Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on October 5, 2015

The US Shale Oil Industry Will Simply Vanish

After many years of prosperity, the tough time has come for the US shale industry.

Dramatic US oil production decline is inevitable and many shale companies face bankruptcy. Their assets can end up to larger producers, reinforcing market concentration. US energy independence can only be saved by government intervention.

US government will remove exports limitation and FED September rate hike suspension is related to the unsustainable debt levels US oil industry is keeping afloat.

But that is simply not enough to prevent a collapse of the US oil industry. From our research we learn that cost per barrel declined slightly but decreasing production cost is not enough to compensate for lower oil price. US oil production already declined 400K barrels per day from its April peak. We estimate an other 2 to 3 Million barrels can be wiped out the coming year.

A few months ago, when the oil price rise again before the June crush, the US oil industry seemed to be able to go through the difficult times. “It is too late for OPEC to stop the shale revolution”, “OPEC can’t stop the shale industry” – roared the headlines. However, after last publications of Energy Information Administration (EIA) the OPEC and Saudi Arabia are the only one to triumph.

In July, the EIA projected the expand of US shale supply in 2016, but it had to adjust its estimates to new conditions. Comparing to the first-half of 2014, the US crude oil prices declined by 47%, despite the fact that they passed 60$ in June and were up 40% from their lowest from March’s 43$. The nearest future looks worrying, as EIA forecasts the Brent crude oil average price will rise in 2016 scarcely to 59$ from average 54$ in 2015.

Nowadays, the main oil price factors are the economic condition of China and expectations of demand growth in emerging markets. The oil price seems to be closely correlated in recent months to China’s Purchasing Managers’ Index (PMI), which declined in August to 47,3, the lowest level in last six years. Also increased uncertainty of developing Asian countries affected the price.

At the same time supply is still going up. There is Iran at the horizon, with looming global crude oil supply. The agreement to ease sanctions will let the Islamic State next year get into the global market with its resources. Added supply could be almost twice as big as the production cuts by US producers. It all together with high stocks is not conducive to price increases.

