Beginning of the End? Oil Companies Cut Back on Spending

Steve Kopits recently gave a presentation [link to presentation at resilience.org] explaining our current predicament: the cost of oil extraction has been rising rapidly (10.9% per year) but oil prices have been flat. Major oil companies are finding their profits squeezed, and have recently announced plans to sell off part of their assets in order to have funds to pay their dividends. Such an approach is likely to lead to an eventual drop in oil production. I have talked about similar points previously (here and here), but Kopits adds some additional perspectives which he has given me permission to share with my readers.

I encourage readers to watch the original hour-long presentation at Columbia University, if they have the time.

Controversy: Does Oil Extraction Depend on “Supply Growth” or “Demand Growth”?

The first section of the presentation is devoted the connection of GDP Growth to Oil Supply Growth vs Oil Demand Growth. I omit a considerable part of this discussion in this write-up.

Economists and oil companies, when making their projections, nearly always make their projections depend on “Demand Growth”–the amount people and businesses want. This demand growth is seen to be rising indefinitely in the future. It has nothing to do with affordability or with whether the potential consumers actually have jobs to purchase the oil products.

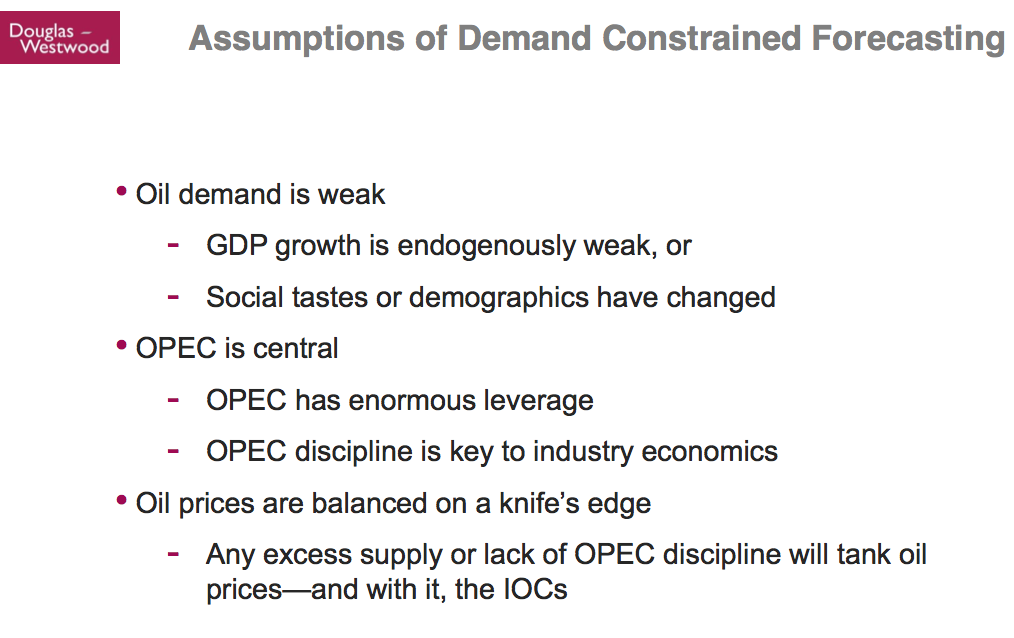

Kopits presents the following list of assumptions of demand constrained forecasting. (IOC’s are “Independent Oil Companies” like Shell and Exxon Mobil, as contrasted with government owned companies that are prevalent among oil exporters.)

Thus, it is the demand constrained view of forecasting that gives rise to the view that OPEC (Organization of Petroleum Exporting Nations) has enormous leverage. The assumption is made that OPEC can add or subtract as much supply as much as it chooses. Kopits provides evidence that in fact the Demand view is no longer applicable today, so this whole story is wrong.

One piece of evidence that the Demand Model is wrong is the fact that world crude oil (including lease condensate) production has been nearly flat since 2004, in a period when China and other growing Eastern economies have been trying to motorize. In comparison, there was a rise of 2.7% per year, when the West, with a similar population, was trying to motorize.

Kopits points out that China’s big source of oil supply has been US main street: China bids oil supply away from United States, to satisfy its needs. This is the way that markets have made oil available to China, when world supply is not rising much. It is part of the reason that oil prices have risen.

