Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on July 21, 2015

How plunging oil prices have created a volatile new force in the global economy

He’d spent years touting his vision that America would one day dominate one of the world’s most powerful markets. And when Harold Hamm, a pioneer in discovering vast reserves of shale oil under American soil, took the stage in front of several hundred oil luminaries, he never acknowledged that the narrative was in doubt.

“For the next 50 years, we can expect to reap the benefits of the shale revolution,” Hamm said one day this spring. “It’s the biggest thing that ever happened to America.”

But away from the stage, the US oil industry – and Hamm – was in crisis.

In the previous six months, Hamm, founder of oil giant Continental Resources, had lost $6.5bn, more than one-third of his net worth. The industry that Hamm had helped create was facing its greatest test in a frantic race to stay profitable as rival Saudi Arabia worked to drive down oil prices and, according to some analysts, undermine America’s oil industry at the most important moment in its history.

Behind the low price of a gallon of gas at the pump this summer lies a competition worth trillions of dollars that is capable of swinging the geopolitical balance of power. On one side are Hamm, a famous wildcatter, and other American oilmen who rode the discovery of hydraulic fracturing to tens of billions of dollars of wealth and a promise of, in Hamm’s words, ending the “disastrous” days of Saudi Arabian control. On the other are the Saudis and their allies in the Organisation of the Petroleum Exporting Countries (Opec), which are trying to stem rising US oil power and maintain their 40 years of dominance.

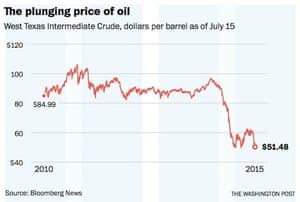

This month, the cost of West Texas Intermediate oil, a US benchmark, has been hovering at just over $50 a barrel – down from about $110 over the past year. Meanwhile, the number operating oil rigs in the country has fallen to just 645. That was lowest rig count in almost five years, down from more than 1,500 a year ago. Opec said last month that it would continue to pump 30m barrels a day, despite low prices, sending a strong signal to US competitors that it had no plans to let up the pressure on the Americans.

And now there is a new pressure on the scene. The decision to strike a nuclear agreement with Iran, which has more oil reserves than all but four Opec countries, will over the coming months unleash new Iranian oil into the markets. Analysts expect Iran to pump 1m or more barrels a day as a result, so the prospect of the deal has been driving prices down in recent weeks – by about 15% – interrupting a stabilising in the price of oil since the big plunge last year.

Even before the Iran news, the clash between the US and Saudi Arabian energy interests had created a volatile new force in the global economy and unprecedented challenges for the two largest producers. The Saudis need high prices to fund their nation but have lost control of the market because of the oil boom in the world’s largest economy. The United States, after years of easy growth, is grappling with painful adjustments –including tens of thousands of layoffs – with the hope of staying viable amid the price collapse.

At stake is not just the price of filling up a car but America’s energy independence and one of its most vibrant industries. The fallout will ultimately determine whether cheap oil is a mere blip or will continue for years.

In the past, when oil prices fell, the Saudis and other oil-rich states would step in, pulling back on production and letting prices rise. But this time, the price fell in part because of the substantial increase in US energy production. Instead of acting to shore up the market, the Saudis increased drilling themselves, sending oil prices plunging and threatening US drillers who rely on oil prices being high.

“For the last 20 or 30 years, it was almost like Opec could flip the switch and change things as they wanted,” said Mike Terry, president of the Oklahoma Independent Petroleum Association and an acquaintance of Hamm’s. “Well, they don’t have that power anymore.”

Nearly a year into the oil contest, senior players in oil capitals from Riyadh to Houston are making risky bets about their next moves. Riyadh is continuing to pump, even as that puts its own petro economy on shakier footing.

For the US, the risk is that sustained cheaper energy prices will derail what had seemed only months ago like an inexorable energy revolution, one that was helping to power a still-recovering economy.

“A tidal wave scenario,” Ryan Lance, chairman and chief executive of ConocoPhillips, said in Houston, describing the forces that were challenging producers across the world. “The industry is in a bit of survival mode.”