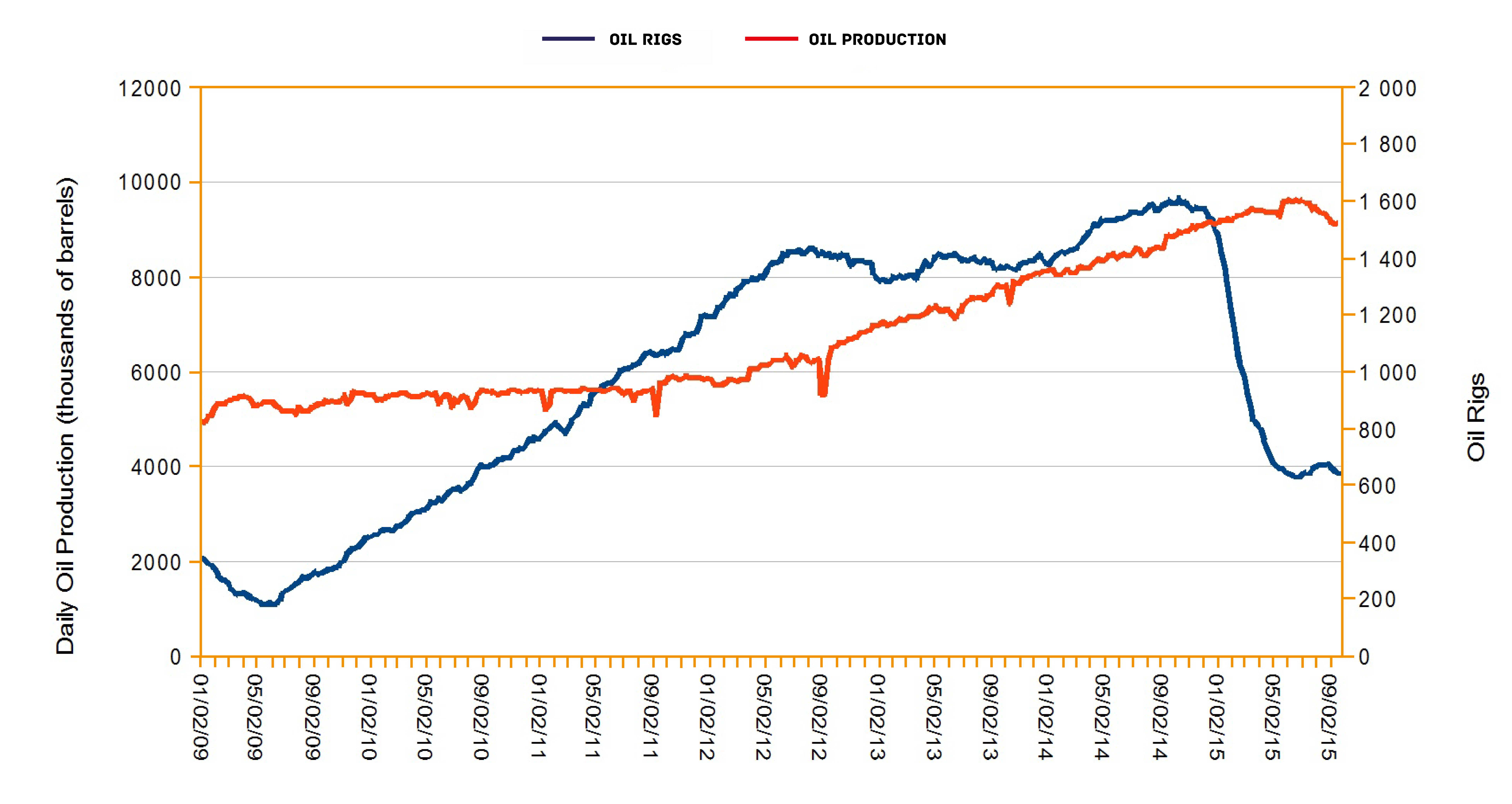

Low prices are forcing American shale producers to cut spendings and reduce output, which reached its highest level in April 2015, but then started to fall as fast as it growth. According to service company Baker Hughes Inc., the number of rigs drilling for oil slumped between October 2014 and August 2015 by more than a half, to 670 down from 1609.

Source: EIA

In such conditions production capacities are limited. EIA estimates that crude oil production will continue to decrease up to mid-2016. Some growth will resume barely in late 2016, just when the oil price will rebound, but average daily production in 2016 will be still lower by 300 000 barrels per day than in 2015. According to our analyses this estimation is far to optimistic. With rig count back at 2010 level we expect oil production will drop to 2010 levels, that is about 4 Million barrel a day less than the US produce today.

This is because of the poor production quality; shale oil wells produce only a very short time oil. The production start to collapse exponentially the moment a new well is in operation. Within 3 to 5 years these wells produce less than 20% of their initial production capacity.

The running cost for one well is about 20 dollar per barrel, even with current price enough to keep the well running. To create a well cost on average 35 to 40 dollars a barrel, US shale companies need 57 dollar a barrel. Most of the shale producers do get paid less than spot market prices exaggerated increasing their problems. This is due to transport cost and other miscellaneous market conditions.

The financial mainstream-media try to reassure investors that the rig production is going up, but forget to mention that the production per well is going down. This is because producers are now drilling more than one hole per rig. Producing oil has become a little cheaper but that is not enough to compensate for the low oil prices.

Industry starts to drop off. In the first half of the year US shale producers lost more than 30 billions of dollars. They are still struggling, but a rise in bankruptcies and restructurings is predicted.

Some of shale companies are highly indebted, so they need to pump the oil to gain enough money for debt payments. These producers cannot utilize the advantage of flexibility, as they are not able to adapt the scale of production to current oil prices.

