Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on April 1, 2014

The Absurdity of US Natural Gas Exports

Quiz:

1. How much natural gas is the United States currently extracting?

(a) Barely enough to meet its own needs

(b) Enough to allow lots of exports

(c) Enough to allow a bit of exports

(d) The United States is a natural gas importer

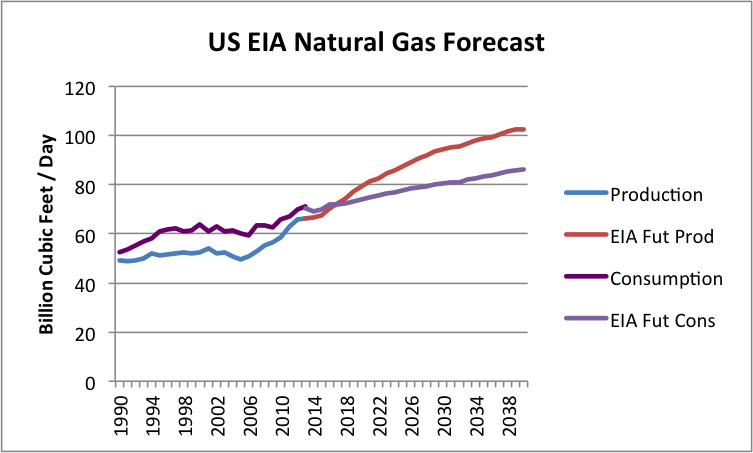

Answer: (d) The United States is a natural gas importer, and has been for many years. The EIA is forecasting that by 2017, we will finally be able to meet our own natural gas needs.

Figure 1. US Natural Gas recent history and forecast, based on EIA’s Annual Energy Outlook 2014 Early Release Overview

In fact, this last year, with a cold winter, we have had a problem with excessively drawing down amounts in storage.

Figure 2. US EIA’s chart showing natural gas in storage, compared to the five year average, from Weekly Natural Gas Storage Report.

There is even discussion that at the low level in storage and current rates of production, it may not be possible to fully replace the natural gas in storage before next fall.

2. How much natural gas is the United States talking about exporting?

(a) A tiny amount, less than 5% of what it is currently producing.

(b) About 20% of what it is currently producing.

(c) About 40% of what it is currently producing.

(d) Over 60% of what it is currently producing.

The correct answer is (d) Over 60% what it is currently producing. If we look at the applications for natural gas exports found on the Energy.Gov website, we find that applications for exports total 42 billion cubic feet a day, most of which has already been approved.* This compares to US 2013 natural gas production of 67 billion cubic feet a day. In fact, if companies applying for exports build the facilities in, say, 3 years, and little additional natural gas production is ramped up, we could be left with less than half of current natural gas production for our own use.

*This is my calculation of the sum, equal to 38.51 billion cubic feet a day for Free Trade Association applications (and combined applications), and 3.25 for Non-Free Trade applications.

3. How much are the United States’ own natural gas needs projected to grow by 2030?

a. No growth

b. 12%

c. 50%

d. 150%

If we believe the US Energy Information Administration, US natural gas needs are expected to grow by only 12% between 2013 and 2030 (answer (a)). By 2040, natural gas consumption is expected to be 23% higher than in 2013. This is a little surprising for several reasons. For one, we are talking about scaling back coal use for making electricity, and we use almost as much coal as natural gas. Natural gas is an alternative to coal for this purpose.