Another piece of evidence that the Demand Model is wrong relates to the assumption thatsocial tastes have simply changed, leading to a drop in US oil consumption. Kopits shows the following chart, indicating that the major reason that young people don’t have cars is because they don’t have full-time jobs.

Kopits makes a comparison of the role of oil in GDP growth to the role of water in plant growth in the desert. Without oil, there is less GDP growth, just as without water, a desert is starved for the element it needs for plant growth. Lack of oil can considered a binding constraint on GDP growth. (Labor availability might be a constraint, but it wouldn’t be a binding constraint, because there are plenty of unemployed people who might work if demand ramped up.) When more oil is available at a slightly lower price, it is quickly absorbed by markets.

“Supply Growth” is the limiting factor in recent years, because the amount of extraction is rising only slowly due to geological constraints and the number of users has risen to the point that there is a shortage.

Experience of Major Oil Producing Companies

Kopits presents data showing how badly the big, publicly traded oil companies are doing. He looks at two pieces of information:

- “Capex” – “Capital expenditures” – How much companies are spending on things like exploration, drilling, and making of new offshore oil platforms

- “Crude oil production” –

A person would normally expect that crude oil production would rise as Capex rises, but Kopits shows that in fact since 2006, Capex has continued to rise, but crude oil production has fallen.

The above information is worldwide, not just for the US. At some point a person might expect companies to start getting frustrated–they are spending more and more, but not getting very far in extracting oil.

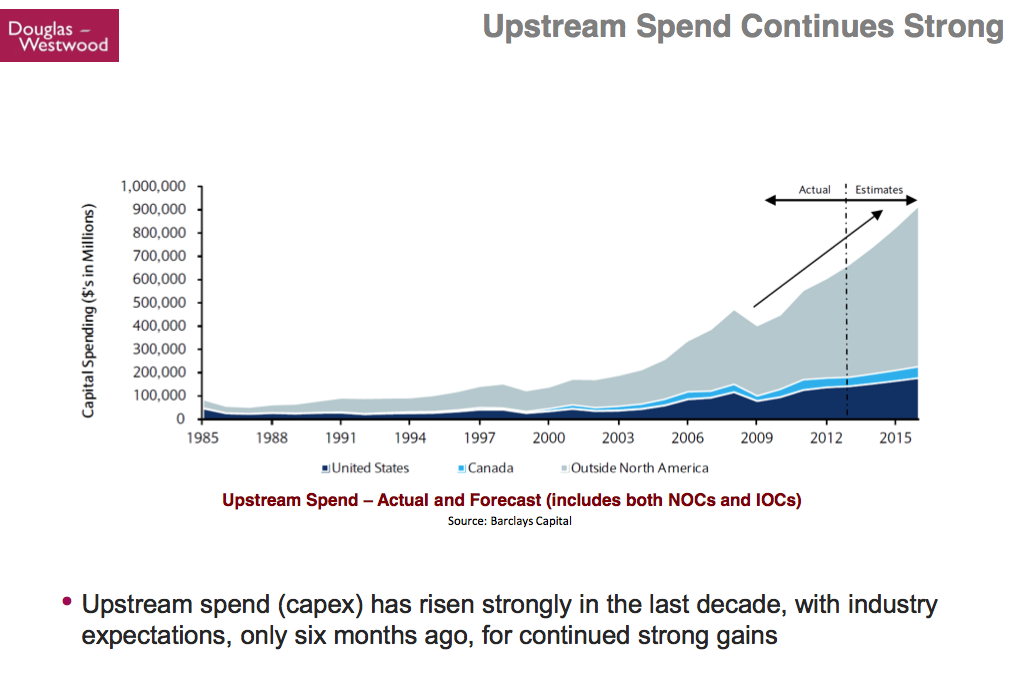

Kopits then shows another version of Capex history plus a forecast. (This time the amounts are labeled “Upstream,” so the expenditures are clearly on the exploration and drilling side, rather than related to refineries or pipelines.)

The amounts this time are for the industry as a whole, including “NOCs” which are government owned (national) oil companies as well as IOCs (Independent Oil Companies), both large and small. Kopits remarks that the forecasts shown were made only six months ago. When talking about the above slide Koptis says,

People in the industry thought, “Capex has been going up and up. It will continue to do very well. We have been on this trajectory forever, and we are just going to get more and more money out of this.”

Now why is that? The reason is that in a Demand constrained model for those of you who took economics–price equals marginal cost. Right? So if my costs are going up, the price will also go up. Right? That is a Demand constrained model. So if it costs me more to get oil, it is no big deal, the market will recognize that at some point, in a Demand constrained model.