Moreover, refinancing debt by taking a new debt on the old one has become more expensive. Interest rates for debt issuance for energy sector are the highest among the entire economy. Even regulators are warning of the risks related to lending to shale drillers, which raised over the first half of 2015 in debt and equity about $44 billion.

Shale oil producers can also compensate lower revenues by hedging, what in the first half of 2015 was a great relief, as net hedging assets stood at almost $9 billion for the nearly whole industry. However, many of these hedges, that secure loans, expire soon. Cutting the credit lines by bank can induce a wave of bankruptcies and a great fire sale of shale assets.

The probable term of turmoil is October, because then takes place second in this year valuation of reserves that bank use to determine the lending quotas. After re-determinations, some companies will have problem to collect enough money to pay liabilities and capital expenditures.

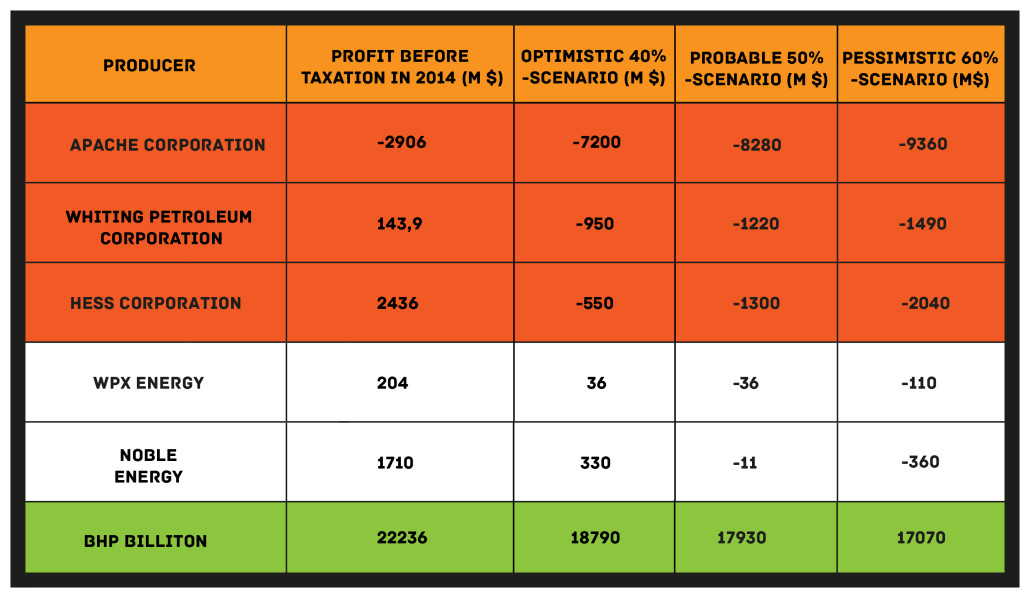

As a commotion comes, our team checked which one shale producer has a chance to remain in 2015 profitable. We analized six big companies, taking their production, revenues, costs and profits from previous annual income statements. Next, we created three scenarios: 40%-, 50%- and 60%-lower crude oil revenues for each of them. We assumed constant other revenues and constant costs at the level from 2014. As a result we gained profits before taxation in our three scenarios, showing if the company was ready for drop in revenues or not.

Table 1. Profit before taxation in 2014 and profits before taxation forecasts for 2015 in 40%-, 50%- and 60%-lower crude oil sales scenarios, assuming constant costs and other revenues at the level of 2014.

The numbers say emphatically that most of companies are at the edge, what is proved by latest quarterly financial reports. In the deepest slump is Apache Corporation from Texas, which had already troubles in 2014, finishing with loss of almost three billions of dollars. But the 2015 seems to be even worse! For the first half of the year Apache’s oil revenues are yet lower about 50%, what results in 13 billions of loss, comparing to margin income the year before. An enormous increase of additional oil and gas property and equipment cost is the main cause, though.