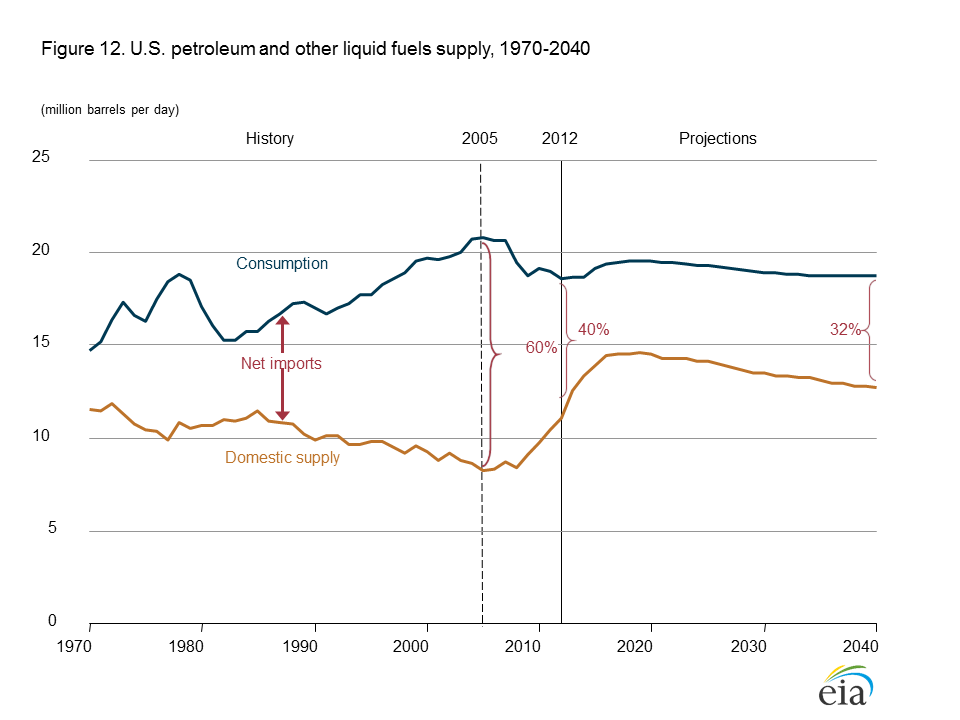

Furthermore, the EIA expects US oil production to start dropping by 2020 (Figure 3, below), so logically we might want to use natural gas as a transportation fuel too.

Figure 3. US Annual Energy Outlook 2014 Early Release Oil Forecast for the United States.

We currently use more oil than natural gas, so this change could in theory lead to a 100% or more increase in natural gas use.

Many nuclear plants we now have in service will need to be replaced in the next 20 years. If we substitute natural gas in this area as well, it would further send US natural gas usage up. So the EIA’s forecast of US natural gas needs definitely seem on the “light” side.

4. How does natural gas’s production growth fit in with the growth of other US fuels according to the EIA?

(a) Natural gas is the only fuel showing much growth

(b) Renewables grow by a lot more than natural gas

(c) All fuels are growing

The answer is (a). Natural gas is the only fuel showing much growth in production between now and 2040.

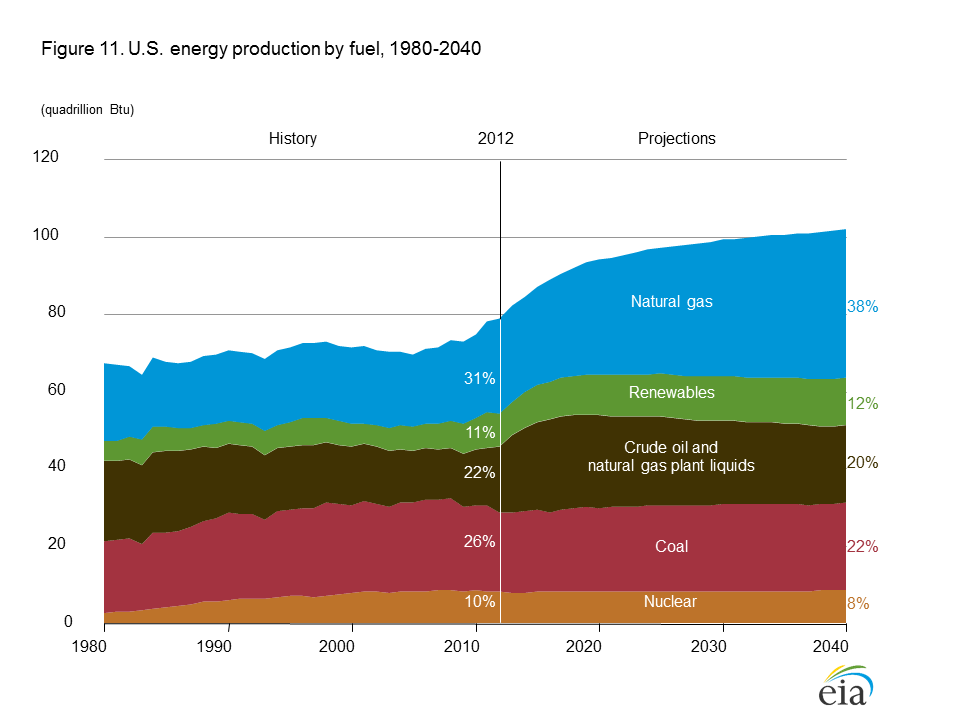

Figure 4 below shows the EIA’s figure from its Annual Energy Outlook 2014 Early Release showing expected production of all types of fuels.