Not in a Supply constrained model! In a Supply constrained model, the price goes up to a price that is very similar to the monopoly price, after which you really can’t raise it, because that marginal consumer would rather do with less than pay more. They will not recognize [pay] your marginal cost. In that model, you get to a price, and after that price, there is significant resistance from the consumer to moving up off of that price. That is the “Supply Constrained Price.” If your costs continue to come up underneath you, the consumer won’t recognize it.

The rapidly growing Capex forecast is implicitly a Demand constrained forecast. It says, sure Capex can go up to a trillion dollars a year. We can spend a trillion dollars a year looking for oil and gas. The global economy will accept that.

I quote this because I am not sure I have explained the situation exactly that way. I perhaps have said that demand had to be connected to what consumers could afford. Wages don’t magically go up by themselves (even though economists think they can).

According to Koptis, the cost of oil extraction has in recent years been rising at 10.9% per year since 1999. (CAGR means “compound annual growth rate”).

Oil prices have been flat at the same time. On the above chart, “E&P Capex per barrel” is pretty much the same type of expenses as shown on the previous two charts. E&P means Exploration and Production.

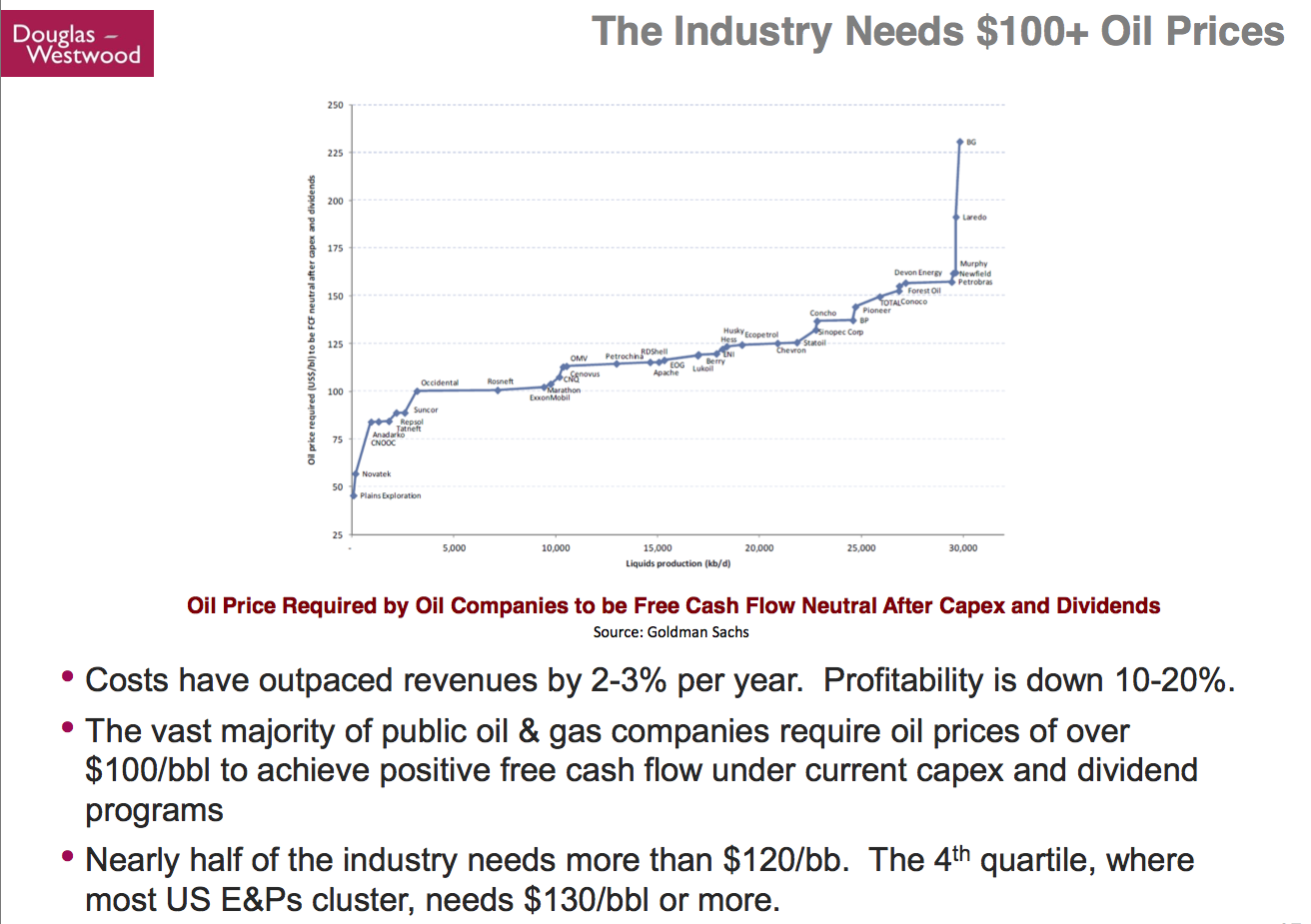

Kopits explains that the industry needs prices of over $100 barrel.

The version of the chart I have up is too small to read the names of individual companies. If you would like a chart with bigger names, you can download the