The only one company still without losses is BHP Billiton, which is not so dependent on crude oil price because of far wider activity, such as copper, iron ore or coal production. Moreover, American shale oil production is only a part of crude oil revenues. One third of them comes from Australia and other countries from different sides of the world. However, the income of BHP diminished clearly in the first half of 2015.

The year 2015 will be crucial and could be the beginning of the end of US Shale producers. However, it could be too strategically important for government. The collapse of shale industry means a return to energy-dependence on OPEC-states. As US Census Bureau data provides, since 2011 the share of crude petroleum and natural gas in total US Import have decreased every year, while total import has steadily grown up. Between years 2011 and 2014 general import of crude petroleum and natural gas fell by $84 billion. At the same time, the share of OPEC trade balance in total US trade balance decreased from 23% to less than 10% in 2014. The rescue of US shale industry or shale production could have strategic dimension.

One of the possibilities is removing US crude export restrictions. Opening the global market for US shale oil could results in increased domestic production. Removal of restrictions would not have significant influence on global crude prices. Removing export restriction will be not enough to save the industry.

Without government intervention the “invisible hand” of the world oil market will simply bankrupt US shale companies and with it destroys the US shale oil industry.

36 Comments on "The US Shale Oil Industry Will Simply Vanish"

Revi on Mon, 5th Oct 2015 12:51 pm

Ouch!

shortonoil on Mon, 5th Oct 2015 1:24 pm

The fact the US shale industry is a Dodo Bird waiting for the Fox to arrive is certainly no surprise to us. It is what we have repeatedly stated for the last two years. An energy company that can not deliver energy to the economy is heading for an extinction event. It has been one huge speculative, financial Ponzy scheme orchestrated by Wall Streets best manipulators.

What the article fails to mention is why in the face of more than a 50% decline in price the economy has not responded with a significant increase in consumption. Like our projection of the price decline months before it occurred:

http://www.thehillsgroup.org/depletion2_022.htm

we also projected that the economy would never again be able to utilize all the oil that the industry would produce. We explain what is really happening here:

http://www.thehillsgroup.org/

Plantagenet on Mon, 5th Oct 2015 1:30 pm

Predictions that the TOS industry will vanish are contingent on the oil glut continuing and oil prices staying low.

But the loss of TOS oil production in the US will help end the oil glut. Also, continuing slow growth in demand will boost global oil consumption by another 1-2 mm bbls/day next year, also helping to end the oil glut.

Cheers!

vegeholic on Mon, 5th Oct 2015 1:42 pm

A bailout would be expensive. Allowing exports would be a cumbersome and ultimately self-defeating exercise in futility. I think the path of least resistance for the government (that’s all it does these days) is to enforce price controls for oil. Of course this too will ultimately fail but it will seem like a good idea at the time, and will bring short term relief for the industry. High and seemingly stable prices will encourage much delayed exploration and production. The ensuing euphoria will be intoxicating for the producers. Unfortunately the economy still will not be able to afford it, so in hindsight it will have been a fruitless gesture. But that is no impediment to any of our many other, fruitless gestures.

apneaman on Mon, 5th Oct 2015 2:00 pm

short, it wasn’t a fox, it was an ape – the rapacious one.

rockman on Mon, 5th Oct 2015 2:23 pm

“It is too late for OPEC to stop the shale revolution”, “OPEC can’t stop the shale industry” – roared the headlines.” Only the headlines from fools who didn’t appreciate the lag time between when a well finishes drilling and first production from that well.