The Saudis have a built-in advantage in this global contest. They have some of the easiest-to-access oil on Earth, including a single field – the massive Ghawar – that produces more oil daily than any other Opec member.

Many state oil companies, from Venezuela to Nigeria, are corrupt, analysts say. Saudi Arabia’s state oil company, known as Aramco, is anything but. Aramco’s facilities glisten with a campus of housing facilities, classrooms and training sites.

In Houston, at the same conference Hamm attended, hosted by consulting firm IHS, an Aramco oil executive made clear that the Saudis, with many advantages over the Americans, were not going to let up during a downturn. Pulling up logos of fallen American companies on the screen – Kodak, Polaroid, Compaq – Muhammad Saggaf warned: “If we look back, we will see history littered with examples of successful companies that were at the front of the race but in a very short period were relegated to the back … because their competitors won the innovation race.”

During the decades of Saudi dominance, crude prices stayed low, but spiked mightily during wars in the Middle East and oil embargoes. More recently, prices reached a new plateau above $100 a barrel given the demand for energy from China and India. All the while, US fracking companies improved their technology to harness oil from regions that were never thought to offer much in the way of energy.

Eventually, amid a slowing economy and a growing awareness that US oil discoveries were enough to make America energy independent – and potentially even an exporter of petroleum – prices began a steady decline. Then, in late November, for the first time, Saudi Arabia embarked on a new strategy, refusing to cut production to prop up prices. That decision turned a gradual price decline into a free fall.

The Saudis were influenced by a bitter memory from the mid-1980s, when declining global demand had led to a similar oil glut. To try to keep prices stable, the Saudis went from producing 10m to about 2m barrels per day. Its customers flocked to other Opec nations, and the Saudis fought for years to get them back.

“We learned from that mistake,” Ali al-Naimi, the nation’s oil minister, said at a March conference in Berlin. “Today, it is not the role of Saudi Arabia, or certain other Opec nations, to subsidise higher-cost producers by ceding market share.”

Aramco declined to comment for this story.

The new Saudi strategy has caused ripples across the world, knocking off pricey drilling operations everywhere from the Arctic to South America. More broadly, lower energy prices have delivered a blow to oil-dependent nations, pressuring state-run oil firms, causing a currency slump in Nigeria, and contributing to major economic contractions in Venezuela and Russia.

Some experts also say that the Saudis are hoping to cut off the fracking boom at its knees. If they’d allowed prices to stay high, US production would have continued to grow rapidly.

“And they’d be asked to cut again and again, losing market share,” said Jamie Webster, a global oil markets analyst at IHS.

The Saudis have huge advantages beyond their plentiful reserves. Hundreds of US companies can’t adjust as quickly as one state-run oil company. Saudi Arabia can bring its oil to market in weeks. US frackers need six months or longer, because their oil is more difficult to access. If US companies choose to raise production, they also face the challenge of coaxing laid-off workers back into the oil fields – in some cases after they’ve returned to their home states and found new jobs.

But the choice isn’t simple for Saudi Arabia, which is grappling with a leadership change and a military conflict with neighbouring Yemen. Despite decades of attempts to diversify the economy, oil revenues essentially subsidise the state.

Sustained lower oil prices will “put the Kingdom’s savings from earlier oil revenue booms at risk of depletion”, Khalid Alsweilem, a former investment director at the Saudi Arabia Monetary Agency, wrote in a recent report published by Harvard University’s Kennedy School.

Hamm rose from poverty in Oklahoma, the 13th child of a sharecropper, and spent the early part of his career working dirty oil jobs, cleaning tank bottoms and trucking supplies to drilling sites. But he grew obsessed with the idea of the big strike, the discovery of treasure in the ground, according to The Frackers, a book about the nation’s new oil billionaires. He started a tiny company in 1967 named after his two daughters, used the proceeds to pay for geology classes and learn about computer mapping, and ultimately bought up land on the cheap in hard-to-drill places like North Dakota.