original presentation.

Historically, oil companies have used a discounted cash flow approach to figure out whether over the long term, pricing for a particular field will be profitable. Unfortunately, this “standard” approach has not been working well recently. Expenses have been escalating too rapidly, and there have been too many new drilling sites producing below expectation. What Kopits shows on the above slide is the prices that companies need on different basis–a “cash flow” basis–so that each year companies have enough money to pay today’s capital expenditures, plus today’s expenses, plus today’s dividends.

The reason for using the cash flow approach is because companies have found themselves coming up short: they find that after they have paid capital expenditures and other expenditures such as taxes, they don’t have enough money left to pay dividends, unless they borrow money or sell off assets. Oil companies need to pay dividends because pension plans and other buyers of oil company stocks expect to receive regular dividends in payment for their equity investment. The dividends are important to pension plans.

In the last bullet point on the slide, Kopits is telling us that on this basis, most US oil companies need a price of $130 barrel or more. I noticed that Brazil’s Petrobas needs a price of over $150 barrel. (OSX, Brazil’s number two oil company,

recently went bankrupt.)

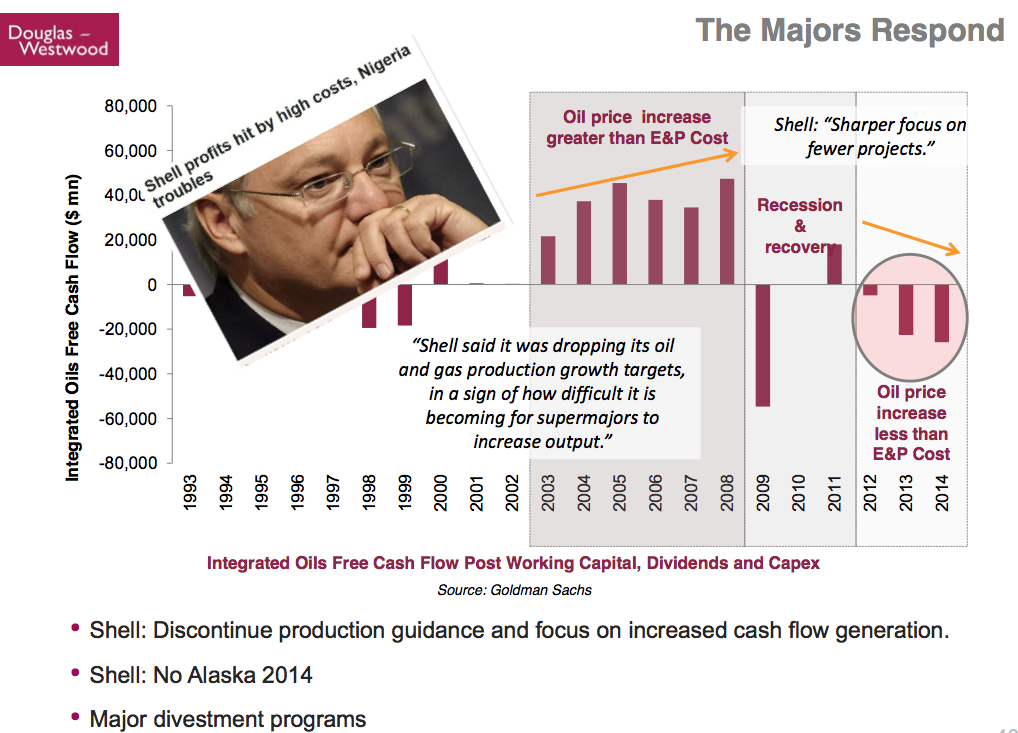

In the slide below, Kopits shows how Shell oil is responding to the poor cash flow situation of the major oil companies, based on recent announcements.