“One of the possibilities is removing US crude export restrictions. Opening the global market for US shale oil could results in increased domestic production.” {Eagle Ford Shale light oil was being exported to foreign markets from the beginning of the shale boom. The article below is from the San Antonio Business Journal in June 2014. Two pipelines from San Antonio to the port of Corpus Christi had been reversed to allow EFS production to be exported out of the US.}

“Valero Energy, operator of this refinery, opposes the easing of the federal oil export ban. Even with the ban in place, U.S. crude exports recently reached their highest level in 15 years, according to a federal analysis. “ {How odd, eh, to see the words “federal oil export ban” in the same sentence as “highest level (of exports) in 15 years”? Exactly how do we have the highest level of oil exports in 15 years if there is an oil export ban? }

{And besides bitching about oil exports what else has Valero been doing? From April 2014}:

“Moored at Valero Energy Corp.’s dock in south Texas, the Liberian-flagged Afra Willow is unloading 300,000 barrels of imported, semi-processed crude oil to the company’s Bill Greehey refinery, where it will be further refined into gasoline, diesel and petrochemicals. On the same dock, Valero is building a terminal to export light crude from Texas’s surging Eagle Ford field to the company’s refinery near Quebec City. Nearby, it is building two crude-processing units that will allow it to handle more light, Eagle Ford oil at the Corpus Christi plant.

The United States exported 268,000 barrels of crude daily {that’s 98 MILLION BBLS OF OIL PER YEAR} in April, according to the U.S. Energy Information Administration, which crunched the latest available federal data for its analysis. Exports began a sharp incline at the start of 2013 and have topped 200,000 barrels daily in five of the past six months.

“The increase in crude exports is largely the result of rising U.S. production, which reached 8.2 million barrels per day in March. South Texas’ Eagle Ford reached the 1 million barrel-per-day milestone in October…”. { I estimate that a minimum of 60 million bbls of Eagle ford Shale production has been exported.}

{And one last FACT}: “According to the EIA analysis, the U.S. Gulf Coast is a major beneficiary of the rising export levels. Gulf Coast crude exports averaged 134,000 barrels per day in the first quarter, nearly quadruple 2013’s record high of 35,000 barrels per day. Texas’ Houston-Galveston district handled around 75 percent of Gulf Coast exports during that period.”

And lastly: according to Baker Hughes there were 100 rigs drilling the Eagle Ford Shale under the current lower oil prices. That would equate to 600 to 800 new EFS wells per year. Certainly not as active as it once was. But not “extinct” either. LOL.

apneaman on Mon, 5th Oct 2015 2:23 pm

Energy firms face tightening credit lines as oil slump drags on

“Many oil and gas companies grappling with weak energy prices face two more looming problems: tighter lines of credit and a fresh round of reserve write-downs.

Every spring and fall, banks review credit facilities for energy companies, calculating how much they will lend companies based on the value of their reserves. They give weight to price expectations, the size of a firm’s reserves and the quality of its hedge book. Few energy firms will escape this autumn’s so-called “borrowing base” evaluation unscathed and, in turn, will be assigned less favourable revolving lines of credit.”

http://www.theglobeandmail.com/report-on-business/industry-news/energy-and-resources/energy-firms-face-tightening-credit-lines-as-oil-slump-drags-on/article26644644/

rockman on Mon, 5th Oct 2015 2:28 pm

vegeholic – “Allowing exports would be a cumbersome and ultimately self-defeating exercise in futility”. The only cumbersome aspect of exporting Eagle Ford Shale production is the roughly 2 week wait time for tankers in line at the port of Corpus Christi waiting to ship that oil to eastern Canadian refineries.

And again the amount of oil the US exports is rather small compared to the exported refinery products made from around 1 BILLION BBLS OF US OIL PER YEAR

apneaman on Mon, 5th Oct 2015 2:29 pm

Suncor launches hostile $4.3-billion bid for Canadian Oil Sands

http://www.theglobeandmail.com/report-on-business/industry-news/energy-and-resources/suncor-makes-hostile-43-billion-bid-for-canadian-oil-sands/article26648394/