Figure 4. Forecast US Energy Production by source, from US EIA’s Annual Energy Outlook 2014 Early Release.

Natural gas is pretty much the only growth area, growing from 31% of total energy production in 2012 to 38% of total US energy production in 2040. Renewables are expected to grow from 11% to 12% of total US energy production (probably because the majority is hydroelectric, and this doesn’t grow much). All of the others fuels, including oil, are expected to shrink as percentages of total energy production between 2012 and 2040.

5. What is the projected path of natural gas prices:

(a) Growing slowly

(b) Ramping up quickly

(c) It depends on who you ask

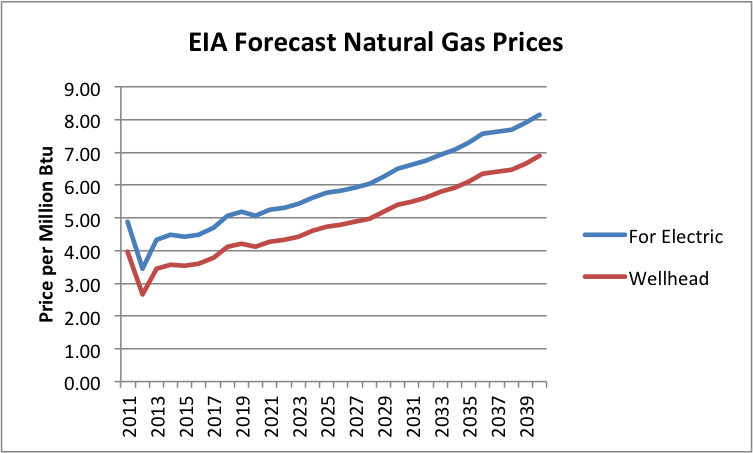

It depends on who you ask: Answer (c). According to the EIA, natural gas prices are expected to remain quite low. The EIA provides a forecast of natural gas prices for electricity producers, from which we can estimate expected wellhead prices (Figure 5).

Figure 5. EIA Forecast of Natural Gas prices for electricity use from AEO 2014 Advance Release, together with my forecast of corresponding wellhead prices. (2011 and 2012 are actual amounts, not forecasts.)

In this forecast, wellhead prices remain below $5.00 until 2028. Electricity companies look at these low price forecasts and assume that they should plan on ramping up electricity production from natural gas.

The catch–and the reason for all of the natural gas exports–is that most shale gas producers cannot produce natural gas at recent price levels. They need much higher price levels in order to make money on natural gas. We see one article after another on this subject: From Oil and Gas Journal; from Bloomberg; from the Financial Times. The Wall Street Journal quoted Exxon’s Rex Tillerson as saying, “We are all losing our shirts today. We’re making no money. It’s all in the red.”

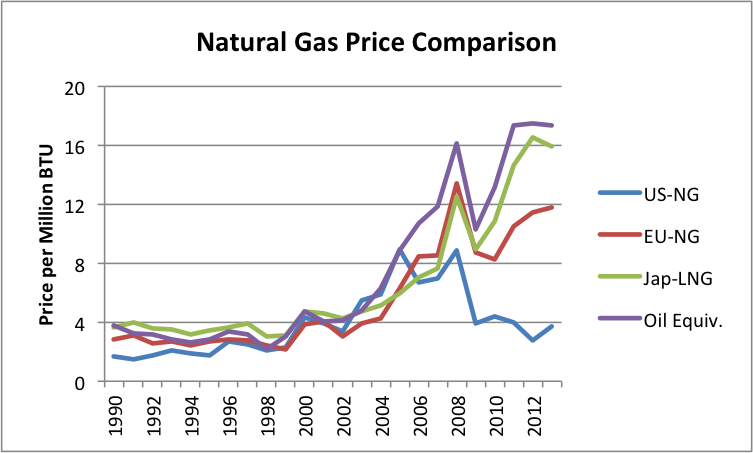

Why all of the natural gas exports, if we don’t have very much natural gas, and the shale gas portion (which is the only portion with much potential for growth) is so unprofitable? The reason for all of the exports is too pump up the prices shale gas producers can get for their gas. This comes partly by engineering higher US prices (by shipping an excessive portion overseas) and partly by trying to take advantage of higher prices in Europe and Japan.