Hamm’s company, renamed as Continental Resources, grew into an oil giant over less than a decade thanks to new but pricey drilling technology that opened access to a previously out-of-reach bounty. “Thank God we had good oil prices,” Hamm said at a Continental event last September, with oil at $97 per barrel.

“One time everybody was looking at the sunset of the [American oil] industry,” Hamm said. “We’ve seen America driven to a new era, if you will.”

But the price collapse has put the United States’ – and Continental’s – continued rise in doubt.

Since last fall, US drillers have shuttered 60% of their rigs, seen share prices tumble with little recovery, and laid off tens of thousands of workers who might not return even if prices were to recover. Only a handful of companies have so far faced questions about their solvency, but they have been furiously cutting projects that are no longer viable. The pullback has been severe enough to slow down the broader US economy, which for years had been powered by oil job growth and investment.

“There was an irrational expectation that the market for US oil was unlimited,” said Michael Levi, an energy specialist at the Council on Foreign Relations. “It led to a lot of ill-advised investment.”

The oil prices of the previous years – $111 per barrel in 2012; $108 per barrel in 2013 – had helped Continental grow at a breakneck pace. In early September 2014, Continental stock hit $80 per share, and Hamm, who owned 68% of those shares, was worth more than Rupert Murdoch.

But then prices started to fold.

The downward slide has left Continental particularly vulnerable because Hamm bet wrong on what would happen in the oil market. As oil began its slide in early November, Hamm believed that oil had reached its “bottom rung”. So he sold off Continental’s hedges, netting $433m in cash while losing his assurances that he could sell oil at a fixed price.

The company, in industry parlance, was “going naked”, fully exposed to the markets. Then, on the day after Thanksgiving, Opec held a meeting in which the Saudis determined that they’d no longer work to balance the market. Though Hamm perhaps saw that part coming, what he didn’t foresee was how the markets would react: they freaked out.

“In hindsight, it was not the right decision,” said Leo Mariani, an analyst at RBC Capital Markets who follows the energy industry.

Continental declined to make Hamm or other executives available for comment to describe company decision-making, but responded to several questions by email.

Warren Henry, Continental’s vice-president of investor relations and research, said by email that “no one anticipated the rapidity of the price drop, in part because it was based on price-cutting actions by Opec members rather than supply/demand fundamentals alone”.

Continental is a much different – and smaller – company than it was a year ago. It’s pressured suppliers to lower their costs and has fewer rigs in fewer places. In the Bakken formation that made Continental famous, operations were once spread across eight counties. Now, Continental works only in a tight cluster where oil is cheapest to come by.

“Last year, I could sit on my deck and count 60 trucks in an hour,” said Jean Nygaard, a Divide County resident who leases her farmland to Continental. “Now, I can drive to work 28 miles [45km] and not see a vehicle.”

Today, the US oil industry is trying to feel out what will happen next. Some figure an increase in oil prices has already been set in motion, triggered by the fact that so many companies have cut down on searching for the next place to drill. Without exploration, companies can maintain production for one or two years. But not for a half-decade.

Hamm has come to interpret the events of the last half-year as a sign of US oil’s staying power. Continental lost $33m in the first three months of 2015, but Hamm says the company will be able to tread water for the rest of the year – and quickly ramp up if oil prices touch $70, something he says “could happen fairly soon”.

“We are adapting well to the new price environment,” Hamm said. “It’s a great time to be in the American oil business,” he added. “America will again be an energy superpower.”

16 Comments on "How plunging oil prices have created a volatile new force in the global economy"

jjhman on Tue, 21st Jul 2015 12:35 pm

This seems a relatively well thought article except for two issues:

-First where the author comments that the US could become energy independent and even export oil. That is total fantasy.

-Second he doesn’t mention the debt bind that most fracking companies are in. We’ve seen several studies recently that suggest that none of these fracking companies have made enough money to pay off their loans. If interest rates go up this year, as expected, they are going to be in worse trouble.

shortonoil on Tue, 21st Jul 2015 12:36 pm

“The industry that Hamm had helped create was facing its greatest test in a frantic race to stay profitable as rival Saudi Arabia worked to drive down oil prices and, according to some analysts, undermine America’s oil industry at the most important moment in its history.”