BC on Mon, 5th Oct 2015 3:45 pm

http://www.ipaa.org/meetings/ppt/2015PCC/TheChangingAandD_MikeBock_PetriePartners.pdf

https://app.box.com/s/dt2c8mz6vgrq11q8p8i5tbkn3oqlckcb

shortonoil on Mon, 5th Oct 2015 3:49 pm

Both Pioneer, and Marathon attempted to export LTO. One load was shipped to Japan, and one to South Korea. The Chinese didn’t want any part of it. As far as I know neither Japan, or SK ordered additional product. The problem with US LTO is that it is very inconsistent, no two wells produce the same ratio of fractions. Since it is being used as feedstock, condensate from Indonesia, Qatar, and or Russia is preferred by users. US LTO will have a very hard time competing with much lower cost, higher quality product producers in other parts of the world.

penury on Mon, 5th Oct 2015 4:45 pm

If the Shale industry is deemed to be “essential to national defense” the bail out will be swift and complete. If the banks which made the loans to the shale producers squeal loud enough of course the industry will be too critical to fail.

BC on Mon, 5th Oct 2015 5:20 pm

penury, the precedent suggests that you are likely to be correct.

Davy on Mon, 5th Oct 2015 5:53 pm

Moral hazard. Does that mean anything anymore or has the term become irrelevant.

onlooker on Mon, 5th Oct 2015 6:06 pm

Why do I see the world now to be like a metaphor of a person drowning and just flailing in the water in futility .

kim on Mon, 5th Oct 2015 6:08 pm

The guy who wrote this article is illiterate. I have to believe his predictions and assumptions are suspect.

apneaman on Mon, 5th Oct 2015 6:33 pm

penury, this is why, short of armed revolt, one’s only option is to decouple from the system as much as possible before they suck you dry. All the G-20 countries have pension bail in legislation in place now. Why? Look for even more fee’s, fines and all sorts of hidden taxes and do not be surprised if every single utility gets privatized and the service goes down and the fees go up. Another hidden tax as far as I’m concerned – just goes to a different master is all. The TPP was passed late last night and there are 1 or 2 more to go and we will all be royally fucked. They will keep taking as long as the sheep let it go on and who knows what the upper limit on that is.

apneaman on Mon, 5th Oct 2015 6:58 pm

A New Kind of Frackademia? New Environmental Inspectors Offered Free Industry-Funded Classes on Fracking

“At an industry conference in Philadelphia last month, oil and gas executives gathered to hear about a little-known public relations effort with a very precise target: newly hired state and federal environmental inspectors.

At a seminar titled “Staying Ahead of Federal and State Regulations: A Partnership with Academia and Government,” officials from Pennsylvania State University and the University of Texas described how gifts from companies like ExxonMobil allowed their universities, along with the Colorado School of Mines, to offer state regulators free classes on oil industry best practices, travel and accommodations included.

“We’re targeting inspectors – oil and gas inspectors – who have three years or less of experience, although we do have lots of inspectors with different experiences on the course,” Dr. Hilary Olson, director of Education, Training and Outreach at the College of Petroleum and Geosystems Engineering at the University of Texas told attendees at Shale Insight 2015.”

http://www.desmogblog.com/2015/10/05/new-kind-fracademia-environmental-inspectors-offered-free-industry-funded-classes-fracking-and-drilling

MrNoItAll on Mon, 5th Oct 2015 8:39 pm

penury — From my point of view, the Shale industry WAS deemed to be “essential to national defense”, but has now lost its true purpose to a large extent, and growing smaller every day.

The national defense imperative for a long time (since 2008 at least?), has been to keep BAU chugging along. No BAU = No nation — no economy, total chaos for national security.

From the point in 2008 (or so) when the economy almost fell into the abyss, keeping BAU going has been a prime imperative.

A major centerpiece of the plan created to achieve that imperative was to PRETEND that we still had lots and lots of oil. We all know the extent to which the “shale revolution” was enabled only by government/FED policy decisions (ZIRP, QE, bailouts, looking the other way, etc..), in direct partnership with banks and financial powers.