Figure 6. Comparison of natural gas prices based on World Bank “Pink Sheet” data. Also includes Pink Sheet world oil price on similar basis.

There are several catches in all of this. Dumping huge amounts of natural gas on world export markets is likely to sink the selling price of natural gas overseas, just as dumping shale gas on US markets sank US natural gas prices here (and misled some people, by making it look as if shale gas production is cheap). The amount of natural gas export capacity that is in the approval process is huge: 42 billion cubic feet per day. The European Union imports only about 30 billion cubic feet a day from all sources. This amount hasn’t increased since 2005, even though EU natural gas production has dropped. Japan’s imports amounted to 12 billion cubic feet of natural gas a day in 2012; China’s amounted to about 4 billion cubic feet. So in theory, if we try hard enough, there might be a place for the 42 billion cubic feet per day of natural gas to go–but it would take a huge amount of effort.

There are other issues involved, as well. The countries that are importing huge amounts of high-priced natural gas are not doing well financially. They aren’t going to be able to afford to import a whole lot more high-priced natural gas. In fact, a big part of the reason that they are not doing well financially is because they are paying so much for imported natural gas (and oil).

If the US has to pay these high prices for natural gas (even if we produce it ourselves), we won’t be doing very well financially either. In particular, companies who manufacture goods with electricity from high-priced natural gas will find that the goods they make are not competitive with goods made with cheaper fuels (coal, nuclear, or hydroelectric) in the world marketplace. This is a problem, whether the country produces the high-priced natural gas itself or imports it. So the issue is not an imported fuel problem; it is a high-priced fuel problem.

Another issue is that with shale gas, we are the high cost producer. There is a lot of natural gas production around the world, particularly in the Middle East, that is cheaper. If we add our high cost of shale gas to the high cost of shipping LNG long-distance across the Atlantic or Pacific, we will most definitely be the high cost producer. Other producers with lower costs (even local shale gas producers) can undercut our prices. So at best those shipping LNG overseas are likely to make mediocre profits.

And there would seem to be great temptation to stir up trouble, to encourage Europe to buy our natural gas exports, rather than Russia’s. Of course, our ability to provide this natural gas is not entirely clear. It makes a good story, with lots of “ifs” involved: “If we can really extract this natural gas. If the price can really go up and stay up. If you can wait long enough.” The story makes the US look more rich and powerful than it really is. We can even pretend to offer help to the Ukraine.

Perhaps the best outcome would be if virtually none of this natural gas export capacity ever gets built–approval or no approval. If it is really possible to get the natural gas out, we need it here instead. Or leave it in the ground.

24 Comments on "The Absurdity of US Natural Gas Exports"

Davy, Hermann, MO on Tue, 1st Apr 2014 11:32 am

Reality sometimes can be so cruel for the “lobby of plenty and technological exuberance” we have a resident on here his name is NOO. Well done Gail! Noo thinks Gail is a nice lady but a grandmother with no brain. “IF” all this LNG export terminals could be switched to importing LNG I would be all for them because if the US wants to grow economically it will need allot more NatGas besides the huge amount of Red Queen Activity we have now. The financial system is teetering on the knife edge of correction which will leave money more expensive and capex liquidity reduced. “HOW” will our oil/gas industry increase drilling with a declining economy. Anyone here that thinks this financial system will keep humming along like it is for the foreseeable future does not read financial news. Markets are currently repressed with central bank policies that keep interest rates low and liquidity to favored sectors high. These favored sectors are the rich. This policy of wealth transfer and financial distortions and manipulation has unintended consequences. Squeeze a balloon and it budges out somewhere else. In the case of big oil we are seeing capex go down and cost go up. That in my book spells an industry in decline. “WAIT” UNTIL THE REAL SHTF then we will see different talk out of Washington DC.

rockman on Tue, 1st Apr 2014 12:01 pm

A very good report IMHO. Except it tends to ignore some critical factors as many others do on this subject. The simple fact is that the US doesn’t export or import NG. Nor does it export LNG to Asia. Nor will it ever export LNG to the EU. That CHOICE is solely in the hands of the companies that own the NG. And if a significant LNG export infrastructure were to be developed it wouldn’t be the US investing the hundreds of $billions to do so: it would be the LNG export companies. Even fairly well balanced stories like this seem to offer the sense that exporting NG/LNG falls into some political process. Unless the US govt decides to export some of the NG produced on federal leases and pays for the infrastructure there is little to no political aspect. Granted the govt has the right to require a license to build an LNG export terminal that’s the limit of their involvement.