Ham the savior of the American way of life, WOW! He build a fortune selling an industry that was thermodynamically, and economically non viable. It is now melting down into the puddle of nondescript hydrocarbons that it is. But, the taxpayer should step forward and save it from the evil devises of the the foreign Middle Eastern oil thugs who absolutely refuse to pay for it. Of course, there will be many people who believe his story. I’m not one of them.

BC on Tue, 21st Jul 2015 1:05 pm

http://www.bloomberg.com/news/articles/2015-07-20/wall-street-lenders-growing-impatient-with-u-s-shale-revolution

@shortonoil, the Wall St and rentier plunderers appear to be recognizing that they jumped in too soon, thinking that oil was going to spike higher with accelerating global growth of demand.

Oops!!!

http://schrts.co/QQBFdG

http://schrts.co/LtRsm8

And now junk debt is setting up what could be another Lehman-like event to suck the air of liquidity and speculative complacency out of the crowded room, so to speak. No doubt energy junk and emerging market debt will take the blame this time around.

https://www.tradingview.com/x/mBfMTUqM/

If JNK cracks 37.50, run for the hills from corporates and equities and get ready for a 1-1.25% 10-year yield. No Fed rate hike but rather more likely a resumption of QEternity at perpetual ZIRP, as in Japan since the early 2000s.

Boat on Tue, 21st Jul 2015 1:45 pm

BC to you remember when GW was president? He encouraged business and families to spend money. If you read the MSM it was popular and smart to leverage your homes and spend or investment in the stock market. They didn’t check the credit and history of potential home owners. Then institutions rated the loans AAA. Now Obama and Bernanke invented the wild use of quantitative easing, Now it’s cheaper to buy than rent with little down payment. How are they rated? No clue but I agree another bubble has been formed. So what else is new. Eventually we will elect somebody that will end the bubbles and busts through education and better, more savvy politicians. How about increasing the amount of money set aside by the banks and the amount of insurance required by bond isseres.

rockman on Tue, 21st Jul 2015 2:04 pm

“And when Harold Hamm, a pioneer in discovering vast reserves of shale oil under American soil…” The Bakken and Eagle Ford Shale were discovered to be oil bearing reservoirs when Harold was a teenager. Harold didn’t invent frac’ng or horizontal drilling. And although he was a great oil man, George Mitchell, didn’t either.

What they do get credit for was recognizing the economic value of applying those technologies to these reservoirs once oil prices got high enough to justify the effort. Just as dozens of other companies recognized at about the same time. But none of them did better than Petrohawk IMHO: they picked up thousands of acres cheap, drilled some “seed wells” and then sold 100% of their lease position for $15 billion.

Boat on Tue, 21st Jul 2015 2:11 pm

Rock,

What are they buying now and do they have stock. Lol

ennui2 on Tue, 21st Jul 2015 2:26 pm

The only phrase doomers should pay attention to in this article is the headline “plunging oil prices”.

Any attempt to bend this into some sort of near-term fear-mongering related to peak-oil is ludicrous. If fracking companies go bust, the land they were drilling will just pass to others when the need arises to drill again and the market will extract that oil.

penury on Tue, 21st Jul 2015 3:03 pm

The main emphasis is as always sell the sizzle not the steak. Harold may be the smartest man in the room, so what, he is rich, so what? he said something right? Tomorrow there will be someone else and the fay after some one different. None of it means anything, including my comments.

shortonoil on Tue, 21st Jul 2015 3:14 pm

“None of it means anything, including my comments.”

Disagree! Your comments are usually well thought out, and worth the effort of closer inspection. Thanks.

rockman on Tue, 21st Jul 2015 4:25 pm

Boat – “What are they buying now and do they have stock.” The new company is called Halcon Resources (Halcon = a Mexican hawk). They pumped the better part of $1 billion in what they had hoped to be an extension of the EFS onto eastern Texas. the rumor is that they are loosing their butts. Their stock hit a high of $39/share in Aug 2011. It’s now trading for $1/share…a 97% decline. And it was trading for only $2/share before the price collapse.

