EIA shows that global dry gas production increased from 270 BCF/day in 2005 to 325 BCF/day in 2012, an increase of 55 BCF/day.

If we use the OPEC condensate to gas ratio as a guide, this implies that global condensate production rose by about 3 mbpd from 2005 to 2012.

The EIA shows that global C+C rose by 2 mbpd from 2005 to 2012. Note that the high volume of US condensate would fall in the non-OPEC data set, so in reality the non-OPEC BC to BCF/day ratio is probably higher than the OPEC data set.

In any case, the foregoing analysis is additional support for the premise that actual global crude oil production (45 and lower API gravity crude oil) probably peaked in 2005, while global natural gas production and associated liquids, condensate and NGL, have (so far) continued to increase.

shallow sand on Mon, 9th Feb 2015 8:49 am

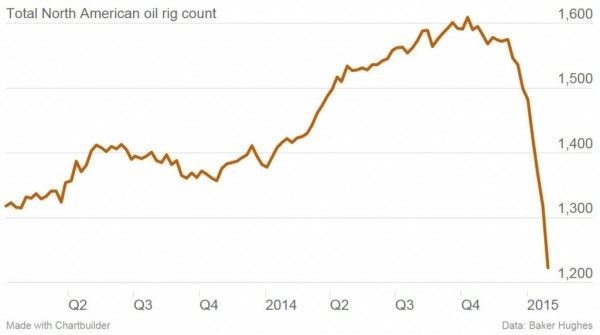

Wish they had posted the oil rig chart from 2000-2014. That would show just how far rigs are going to drop without a much higher price. Oil rigs were never much above 400 in US from 1990-2009.

However, price has went up over $8 recently. It is early, but I think I am getting the answer I was looking for, which is shale needs a much higher price than we do to stay in business. Haven’t lost money yet and haven’t laid anyone off yet.

Just get to about $65 WTI and sit there a couple years, give us a chance to pick up some more “donkey oil” on the cheap.

Mike 991 on Mon, 9th Feb 2015 10:03 am

This is the “Republicans are never wrong” bullshit.

The title is wrong.

“We are approaching peak low cost oil” IS PEAK OIL.

What a dumbass.

What else is it.

We are now in a position to buy 200 mile range EV’s now from Tesla, in two years from GM. We can now power our homes with solar. And we can now store energy in our homes for blackouts.

Oil is DEAD.

It just depends on when you are aware of it.

The longer you deny reality the more MONEY YOU WILL LOSE.

Carbon assets are STRANDED ASSETS Today.

Mike 991 on Mon, 9th Feb 2015 10:05 am

This is why I’m no longer a Republican.

Republicans have become the Dumbass Pussy Party. TERRIFIED of the Future like Little Girlz.

Mike 991 on Mon, 9th Feb 2015 10:06 am

Shock. Republican states built NO RESERVES for an oil downturn. It’s almost as if they can’t govern.

bobinget on Mon, 9th Feb 2015 10:23 am

Pinning down the exact date we began to depart

from “The World of Oil’ then entered “The World of

Gas” is best left to historians.

I’m impressed, as should we all, over discovery news of ‘giant elephant’ fields— not oil but gas and condensates explained eloquently by friend of the board, ‘westexas’.

shortonoil on Mon, 9th Feb 2015 10:23 am

It is interesting that not one analyst has yet come to the very obvious conclusion that it requires oil to produce oil. Perhaps they think it is delivered by the Tooth Fairy? If production declines so does demand. At the present price of crude at least one third of the world’s production is now below full life cycle cost. If producers aren’t making money producing oil, it is likely a lot of them will find a different interest, like golf.

We have done some calculations that excludes the “he said”, “she said”, and “if this one does that, that one will do this”. A whole pile of “ifs” all stacked in a heap are not likely to produce much in the way of accurate forecasting. Long term the price is going down. That will take more production off line as time goes forward, and demand will fall with it:

http://www.thehillsgroup.org/depletion2_022.htm

Our approach is not as wordy as most, but we are not getting paid by the word.

http://www.thehillsgroup.org/

Rodster on Mon, 9th Feb 2015 10:42 am

Short- “If production declines so does demand.”

Can you explain that? Because i’ve always that that the two are separate i.e. production/supply could be down but demand could be thru the roof.

marmico on Mon, 9th Feb 2015 10:55 am

If producers aren’t making money producing oil, it is likely a lot of them will find a different interest, like golf.

It doesn’t quite work that way. No oil production, no money, no green fees for golf.

Thank you that the lard in the U.S. oil business has been transferred to consumer pockets so more of them can play golf.