Whether NG is exported from the US or not it doesn’t matter if the US is a net importer of NG or not. The NG belongs to private companies. If they estimate a better profit margin exporting the NG they OWN then it will be exported. But that will require them to expand the infrastructure. Of course, that could change: the US govt currently doesn’t allow oil to be exported. Perhaps one day the govt will make a similar law regarding NG. But trade agreements wouldn’t allow them to cancel existing LNG export contracts which ten to run at least 20 years.

While it’s all well and good for US politicians to toss around statements that they want to help the EU escapes the clutches of Russian NG those politicians have no ability to do so: they don’t own the NG and thus they don’t get to decide if any goes to the EU. The owners of the NG will make that decision. And I’m fairly sure they’ll make that decision based on normal economic considerations: if the EU or anyone else wants US NG all they have to do is make it profitable enough for the OWNERS of that NG to sell to them. Lately the Asian market has been doing so. But at a price significantly higher than the EU is paying for Russian NG.

One last factor in the political rhetoric about the US “helping” the EU out with LNG: there is currently a huge amount of LNG being exported from the ME today. In fact the vast majority of LNG on the planet is coming from the Persian Gulf. The Persian Gulf which is a much shorter sail to the EU then from the US. The Persian Gulf where there is little domestic demand for NG unlike the US where demand exceeds supply. So where should the EU be able to import LNG from cheaper: a market close by which consume far less NG then it produces or a market much further away that consumes more NG then it produces? And even if one takes a leap of faith and assumes the US will have excess NG sometime in the future why would one expect it to sell for a lower price than ME LNG?

And here’s some more recent news that would have an impact on a company’s decision to build LNG export terminals specifically targeting the EU: check out the Yamal LNG project from Russia:

http://www.bloomberg.com/news/2014-01-29/yamal-lng-to-pick-european-transshipment-port-by-third-quarter.html.

It’s about a $30 BILLION project that appears to be aiming trillions of cubic feet of LNG for the EU market. Granted it’s Russian LNG but I’m sure they’ll be competitive with any other LNG supplier. A serious consideration IMHO for any US company deciding to invest many $BILLIONS in LNG export infrastructure.

Arthur on Tue, 1st Apr 2014 12:24 pm

The US pretends to have more fossil muscle than it actually has. It is like slowly driving past the house of the gall you have a crush on in the Ferrari of your friend, with the intention of telling her the truth only after making ‘the score’.

The US likes to see Europe cutting ties with Russia, by pretending that the US can step in. It won’t because it can’t.

The Europeans are not that stupid. Here is the main reason why it is not going to happen, this German self-implementation of the Morgenthau-plan 2.0 of self-de-instrialisation:

http://news.bbcimg.co.uk/media/images/73381000/gif/_73381797_russia_trade_partners_464gr.gif

Rasti on Tue, 1st Apr 2014 12:36 pm

Can somebody tell what is exactly US NG reserves(conventional and unconventional)?

Because with that large export and increase of consumption in USA it’s very hard that US have enough NG for next 30-40 years.

I know that USGS put unconventional reserves on 500 tcf, and conventional are 400 tcf. That is 900 tcf of reserves. And now US produce around 24 tcf/y and is expected to 2025 to grow to 30 tcf/y. So, in that case, US have 30 years of NG on that level of production. Of course, that is not possible, and there will be peak and fall of production.

Maybe i something miss?