Basically, Shell is cutting back. It no longer is going to tell investors how much it plans to produce in the future. Instead, it will focus on generating cash flow, at least partly by selling off existing programs.

In fact, Kopits reports that all of the major oil companies are reporting divestment programs. Does selling assets really solve the oil companies’ problems? What the oil companies would really like to do is raise their prices, but they can’t do that, because they don’t set prices, the market does–and the prices aren’t high enough. And the oil companies really can’t cut costs. So instead, they sell assets to pay dividends, or perhaps just to get out of the business. But is this sustainable?

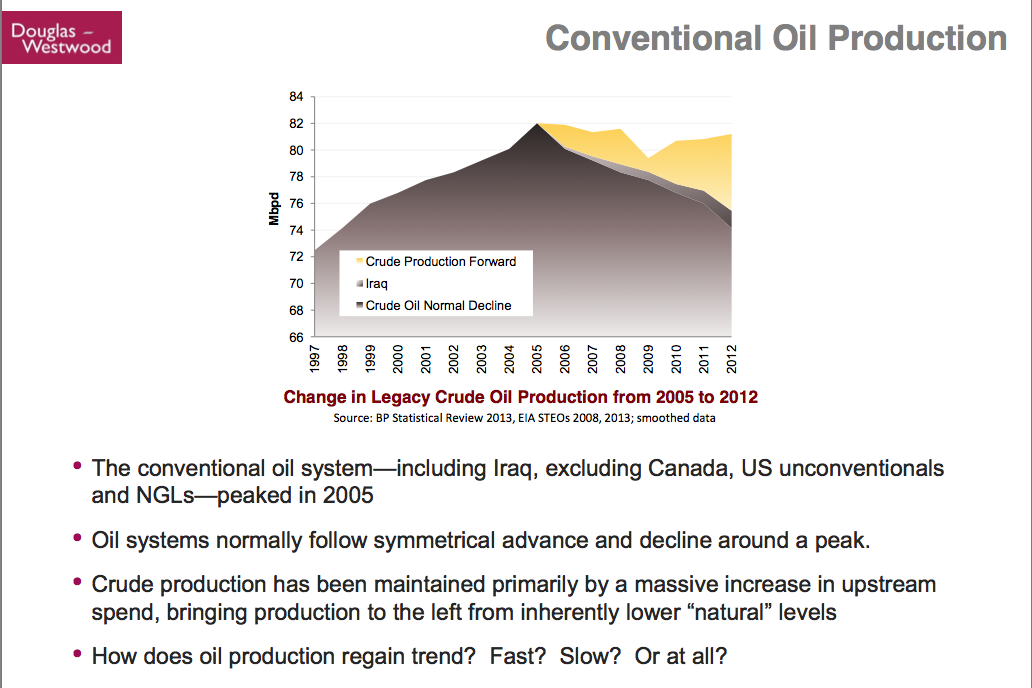

The above slide shows that conventional oil production peaked in 2005. The top line is total conventional oil production (calculated as world oil production, less natural gas liquids, and less US shale and other unconventional, and less Canadian oil sands). To get his estimate of “Crude Oil Normal Decline,” Kopits uses the mirror image of the rise in conventional oil production prior to 2005. He also shows a separate item for the rise in oil production from Iraq since 2005. The yellow portion called “crude production forward” is then the top line, less the other two items. It has taken $2.5 trillion to add this new yellow block. Now this strategy has run its course (based on the bad results companies are reporting from recent drilling), so what will oil companies do now?

Above, Kopits shows evidence that many companies in recent months have been cutting back budgets. These are big reductions–billions and billions of dollars.

On the above chart, Kopits tries to estimate the shape of the downslope in capital expenditures. This chart isn’t for all companies. It excludes the smaller companies, and it excludes the National oil companies, so it is about one-third of the market. The gray horizontal line at the top is the industry consensus back in October. The other lines represent more recent estimates of how Capex is declining. The steepest decline is the forecast based on Hess’s announcement. The next steepest (the dotted gray line) is the forecast based on Shell’s cutback. The cutback for the part of the market not shown in the chart is likely to be different.