They had to keep it going even if based on a lie. Shale was a great jobs program, it really revved up the economy for a while, it put a lot of people to work (in a few states) — it kept the wheels-a-turning, it bought us all some time!

Sadly, that ride is coming to an end. The myth of the great shale revolution is played out. Nobody believes it anymore. Investors across the board are losing their asses with a lot more of that to come.

Since shale is practically a zero-net-energy enterprise and a money-sucking demon from hell, there is no way that I can imagine that any attempt is made to bail out shale production — it just isn’t worth it.

I could be wrong, but if you ask me, it is Game Over. The illusion is BUST.

Now, give us a little time to mentally absorb that reality while we navigate our way into the Christmas season, while the stock market makes a few more “impressive” bounces, then we’ll begin to see what consequences are headed our way.

makati1 on Mon, 5th Oct 2015 9:05 pm

Well summed up, MrNo. Thanks.

Gil on Mon, 5th Oct 2015 9:18 pm

Does anyone proofread these messages before they are posted?? The writing is virtually on an elementary level. It does not inspire much confidence in the message.

MrNoItAll on Mon, 5th Oct 2015 9:29 pm

Gil — Most people are here to get the information and to focus on the message. None of us are turning in college assignments for grading here. Your post contributes zilch, and does not inspire much confidence in whatever “message” you might wish to convey. Are you serious? There are major issues and serious consequences being discussed here. And you’re complaining about “elementary level” writing? What are you? A journalism professor?

apneaman on Mon, 5th Oct 2015 9:43 pm

MrNoItAll, it was a Hail Mary pass, but not for the win; just to get us to overtime. It worked but now were down by 8 points, 45 seconds on the clock, on our own 2 yard line. QB Flutie is looking old and raggedy – I don’t think he has another miracle comeback in him.

GregT on Mon, 5th Oct 2015 10:16 pm

“The writing is virtually on an elementary level.”

Virtually on an elementary level?

Did you bother to proofread what you wrote Gil?

Joe Clarkson on Tue, 6th Oct 2015 1:35 am

Gil,

GEFIRA is a European site whose authors are probably not native English speakers (most likely German or Polish). I, for one, appreciate those who are willing to post interesting analysis in English even if their language has some mistakes. I think a little forbearance is in order.

Nils Hellevig on Tue, 6th Oct 2015 6:05 am

I guess there will be an import tax on crude to the US once the GOP is in charge. Kind of remember a $5 from last time prices were low (1999?) Guess it will need to be $30 to keep the frackers (and the financial system) afloat

rockman on Tue, 6th Oct 2015 6:19 am

In case some missed Greg’s point:

“virtually” definition: very nearly; almost entirely

“elementary” definition: of or relating to the most rudimentary aspects of a subject. Synonyms: easy, straightforward, uncomplicated.

Thus “virtually on an elementary level” = Almost entirely straightforward and uncomplicated.

Gil – Thank you for the compliment. Although the subject matter is rather technical and complicated most of us strive to communicate such thoughts as clearly as possible to our less informed cohorts here.

An effort I’m sure you greatly appreciate. LOL.

shortonoil on Tue, 6th Oct 2015 9:28 am

The shale industry gobbled up over $1 trillion to create an industry with gross sales of $360 billion per year. IF the industry produces a 10% profit margin on its sales it would take it 28 years to return the principal. For wells that become essentially stripper wells in five years the return of that principal is not going to happen!

The CBs have been printing gigantic quantities of unbacked, fiat currency for several years. In an overall stagnant economy, that money had no place to go except into high risk investments. HY Energy junk bonds received a good sized portion of that money. That allowed producers who otherwise could not have stayed in business to expand production. A lot of low quality, high cost oil that no one wanted hit the market, and prices fell 55%.