Davy, Hermann, MO on Tue, 1st Apr 2014 12:40 pm

Rock, your point in a nut shell covers the primary point. Look to the money. Look to the ownership. The US can make Gas political like you said with regulations barring NatGas exports which is possible in the near future. More likely the markets will dictate no exports. If you look at the physics then there is no denying the reality that infrastructure is not there to export. Financially the price will not be there with Russia and ME far better placed with low price gas and distance. Economically the US will need more gas in the future if it wants to grow and the supply trend is stagnation due to prices, cost, and capex availability.

paulo1 on Tue, 1st Apr 2014 1:05 pm

One disagreement, Rocky. Just like the ownership of gold was once banned:

(Executive Order 6102 is a United States presidential executive order signed on April 5, 1933, by President Franklin D. Roosevelt “forbidding the Hoarding of gold coin, gold bullion, and gold certificates within the continental United States”. The order criminalized the possession of monetary gold by any individual, partnership, association or corporation.)

any Govt. under duress will and can change a law at whim. If electricty rates were to rise to restive levels, or if other industries faced hardships due to world prices, (not just the energy industry owns politicians), or if there was a rapid economic lurch requiring drastic action, the banning of all energy exports is only waiting for a signature by the Govt. in power. Just like there are mothballed steel mills when it suits NA coorporations, it is just as easy to imagine ivy covered walls of a NG export terminal.

I am sure you will argue that if that is the case the companies will simply fold and/or decline to produce NG. I would agree. I am simply pointing out that so far most folks do not believe that the flow of energy will and needs to do so at world prices, rather, that the US is an exception to this rule. Furthermore, it will be a dash of cold water when folks finally realize there is not an over abundance of energy in the US.

regards….Paulo

ghung on Tue, 1st Apr 2014 1:09 pm

Methinks all the hype about exporting natural gas, and the many commercials implying how much the US has, and how wonderful it is, is all about manufacturing consent for eventual higher prices. It’s all for a good cause, so don’t whine if prices go up a bit, eh?

Arthur on Tue, 1st Apr 2014 1:15 pm

Meanwhile, in Holland, Q1-2014 was the worst car sales quarter in 45 years.

http://www.autoblog.nl/nieuws/slechtste-eerste-kwartaal-autoverkopen-in-45-jaar-66190

It looks like peak demand is anticipating peak-fossil by a street length.

Arthur on Tue, 1st Apr 2014 2:14 pm

This just in:

http://deepresource.wordpress.com/2014/04/01/100-electricity-from-wind-for-all-dutch-households-by-2023/

Yesterday, the Dutch government allocated 11 areas for 6.0 GW land based wind energy before 2020. Add that to already decided upon 4.4 GW offshore wind capacity before 2023 and all the Dutch households will have 100% electricity from wind by 2023. That is per capita-wise the same as if the US government would decide upon new 202 GW wind capacity before 2023.

More massive NG/fossil demand destruction in the works. Holland finally catching up with other European nations. Better late than never.

Davy, Hermann, MO on Tue, 1st Apr 2014 3:01 pm

Arthur I would be more impressed if that investment was targeted at the end user with lite solar electric and solar water heating in partnership with a simplified national grid made regional. In addition a nationwide program of learning to do less with less, food security, and AGW adaptation strategies

BESIDES planning on 2023 is like planning on a retirement with full benefits in a city like Detroit.

Arthur on Tue, 1st Apr 2014 3:42 pm

http://tinyurl.com/nevdvyb

Holland has ca. 7 million private households. 200,000 now have a solar installation on their roofs, an annual growth rate of 82%. Total capacity 0.8 GW peak (Germany already has 32 GW).

According to this source…

tinyurl . com/py4ncbg

…about half of the roofs in the Netherlands are suitable for solar electricity generation, in other words total capacity: 3.5 million roofs/0.2 million roofs = 17.5 * 0.8 = 14 GW.

With growth rates like almost 100%:

0.4 –> 0.8 –> 1.6 –> 3.2 –> 6.4 –> 12.8… that’s ca. 6 years until all roof capacity is occupied.

Next big thing: roads.

tinyurl . com/l2ne6py

In Holland there is so much asphalt: 137,000 km, that is 70 m2 per household. Imagine covering that with solar panels and top layer of 1 cm glass. Pilots are already underway:

deepresource . wordpress.com/2013/01/07/solaroad/

Furthermore, Dutch industry is good at building dikes. There is potential for 6 GW capacity by building a dike perpendicular to the Dutch coast, 40 km straight into the sea. Largest Dutch dike into the sea so far: 32 km (wiki Afsluitdijk, built in 1927-1933). Make holes in the dike and put turbines in it, like this:

deepresource . wordpress.com/2013/10/07/6-gw-tidal-power-dam-proposed-off-the-dutch-coast/

Nice export product. The Chinese already have shown interest.