Oil and Economic Growth

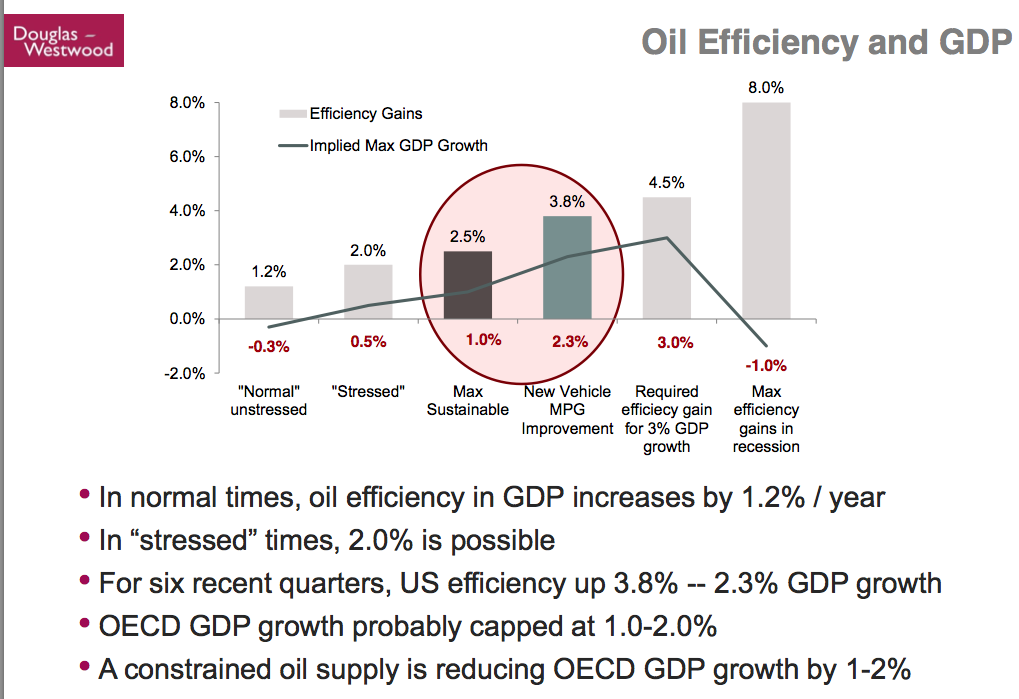

Kopits offers his view of how much efficiency can be gained in a given year, in the slide below:

In his view, the maximum sustainable increase in efficiency is 2.5% in non-recessions, but a more normal increase is 1% per year. At current oil supply growth levels, OECD GDP growth is capped at 1% to 2%. The effect of constrained oil supply is reducing OECD GDP growth by 1% to 2%.

Conclusions

While demand constrained models dominate thinking, in fact, a supply constrained model is more appropriate in recent years.

We seem to be short of oil. Whenever there is extra oil on the market, it is quickly soaked up. Oil prices have not collapsed. No one is nervous about a price collapse.

China recently has been putting little price pressure on the market–its demand is recently less high. Kopits thinks China will eventually return to the market, and put price pressure on oil prices. Thus, oil price pressures are likely to return at some point.

Gail’s Observations

An obvious point, which I thought I heard when I listened to the presentation the first time, but didn’t hear the second time is, “Who will buy all of these assets on the market, and at what price?” China would seem to be a likely buyer, if one is to be found. But when several companies want to sell assets at the same time, a person wonders what prices will be available.

The new strategy is, in effect, maintaining dividends by returning part of capital. It is clearly not a very sustainable strategy.

It will take a while for these cut-backs in Capex expenditures to find their way through to oil output, but it could very well start in a year or two. This is disturbing.

What we are seeing now is a cutback in what companies consider “economically extractable oil”–something that isn’t exactly reported by companies. I expect that what is being sold off is mostly not “proven reserves.”

In this talk, it looks like lack of sufficient investment is poised to bring the system down. That is basically the expected limit under Limits to Growth.

In theory, if an expansion of China’s oil demand does bring oil prices up again, it could in theory encourage an increase in drilling activity. But it is doubtful that economies could withstand the high prices–they are already having problems at current price levels, considering the continued need for Quantitative Easing to keep interest rates low.

Mr Hockey said reaching the goal would require increasing investment but that it could create “tens of millions of new jobs”.

The cutback in investment by oil companies is working precisely in the wrong direction. If these cutbacks act to cut future oil extraction, it will bring down growth further.

