- The recent oil-price collapse confirms what we should have learned in 2007-8 about the influence of the last increments of supply and demand on price.

- This also means that future oil prices should be largely independent of the size of the oil market, even in a decarbonizing world.

In 2008, near the peak of a historic oil-price spike, the US Energy Information Administration (EIA) published a study projecting that opening the Arctic National Wildlife Refuge (ANWR) for drilling would reduce oil prices by no more than $1.44 per barrel, compared to their forecast without ANWR. Adding up to 1.5 million barrels per day to US production by 2028 would thus save motorists less than 4¢ per gallon. That result appeared during a Presidential election campaign that featured the slogan, “Drill, baby, drill!” and received significant attention. I hope the authors of that study have been watching the current oil price collapse, because it provides some useful lessons in how oil prices are determined.

Oil traders and most economists understand that oil prices are ultimately set by the last few million barrels per day of supply and demand in the market, and resulting changes in inventory. The oil price spike of 2007-8 provided firm evidence for this phenomenon, as rapidly growing demand and production problems eroded global spare production capacity to a level of around 2 million barrels per day (MBD) compared to more than 5 MBD in late 2002, prior to the Venezuelan oil strike and the start of the Iraq War. This may have been obscured by the rise of the widely publicized Peak Oil meme, which provided a more viscerally appealing explanation for high oil prices until it ran out of steam recently.

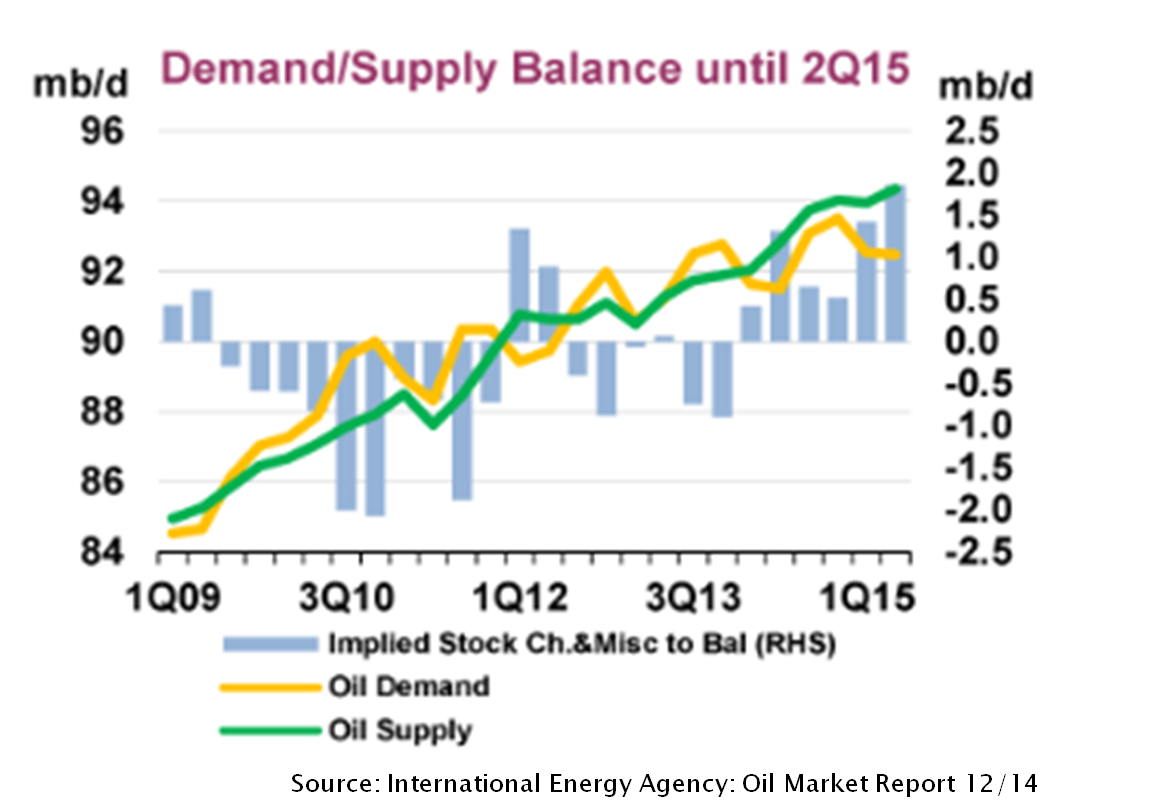

A chart from one of the International Energy Agency’s recent Oil Market Reports provides a neat illustration of the main factors leading to the recent price collapse. (See below.) Here, the emergence of a sustained surplus of 1-1.5 MBD starting in early 2014–less than 2% of the global oil market of around 93 MBD–was instrumental in depressing oil prices by more than half. Another factor was that, contrary to a key assumption of the 2008 EIA study, OPEC elected not to “neutralize any potential price impact of (additional US) oil production by reducing its oil exports.” While shale technology has expanded US oil output by a multiple of what the EIA expected ANWR might add, the benefit for consumers isn’t just pennies per gallon, but more than a dollar, at least for now.

Since the price of oil is set at the margin, then the oil price is also essentially independent of the total size of the oil market. That has important implications for how we envision the future of the oil market, especially in a world that is increasingly concerned about greenhouse gas emissions and transitioning to cleaner sources of energy. Even if future oil production were to be increasingly constrained by energy efficiency improvements and environmental policies, it doesn’t necessarily follow that future oil prices must be low. That would only be the case if producers mistakenly invested in more production capacity than the market actually ended up needing.