No need for fracking whatsoever. The potential for 100% transition in the second most densely populated country in the world is there.

rockman on Tue, 1st Apr 2014 4:16 pm

Rasta – I don’t think you’re missing much. But you do seem to be equating anyone’s “proven” reserve numbers with future production rates. The future rate of US NG production, how much we consume and how much we might have an excess of to become a net exporter has little bearing on how much NG we have “proven” in the ground. Look at the volatility of NG prices, drilling activity and consumption over the last dozen years and it provides little optimism for anyone’s prediction for the next 30 years IMHO. First, that proven number is based upon an assumed NG price: the NG “proven” reserve assuming $4/mcf is much less than a $9/mcf assumption. Second, regardless what we are producing on any given day in the future the export capability will depend upon or NG consumption. Is that going to increase 2%/yr or 4%/yr for the next 30 years?

Dividing the amount of “proven” reserves by any assumed production rate is rather meaningless IMHO. It assumes that the second half of whatever number you chose to use will come out of the ground at the same rate. In general that’s a rather poor assumption. Typically the higher rate wells in a play are drilled first. Which brings up another problem: those “proven” reserves in the ground can’t be produced at a rate higher than can be achieved for the number of wells drilled. And that number depends upon the complex economic dynamics of resource development.

Davy, Hermann, MO on Tue, 1st Apr 2014 4:26 pm

Arthur how is the dutch mentality for doing less with less? I am sure better than the “land of the free and home of the brave” idea of the American Dream and living life to it’s fullest i.e. excess financed by debt! I am impressed with your countries end user AltE statistics and if all this is true this should be a template for the rest of the world.

GregT on Tue, 1st Apr 2014 4:56 pm

Arthur,

“The potential for 100% transition in the second most densely populated country in the world is there.”

So the potential for 100% energy production during the transition is there. That IS a good thing. Any plans for post transition? AFTER modern industrial society is no longer able to mass produce all of the electric gadgets that all the infrastructure is being put in place to power? Does it really make sense to spend so much time, energy, and resources on something that might last for a few decades at best? Wouldn’t it make more sense to focus on food production, instead of focussing on generating electricity for items that will soon no longer be available? Wouldn’t an all out effort to mitigate the coming effects of CC make much more sense in a country that is largely below sea level?

Maybe it’s just me, but all I am seeing is a futile attempt at continuing on with BAU. Something that is only possible for a relatively short period of time, if climate change is NOT being taken into consideration.

Arthur on Tue, 1st Apr 2014 5:07 pm

Greg, I am not saying that all altE potential should be realized, just that it is there. Besides, it would take decades to implement. What I am saying is that despair for the future is unnecessary, at least for the west.

GregT on Tue, 1st Apr 2014 6:09 pm

Arthur,

Here on the west coast of Canada, there is zero thought being given to altE infrastructure, our population and traffic are growing exponentially, our agricultural lands are being paved over and turned into condos and big box shopping centres, and debt levels are rising faster than in all of history. The only thoughts on ‘transition’, are bike lanes in the downtown core, urban densification, rooftop gardens, and chicken coops. Most people have absolutely no clue about climate change, ocean acidification, peak oil, or even where their food comes from. The drive, shop, consume lifestyle, is accelerating at a pace that is beyond comprehension, (to me) and people are more concerned with money, than they are about life on the planet that they live on.

No reason to despair about the future, everything will be just fine. Somebody, somewhere, has everything under control, and all of our best interests, are of their primary concern.

Davy, Hermann, MO on Tue, 1st Apr 2014 6:27 pm

Arthur said – What I am saying is that despair for the future is unnecessary, at least for the west.

I echo what Greg said. We are a society that is compulsive in our pursuit of anything technical. We have little interest in simplifying and doing less with less. Even an attitude of relative sacrifice is hard to find anywhere in the world in numbers to make a significant difference. Much of the world is so poor they experience forced sacrifice. I mention this attitude of increase complexity and technology even for a place like Europe. Europe treats the old ways like hobbies but they still look to complexity over simplification in their societal structures. I readily admit the US is the worst example of hyper consumerism from a hijacking by the BIG corporations. Change is in the air but it is too little too late IMHO.