Our Finite World

rockman on Tue, 4th Mar 2014 4:41 pm

A nice collection of data for sure. But:”Controversy: Does Oil Extraction Depend on “Supply Growth” or “Demand Growth”?”. There is no real controversy. Oil/NG depends on the same two factors today it has always has IMHO: the price of oil/NG and the number of viable prospects available at that price. The price, as always, is determined by the supply/demand relationship. Feel free to banter that relationship around all you like. How many wells can be drilled? For the most part they’ve been known for many years but weren’t economic at lower prices. When ever prices jump the oil patch jumps on that inventory like a duck on a June bug. But in time that viable inventory gets drilled up and activity eventually falls off. That cycle has been repeated without fail in every trend since the beginning of the petroleum age. Thus a decrease of drilling activity even at a fairly constant oil price is predictable.

Neither high oil/NG nor surging demand “create” oil/NG reservoirs…they’ve been there all this time. All that develops are conditions that make them economically viable. There are no more oil and gas fields to discover today then there were 100 years ago. And when the only ones remaining aren’t economical to drill then production increases grind to a halt. If the economies can handle higher prices then more reservoirs will be developed. If not they won’t.

It really is that simple IMHO…always has been.

Northwest Resident on Tue, 4th Mar 2014 5:05 pm

rockman — That makes perfect sense to me, and I guess it also does to anybody else with a brain that doesn’t have a deep psychological need to block out reality.

If I understand correctly, the oil companies pretty much know where all the oil is on planet earth — most of those finds have been mapped over the last hundred years or so. Sure, there are some deep water finds as yet undiscovered, maybe a little shale oil too, but those not-founds represent only a tiny percent of the big picture.

The only question is, at what price does it become economically viable to go after those oil reserves? Theoretically, the price could keep rising forever, perhaps with the price of a barrel of oil going to a few hundred dollars and only the truly wealthy and the government being able to afford that high price.

But that theory falls flat on its face because there is a point where the price of a barrel of oil is simply too high for economy to be able to turn a profit or break even on that high-priced barrel of oil. At that point, the price can’t go up any more and it won’t because demand drops through the floor.

When it comes to how high can the price of oil go in reality, I think there must be a “sweet spot” where the price is high enough to incent sufficient oil production to keep things rolling along more or less normally, and not so high that the government and financial giants can’t cover up the severe damage being done to the economy by that high price through stock market manipulations and other tricks. I think that’s where we are right now.

Eventually, the oil that can be produced with the price hovering in that “sweet spot” zone will be gone or severely depleted. Then what happens?

rockman on Tue, 4th Mar 2014 5:29 pm

NR – Not so much that they know exactly where the reserves are but they have a good idea where to poke around for them. As I mentioned before we knew about the oil production capability of the Eagle Ford Shale over 30 years ago. And we had the drilling/frac’ng tech to develop it 20 years ago. It was just a matter of waiting for prices that justified it. Then it boils down to risk vs. reward. At $100/bbl lots of new oil wells will be drilled but so will a lot of dry holes. But eventually as the less risky prospects are developed only the riskier/smaller ones remain.

And that takes us back to your observation: there’s a limit to how high a price the economies can handle. If the bulk of remaining reserves require such a higher price then they won’t be developed. So it is true: we will never run out of oil/NG. We’ll just run out of oil/NG the economies can afford to buy.

Nony on Tue, 4th Mar 2014 6:54 pm

US gas looks pretty plentiful though. A switch from LNG import to export projects (several billions investment) is massive. Somewhat more of a real changed game than the oil world. I mean Marcellus gas has been climbing steadily, even with pricing at $4-5. And the long term futures are stubbornly at 4.75 or so. The markets guess on supply/demand seems to be pretty strongly predicting abundant supply.

And no…I’m NOT saying NG can replace oil. Just that everything is not predictable.

Go gas and watch over us from Heaven, Saint George Mitchel! 😉

Nony on Tue, 4th Mar 2014 6:56 pm

P.s. Haven’t we seen this same presentation about 1-2 times already on this site? I think Kopits is very interesting and would love to pick his brain, engage with him, challenge him (just a widdle). Gail OTOT. Woah! Nice lady, but…come on. Kopits, James Hamilton, those are the sorts of peakers that I want to learn from.