Production (supply) = consumption (demand) plus/minus inventory build/draw. U.S. inventory build is record big with the contango trade.

rockman on Mon, 9th Feb 2015 11:15 am

“Below are the typical production costs for a barrel of oil, taken from various sources:”

Once again the ignorant use of “production cost” when they actually referring to “development cost”. As fae as those “development cost” numbers they are BS anyway. There is not a single oil price at which any trend is commercial. That determination is made from prospect to prospect: there have been many Eagle Ford Shale wells drilled that proved to be non-commercial at $100/bbl and other EFS wells being drilled today that will make an acceptable profit at $55/bbl. Fewer EFS wells will be drilled at the current price and thus less new EFS production. But some wells will still be drilled and some new production will be created. And the same is true for all trends…conventional and unconventional.

Apneaman on Mon, 9th Feb 2015 11:28 am

Bribart are a bunch of conservative conspiracy tards who think America needs to go back to a golden age… an age that never existed. They are no different than the latte liberals who think we can green industrial civilization and carry on with our undeserved privileged lifestyles forever, if it were not for those dirty oil companies getting in the way. Completely fucking delusional, everyone of them.

Rodster, using whole systems thinking add every bit of fuel burned per well from commuting to and from work and every single thing that is delivered to any and all related sites by rail, heavy trucks, shipping, steel, tools, food, office supplies, medical, etc, etc. It really adds up and thus subtracts when it goes away.

DOT: More than 1,600 trucks could be required for one NC fracking site

Read more here: http://www.newsobserver.com/2015/01/08/4460803/dot-more-than-1600-trucks-could.html#storylink=cpy

rockman on Mon, 9th Feb 2015 11:48 am

Shallow – Actually the stat is worse than you imply. From 2000 until the shale boom began there was an average 900 rigs drilling. But of that 900 an average of only 20% or so were drilling for oil. IOW before the price of oil surged less than 200 rigs were targeting oil prospects. And those 700 rigs drilling NG? For much of that period NG was selling for 2X to 3X the current price. The last time NG prices were at this level only 400 rigs were drilling for it. Not that the math will be that simple but if there were only 200 rigs drilling for oil at its current price and just 400 rigs were drilling for NG at its current price then, in theory, we could be looking at only 600 rigs drilling in the near future if oil/NG prices hover around current levels.

rockman on Mon, 9th Feb 2015 12:00 pm

And today only 314 rigs are drilling for NG. But many of those wells were targeting NG reservoirs with significant associated oil. The drop in oil prices will have a negative impact on all of those prospects.

I don’t think many folks have grasped the full potential negative impact on the service companies the current oil/NG prices may have.

marmico on Mon, 9th Feb 2015 12:04 pm

I don’t think many folks have grasped the full potential negative impact

Take a pay cut.

Perk Earl on Mon, 9th Feb 2015 12:12 pm

If NG, condensates etc. are still rising per WT’s post above, like China’s new NG find, then it would seem the BAU party will go on until such time those other energy sources also go into decline.

That is unless those other energy sources are so different from oil they do not make much of a difference.

OFT on Mon, 9th Feb 2015 12:47 pm

Rockman, marmico – about that negative impact: too true. Talking to those in my service sector network, pay cuts were last month’s news – now the job cuts are starting.

shallow sand on Mon, 9th Feb 2015 2:30 pm

ROCKMAN, so if rig count drops to 300 oil 300 gas (ballpark) US I assume that sets up the super spike that Gulf OPEC has been alluding to recently? Or, if you believe some of the talking heads, shale is so prolific that 600 rigs can keep growing US production of oil and gas.

ROCKMAN, you are correct. Most of the period I referred to (1990-2009) there were about 200 oil rigs running. Got as low as 120s in 1999. Of course, oil production for US was on a slow decline until 2009, and really did not take off until 2011, at which time 1,400 oil rigs had been running continuously for some time. I doubt 300 or even 800 oil rigs continuously running will be able to keep US production flat, especially with the high first year decline. Those 30 day and one year rates coming off will have a big impact, IMO.

shortonoil on Mon, 9th Feb 2015 2:38 pm

Can you explain that? Because i’ve always that that the two are separate i.e. production/supply could be down but demand could be thru the roof.

At the present time it takes about half of the energy content of a unit of oil (barrel, gallon, etc) to extract, process, and distribute the product. It takes half of the energy from oil to produce it, therefore it takes half of the production. Producing petroleum, and its products creates a demand for petroleum!

Here is the 2012 energy breakdown for the “average” barrel:

Extraction…….618,870 BTU/barrel

Processing…….2,053,800

Distribution…..267,330

Total……………..2,940,000 BTU/barrel

The energy content (exergy) of 37.5 deg. crude is 5.88 million BTU/barrel:

http://www.thehillsgroup.org/depletion2_011.htm

That is 50%

As production goes down demand will go down by half.