Arthur, you amaze me. You can have these very entertaining political diatribe that are sensational and fantastic. They are way above my head because I just don’t invest the time it takes to research these things. I have a very good background in history, geography, and culture but not in the intrigue and conspiracies of history and the resulting global political reality. LSS, then Arthur you say “despair for the future in unnecessary”. I guess being a doomer I can’t see the optimism you do but every day (day in day out) I see bad news reinforcing bad news in a relentless stream. Tell me Folks “HOW” the hell can you have a positive face on status quo BAU? And if you believe BAU over tell me the silver bullet waiting in the wings to save us from ourselves. This is not the fall of the Berlin Wall where the west welcomed the vanquished USSR into a functioning western system. We have a problem Houston. We are an overcrowded spaceship traveling to an unknown destination with power, food, water, heating/cooling, and waste problems. You tell me how to be optimistic?

GregT on Tue, 1st Apr 2014 6:39 pm

April fools day? Front page of todays local rag.

http://epaper.theprovince.com/epaper/viewer.aspx

Everyone is doing the usual finger pointing, almost nobody understands why prices are rising exponentially, and will continue to do so. Meanwhile, wages have been stagnant for over a decade, more and more of our population are now called the working poor, and our Premier, Christy Clarke, is going to solve everyones problems by fracking for natural gas, and shipping it off to Asia.

Ya, everything is coming up roses. Glad I have a plan B. The sooner it’s completed, the better.

J-Gav on Tue, 1st Apr 2014 7:31 pm

Good article.

Arthur on Tue, 1st Apr 2014 7:43 pm

Davy, Greg… I guess it is more a matter of temperament. Maybe we ARE going to have runaway climate change, nuclear war, over population, race wars, clashes of civilization, resulting in game over for human civilization.

And then again, maybe not.

No, I don’t believe in BAU, don’t even desire BAU. Am actually looking forward to a world with less materialism, less miles traveled, less stuff bought. But despair is simply not an option. OK, we are running out of fossil fuel. What can we do about it? Renewables. OK, let’s do it, implement it.

DC on Tue, 1st Apr 2014 7:45 pm

IF you look at all the price increases, it is worth noting that almost every single one(with the exception of tobacco) is attached to unsustainable, wasteful end-user practices.The hidden subsidies BC users have enjoyed for long are starting to give way to, well, reality.

Hydro-I am sure well both agree, BC users are no paragons of efficiency or fugality when it comes to electricity use. Plus exporting huge amounts of power to equally wasteful amerikans to the south isn’t helping any either.

Gas-We frak now. Its out of sight, out of mind-but most of the ‘real’ gas is gone.I keep hearing the massive ‘glut’ of frak gas on both sides of the border was supposed to signal the beginning of NG nirvana. Maybe not eh?

BC Ferries-An inefficient, wasteful organization that never misses a chance to pass on its bloated overhead to those least likely to afford it. That gold-plated parachute\pension plan for the amerikan ex-CEO Hahn(315K per annum), while he kicks back in whatever gated community in the uS he came from isn’t going to pay itself. With ridership down(due ironically to high ferry rates in part), got to squeeze walk ons and seniors for every last drop.

Canada Post-Pushed into the uneviable position of having to ‘compete’ with amerikan firms, FedEx and UPS with its 11/12.00 hr. drivers and min wage sorters(that work 3 4 hours a day), finally forced to bump stamp costs to help cover costs. Sure email hasnt helped, but opening up CP to ‘competition’ from min. wage uS corps only effect seems to be the gradual elimination of CP as a public service. Isnt ‘privatization’ and corporate rule working out grand?

As the subsidies for our most wasteful and inefficient systems get slowly withdrawn-this is what we can expect to see. All the solar panels and tesla cars in the world wont change the underlying reality.

antaris on Tue, 1st Apr 2014 8:21 pm

Paulo

What are your thoughts on this huge amount of NG we are supposed to have in BC ? I like Christy but giving away my great grand kids hot bath does not make sense.

GregT on Wed, 2nd Apr 2014 2:56 am

Antaris,

Sorry to be a downer, but if we exploit the current fossil fuel reserves, never mind the stuff we haven’t tapped into yet, your great grand kids won’t be bathing in anything. Unless they have been born already, or your grand children are close to being grown up, in all likelihood your great grandchildren will never be born. If they are some of the very few that make it through the middle of this century, they’ll probably wish they hadn’t.

GregT on Wed, 2nd Apr 2014 3:00 am

Oh, and while we’re talking about Christy, I went to school with her brother, and my sisters both went to school with Christy. Let’s just say, tigers never change their stripes.