As things stand today, there is a significant risk that the industry will not invest enough in future capacity, and that prices will again rise sharply before electric vehicles and other alternatives could scale up sufficiently to fill the gap, particularly if low oil prices also deter their growth. That’s largely because without large investments in new oil output, current production will eventually decline from today’s levels. Field-level decline rates range from just a few percent to 65% per year, depending on whether we’re looking at the conventional oil reservoirs that make up over 90% of global supply, or at US shale production, which accounts for less than 5% of world oil.

Perhaps the bottom-line lesson is that we should never become complacent about the potential price volatility of what is still, at this point, an indispensable commodity. The shale revolution and OPEC’s current behavior don’t guarantee that oil prices must remain depressed, any more than previous concerns about Peak Oil meant they would remain high indefinitely.

shortonoil on Mon, 23rd Feb 2015 9:45 am

Perhaps the bottom-line lesson is that we should never become complacent about the potential price volatility of what is still, at this point, an indispensable commodity. The shale revolution and OPEC’s current behavior don’t guarantee that oil prices must remain depressed, any more than previous concerns about Peak Oil meant they would remain high indefinitely.

The PO community was right about petroleum prices becoming so high that the consumer could no longer afford it. They were wrong about where that price point occurred. It occurred at a point that was much lower than most guessed; it occurred in 2012 at $104/barrel:

http://www.thehillsgroup.org/depletion2_022.htm

The author is wrong in implying that there is going to be much of a price increase. Petroleum prices are now range bound, and that range is shrinking. As it shrinks producers will be continually priced out of the market; the highest cost first. With maybe as much as 4,200 Gb still buried in the ground, and oil “an indispensable commodity” it will be interesting to see how they explain the decline in the oil industry over the next five years. How long they will be able to hang on to their flawed supply/demand theories will be interesting. Given that they appear to regard them as divinely received proclamations, their paradigm shifts will likely be slow, and painful. Slow is the last thing that the world can now afford!

http://www.thehillsgroup.org/

jjhman on Mon, 23rd Feb 2015 4:02 pm

One thing very well stated in the article is that regardless of how accurately the peak oil “meme” described the economic/geological situation it has lost the ear of any decision makers including consumers making energy relevant choices.

I’m respectful of the hills group analytical work but must confess that the article’s discussion of the effect of pricing and marginal production costs has a credible ring to it.

Energy Investor on Mon, 23rd Feb 2015 9:53 pm

Consider the impact of mal-investment.

Few understand what the genesis was for the current price crash for oil.

1. Oil is hard won from the ground – each year getting harder, deeper and more risky and certainly far more costly – and generally there is a balance between supply and demand as no-one in the actual industry profits from the existence of surplus oil once refineries have been supplied and strategic reserves filled. For one thing, there is not storage for large surplus volumes of oil.

2. But Wall Street was not happy with that and felt that with oil becoming more scarce there could be a lot of money made by jumping onto the back of the shale plays in North America and so the Shale hype began. The problem is that with an extra thousand drilling rigs and USD700billion of surplus QE low cost money floating around looking for a home (with a high risk tolerance) they built a 4 million barrel per day of extra production within a couple of years – at a time when global demand was faltering.

3. The number of drilling rigs that moved into the shale plays became approximately half of the world’s total. The ready capital and the availability of expertise had all come together in a way that even astounded the industry. So what we have is a bubble in oil production due to mal-investment as much as anything else. Now we will face a bust. But the issue is that while drilling rigs are being sent back to the suppliers, wells are still being completed in larger volumes so the production will continue higher until the volume of well completions falls to match rig utilisation. Meantime the proportion of rigs being idled will likely continue to increase.

4. So production will fall later this year or early next, by sufficient to start driving prices back towards the level where even the marginal producers can break even. Meantime many shale producers and tar sands producers will go belly up or be the subject of takeovers.

This will be a time of complacency. Shale has been an American phenomenon and once it starts to fade by 2020 we will start to feel the scarcity but welcome the shale phenomenon as having been a range extender to BAU.

Just a pity about the investors who will likely lose their shirts in 2015/16.

GregT on Mon, 23rd Feb 2015 11:56 pm

EI,

“they built a 4 million barrel per day of extra production within a couple of years – at a time when global demand was faltering.

If those 4 million barrels per day were profitable at ~$10/bbl, we would have seen economic growth and an increasing demand for that oil. Global demand has stopped growing because our economies cannot afford higher priced oil, not because of increased production.

Davy on Tue, 24th Feb 2015 4:55 am

Naturally Short great comment.

EI, gives the coup de grace. EI hit the nail on the oil market side. This was a classic central bank induced gold rush. It was also happily for preppers like me a BAU extender. My family made a killing off the pipeline side in the last several years. The down side is the piper will be paid and what did the DC thieves and the WS parasites do with all that time. Nothing. The top has kicked the can down the road.

The party is definitely a retirement party now. The bumpy descent of demand and supply related destruction has begun no doubt with some market gyration. Yet, we will never see another oil gold rush. The conditions that allowed this are no longer together in a perfect hand. We had the expertise, the infrastructure, the capex, and the product to kick ass and take names. You got to hand it to those oil boys they are some wildcatters.

We are now likely in POD & past 1/2 way with ETP. This ensures we are in T-minus BAU’s end from a foundational commodity view point. The other numerous black swans are still there and ready to lite on the BAU pond at any time.

It is the oil brick wall ahead in no more than 10 years that is the end of BAU. There is nothing on the horizon to stop this runaway train. All other unconventional oil sources have been rendered beyond economic except as niche supplies. No other FF can be substituted for oil. No AltE can come close to filling the gap. This is the end folks the end days of BAU. In the meantime the relentless depletion of high quality oil is proceeding uninterrupted. Nothing can stop this because it is a law of nature.