The economy can not grow because petroleum is no longer supplying it with enough energy to make that possible. In response to no growth the CBs will continue to print. More money with no place to go will enter the market allowing producers that should be shutting their doors to keep pumping. Prices will continue downward until no one can afford to supply oil.

The underlying problem is an energy deficiency resulting from the ongoing depletion of petroleum. Intensifying that problem is a banking system that must have an expanding monetary base to remain functional. The money supply must grow for the funds to exist to service existing debt. Once the money supply falls to a specific level cascading defaults begin to occur, and the entire system shuts down.

There are two events taking place. (1) The energy supplied by petroleum will continue to fall until the overall economy can no longer be maintained. (2)The monetary system can not generate enough currency to maintain itself, and also allow for the production of an adequate enough supply of petroleum so the economy can function.

The question raised by the first event we have a specific answer for; the second one is yet unknown. It will, however, be very apparent when that answer arrives!

http://www.thehillsgroup.org/

Davy on Tue, 6th Oct 2015 12:33 pm

notice a trend?

http://www.zerohedge.com/sites/default/files/images/user5/imageroot/2015/10/IMF%20World%20Oct%202015.jpg

Kenz300 on Tue, 6th Oct 2015 12:38 pm

Banks have stopped lending…….. fossil fuels are investments in the past…..

Wind and solar investments are growing around the world.

Solar Beats Gas in Colorado – Renewable Energy World

http://www.renewableenergyworld.com/articles/2015/08/solar-beats-gas-in-colorado.html

Bob on Tue, 6th Oct 2015 4:49 pm

The sole purpose of this site is the prediction that oil production is in decline, we are currently in an oversupply situation. Does anyone else find this comical? The site is now making a prediction based on the fact prices fell because we were too successful and have been producing more oil than we need, hence the fall in prices and the problems with US shale producers. I would think that a site whose sole purpose is ‘peak oil theory’ should not be allowed to make predictions at this time.

Kenz300 on Tue, 6th Oct 2015 5:26 pm

A good article explaining the cost benefits of moving to wind and solar.

Solar and Wind Just Passed Another Big Turning Point

http://bloom.bg/1WK34MZ

Margo Cooper on Wed, 7th Oct 2015 10:35 am

The post above that is referenced as poorly structured grammar is probably due to an ESL writer– the content was intelligent and coherent despite the number of ESL mistakes. I’m a certified ESL teacher. I only stumbled on here trying to find out why there are always so many tankers lined up waiting to come into the Port Aransas channel.

BC on Wed, 7th Oct 2015 11:46 am

Forgive the cross-posting from other threads, but I wanted to catch some of the newcomers.

https://app.box.com/s/8f0rm31psk7thwtd5j3gwgrtx8acmo8t

https://app.box.com/s/ys8ijadj4b57nb95ka0b3ilph38ga7fm

https://app.box.com/s/x61sqtg4c3vp1ubo67k8715ulapw35me

https://app.box.com/s/894h3w9iool3d07cnadqa21tmg89xu8n

Oil is “cheaper”, but it still ain’t “cheap” WRT to the economy’s capacity to grow at current oil prices and supply.

https://app.box.com/s/s0wyvm4xh7kvd4fxcwyxx3mfevtf8yub

And US oil is still being depleted per capita at a steady, log-linear rate (falling 50% per capita by no later than the early 2020s).

https://app.box.com/s/dt2c8mz6vgrq11q8p8i5tbkn3oqlckcb

https://app.box.com/s/6aju2cctaq9wxck2y6xwxdfbqidq95op

https://app.box.com/s/u3icgvx6wbcddnijynhx257dshzm1dyr

Rigs are contracting with the oil cycle, and production will eventually follow.

BC on Wed, 7th Oct 2015 11:48 am

Davy, see here:

https://app.box.com/s/xt8fhcxp62igds328g7q6mzorpytq9pw

Davy on Wed, 7th Oct 2015 12:04 pm

Thanks BC, impressive graph.