Too bad you didn’t get to buy in early on. I’m sure you could have used the write off. LOL.

Everyone is the oil patch is a f*cking genius…until they aren’t LOL.

Boat on Tue, 21st Jul 2015 5:42 pm

Rock,

Two comments, sometimes your the hammer, sometimes your the nail. Sometimes your the bug, sometimes your the windshield.

shortonoil on Tue, 21st Jul 2015 6:34 pm

“If fracking companies go bust, the land they were drilling will just pass to others when the need arises to drill again and the market will extract that oil.”

It looks like the financial industry is getting tired of the shale song and dance:

http://www.bloomberg.com/news/articles/2015-07-20/wall-street-lenders-growing-impatient-with-u-s-shale-revolution

38% of shale has an API > 50. Shale never was profitable, and never will be. It lacks the molecular structure to make producing fuels from it cost effective. Once shale shuts down it will stay shut down until some comes along who can afford a lot of plastic pipe. Feedstock and diluent was all it was ever good for, and it is all it ever will be good for. Nature over cooked it several million years ago!

BC on Tue, 21st Jul 2015 6:42 pm

Boat, right. The period since the late 1980s has been a process of deindustrialization, decapitalization and deskilling of labor, financialization, and feminization of the labor force and economy (not a sexist statement but an observable fact), which reduced real wages and productivity of labor after the effects of increasing debt to wages and GDP.

US capital formation to GDP is now at the level of the early to mid-1990s, even as debt and equity market capitalization has risen to a record bubbly high to wages and GDP via record leverage.

The debt and equity claims by the top 0.001-1% to 10% on the bottom 90% now preclude any real growth per capita after debt/equity claims on wages, profits, and gov’t receipts in perpetuity.

We don’t know this because those who are in the position to inform us have been captured by Wall St., the CEO caste, the corporate media, and the top 0.001-1% who own everything.

Besides, we have been conditioned for 40-50 years to care more about tattooed sports thugs with an 87 IQ; porn stars with cup sizes larger than their IQs; NASCAR; Kardashian’s fat a$$; Ms. Bruce Jenner’s dress and bust sizes; and the British Royals’ breeding habits.

G-d bless/damn ‘Merika?!

Brent on Tue, 21st Jul 2015 7:23 pm

Yes short this needs to be the front page of every newspaper in this country. http://www.bloomberg.com/news/articles/2015-07-20/oil-guru-who-called-2014-slump-sees-return-to-100-crude-by-2020

Boat on Tue, 21st Jul 2015 7:53 pm

BC, You and apeman come up unique ways to string together words. I enjoy it. I am just a high school graduate with a passion for reading.

I have been concerned over advantages for the more well off in the tax code and business as well for three decades. I also think our passion for military spending is most of problem in the US. If you go and add the deficit up every year for the last 25 years you will find it surpasses our debt of 18 trillion. If you add up the interest on the debt for the same time period it is over 8 trillion. I did this math several years ago and it has only gotten worse.

You can look at tax compliance in the US, it runs over 450 billion.

Another headwind is immigration which I agree is and has been a huge problem for the world as resources tighten in a finite world.

I would rather focus on oil energy and what improvements can be made like this.

Under the new rule, a best-in-class, long-haul truck carrying 68,000 pounds of cargo is expected to get at least 10 miles per gallon, up from a range of 5 to 7 miles per gallon today, the EPA said. Vehicle owners would recoup costs associated with the rule within two years because of reduced fuel consumption, officials said.

http://www.usnews.com/news/politics/articles/2015/06/19/epa-proposes-tougher-mileage-standards-for-trucks

apneaman on Tue, 21st Jul 2015 8:09 pm

Boat, I dropped out of school in grade 9. Reading, life experience and paying attention is how I learn too.