Nony on Tue, 4th Mar 2014 6:57 pm

OTOH. Typo fail. 🙁

Davy, Hermann, MO on Tue, 4th Mar 2014 6:58 pm

Nony, I am not sure the economics are going to be there if we have a financial correction that is due anyday. These gas sources are already marginally profitable to unprofitable lately.

Nony on Tue, 4th Mar 2014 7:07 pm

Davy, could be. We definitely don’t seem to be seeing any more sub-4 gas. That was a glut that was worked off. Even if it goes to 6 or 7 though, there will be huge ability to supply the market.

And for some reason, the financial markets don’t even thing we get over 5 long term. I think the shale revolution really has made a big difference for gas.

I am not an oil professional (IANAOP), but my naïve thought is perhaps the chemistry of NG is enough different (much smaller molecule, getting through tinier cracks?) Also the gas seems to be more abundant on the planet overall than oil, at least in more different shales. And then the Marcellus really is magnificent as a shale play.

The only point is not to lump everything together. Cornies want to say all shales are great. Peakers want to s#$% on all of them. But things can be different and maybe there is a middle road. The oily Bakken and Eagle Ford get a lot of press but the Marcellus is really pumping out gas.

I guess I’m sort of in the camp of Bakken/EF…OK, cool, but a bubble. But shale NG? Not a bubble.

Dave Thompson on Tue, 4th Mar 2014 7:12 pm

Very plain up front and easy to “get”. Northwest “it also does to anybody else with a brain that doesn’t have a deep psychological need to block out reality”. When those people “get” the message, is what happens next.

Northwest Resident on Tue, 4th Mar 2014 7:52 pm

“Marcellus is really pumping out gas.”

It has been shown that the average productive life of a Barnett Shale well is 7.5 years. From these early production results it looks as though these Marcellus wells may share that same short lifespan. The trend points to a 65-percent drop in production over the first 3 years, with further declines of 8 percent per year after that. Using that model, a Marcellus well’s average productive life would be 8 years. Gas liquids (alternately listed as either condensate or oil) production drops just as fast, if not faster, than the methane production shown in the charts below.

http://www.marcellus-shale.us/Marcellus-production.htm

Nony on Tue, 4th Mar 2014 7:57 pm

The initial IPs are very high and the drilling is low risk (few dry holes). So there are counterbalancing effects. The bottom line is production from Marcellus is booming. So, overall, the positive factors are beating the negative ones. The Red Queen is getting her mean old butt kicked.

🙂

Nony on Tue, 4th Mar 2014 8:06 pm

Marcellus production versus time

http://www.eia.gov/todayinenergy/images/2013.12.09/main.png

And that is happening DURING a period of relatively low prices. Not really the whole “we knew about the Eagle Ford, just needed prices high” dynamic.

http://www.infomine.com/investment/metal-prices/natural-gas/5-year/

Go gas! Even Obama likes it. 🙂

Northwest Resident on Tue, 4th Mar 2014 8:54 pm

“The bottom line is production from Marcellus is booming.”

And so is the stock market, right Nony? The good times are rolling. It is all up from here. Don’t let anybody tell you different.

Nony on Tue, 4th Mar 2014 9:45 pm

Put down the cyanide pill…

https://www.youtube.com/watch?v=yv-Fk1PwVeU

Davy, Hermann, MO on Tue, 4th Mar 2014 10:08 pm

put down the crack

Kenz300 on Wed, 5th Mar 2014 12:21 am

Even oil companies will be forced to change when the price of alternatives become cheaper than fossil fuels.

http://www.smartplanet.com/blog/the-take/the-energy-transition-tipping-point-is-here/?tag=nl.e662&s_cid=e662&ttag=e662&ftag=TRE383a915

bobinget on Wed, 5th Mar 2014 1:00 am

Energy companies only receive a dollar for every $1.50 spent on drilling operations

Experts: Energy independence through shale boom poses a challenge for U.S.

Achieving energy independence by developing shale oil reserves poses a major challenge for the U.S., according to industry analysts. Despite the shale boom, energy companies only receive a dollar for every $1.50 spent on drilling operations, while shale production decreases at a faster rate compared with conventional oil production, experts say. “We are beginning to live in a different world where getting more oil takes more energy, more effort and will be more expensive,” said Tad Patzek of the University of Texas at Austin.

http://www.businessweek.com/news/2014-02-26/dream-of-u-dot-s-dot-energy-independence-slams-against-costs-of-shale

Nony on Wed, 5th Mar 2014 1:31 am

Simple payback in 18 months. Not bad…