That percentage is changing with time; for example in 1980 it took 931,500 BTU/barrel to extract, process, and distribute the average barrel. 16% of the energy content of a 35.7 deg. crude. A 1 mb/d drop in production in 1980 reduced demand by 160,000 b/d. In 2012 a 1 mb/d drop would have reduced demand by 500,000 b/d.

This commonly ignored fact makes predictions for the supply/demand balance inaccurate. It will take a production cut of at least 3.0 mb/d to bring the markets’ excess of 1.5 mb/d back in line.

Actually, we are estimating a 4 mb/d reduction will be necessary because of end user demand decline from a slowing global economy. The strong demand that has been seen in the last few years has been largely due to petroleum production itself. This is especially true of shale production which is at best a net zero energy product.

It seems likely that OPEC is aware of this phenomena, and that would explain their reluctance to cut production to raise prices. Production cuts could never be offset by sufficient enough price increases to compensate for their fall in revenue. For OPEC it would be like pushing on a string. For them cutting production would only mean a greater loss of revenue.

http://www.thehillsgroup.org/

rockman on Mon, 9th Feb 2015 3:48 pm

“ROCKMAN, so if rig count drops to 300 oil 300 gas (ballpark) US I assume that sets up the super spike that Gulf OPEC has been alluding to recently?”

maybe: the rig count went into the crapper in the mid 80’s…and oil dropped below $15/bbl.The price f oil depends more upon global economic vitality then any other factor IMHO.

Of course if US production drops off quickly, global demand shoots up as economies benefit from lower oil prices and there’s some sort of ME supply disruption then yes: a super spike could hit us.

Makati1 on Mon, 9th Feb 2015 7:22 pm

Great comments! I had my understanding clarified and reinforced. It is true that many do NOT see the whole systems picture or they would not make the comments that they do.

Oil production does NOT start at the well site or even the state/country where it is located unless that state country produces EVERYTHING that goes into that well site. That is not possible in most locations as very few countries have the mines, refineries, smelting, factories, etc. to make all of the equipment, supplies and skilled personnel necessary from domestic sources.

Total systems (EROEI) are where the breakdown is beginning to occur. Not necessarily the price of oil or where it is located.

Fred's Horseradish on Mon, 9th Feb 2015 9:12 pm

I joined because I was getting the same response from people that many of you get, just today: enough of this end of the

age stuff. But that’s what it is. I have 206 scenic canyon rim acres. 60% of my heat come from these heavy digger/coulter pine cones! I don’t have a TV. I use 4 cyl PUs. In a few years, people are going to say: “you were right.” I am not an expert in oil. More the humanities. Masters.

Fred's Horseradish on Mon, 9th Feb 2015 9:31 pm

I believe in global warming. So far at 3000′, no snow. The glaciers are melting.

Mike 991 on Mon, 9th Feb 2015 10:12 pm

Repubs are the Last to Know.

They have NO IDEA the Breakthrough production in Wind Power, especially with the Polar Vortex Blowing down the east coast. Wind output DOUBLED.

Globally there is a DIVESTMENT from Carbon, especially Coal going on right now.

You’re the last to know because Fox News and the WSJ are NEVER going to tell you about it.

First Solar has increase solar cell output to 21.5%, this is 7 increases in less then 2 years.

Just announced a way to get solar output to 45% efficiency.

Let’s face it, the Republican Whoring up to the Koch Bros is causing your Red States to LOSE Jobs in Wind and Solar, while the Blue States take INVESTOR MONEY and run with these products.

Look at what Repubs have done to Red State Education. Cut College budgets, and Literally transferred that money to the 1%.

You Repubs, the Most Gullible Pussies to ever live, Terrified of the Real World. I feel sorry for any Farmer or Rancher Republican, You’re scheduled to DIE because of Global Warming, and your party will do NOTHING, just like they’re doing Nothing as California goes into it’s FIFTH Year of Drought.

You really do Deserve the Incompetent Government you voted into office in 2014.

No Wind and Solar Jobs for you, the Blue States say THANKS Suckers.

Mike 991 on Mon, 9th Feb 2015 10:14 pm

DON’T Click This Link Republican Sissy Girlz:

http://droughtmonitor.unl.edu

You’ll soil your Pants.

GregT on Mon, 9th Feb 2015 11:57 pm

The world is not divided between Republicans and Democrats Mike. Most countries have more than two ‘choices’, and many people outside of the US can see that the Republicans and Democrats are two sides of the same coin.