Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on December 20, 2014

A Continent of New Consumers

Africa has the foundation for an exceptionally long runway for consumer spending.

Morningstar’s long-term approach to analyzing companies requires careful analysis of Africa, which we expect to become an increasingly fertile region for consumer spending over the next several decades.

Several tailwinds drive these expectations: favorable demographic trends, including a large, young, and rapidly growing population; wealth creation and the growth of Africa’s consuming class; urbanization and infrastructure investments; and favorable regulatory reform.

Many consumer staples firms have been slow to act because of historical government instability, commodity price swings and the impact on consumer spending and raw material costs, and the perception of poor returns on infrastructure investments. These fears have slowly been placated, however, with consumer companies coming to the realization that Africa offers an opportunity to extend their brand and develop economies of scale. Companies with moats are especially poised to take advantage.

Youth Served

According to U.N. projections, Africa’s population is expected to grow from approximately 1.1 billion to 2.4 billion by 2050. This represents a compound annual growth rate of 11.3%, outpacing world population growth estimates of 4.4% and collectively making it one of the highest potential emerging markets across the globe. For perspective, China and India are expected to have a collective population of 2.9 billion by 2050, and the United Nations forecasts that Africa will surpass the collective population of these two regions by 2065. To capitalize on this large addressable audience (both from a potential spending and workforce perspective), we believe companies will increasingly migrate to Africa in the decades to come.

Africa is also made up of a younger population than many emerging markets, with a median age of 19.7 years, using U.N. estimates, compared with just over 30 in Asia and north of 40 in Europe (Exhibit 1). Over the next several years, we expect dependency ratios (the number of children and elderly supported by each working individual) to decline, freeing up income for additional personal consumption. Moreover, we believe regulatory reform has accelerated over the past decade, breaking down many trade barriers in the region and allowing for new infrastructure and workforce investments by foreign companies that should help to stabilize many economies across the continent.

Younger African consumers have not only become important to the region’s economies, but like many developed economies, they have also become more brand-conscious and technologically savvy.

In our view, this portends major changes in consumer consumption patterns in the years to come. According to an October 2012 McKinsey survey of African urban residents, 16- to 34-year-olds account for 53% of the continent’s income. Additionally, 53% of 16- to 34-year-olds claim to follow the latest fashion trends (versus 33% for individuals older than 45), and 67% are active online (compared with just 32% for individuals older than 45). We believe these developments are important for many consumer staples companies, as we think it is vital to start cultivating brand intangible assets now given the lifetime of potential transactions that the typical African consumer represents. This dynamic is particularly noteworthy for alcoholic beverage companies, which will have access to a much wider population above the legal drinking age at a time when they are adopting new taste preferences that will carry through to adulthood.

Wealth Catalyst

A natural byproduct of Africa’s growing population, an expanded government and corporate workforce, and infrastructure investments, wealth creation will be a key catalyst for consumer spending growth over the next several decades. Africa’s workforce is currently made up of approximately 382 million people, with another 122 million expected to enter the workforce by 2020, according to McKinsey. This suggests that Africa’s consuming class could reach 500 million by 2020 (representing more than a third of the continent’s projected population), offering a consumer base that will be difficult for most consumer staples companies to ignore.

A move toward a salaried job culture and away from traditional government and agricultural activities will drive the rise of the African consuming class. According to the International Labour Organization and McKinsey, almost 60% of Africa’s labor force was composed of government and agriculture jobs in 2010. Over the next several decades, we anticipate a shift into more commercial agriculture professions (commercial farming on underdeveloped land, crops for biofuels), which we expect will play a major role in global infrastructure investments across the globe.

We also think manufacturing, service, and technology professions will become more commonplace in the years to come, as foreign and domestic firms capitalize on Africa’s vast labor pool and infrastructure investments. In fact, many African nations have wage rates and productivity levels that are competitive with other cost-effective manufacturing regions such as Southeast Asia, which should present a key tailwind for manufacturing growth. Additionally, with increased urbanization and modernization, we believe that demands for retail, technology, hospitality, and other leisure services will naturally emerge, creating even more labor opportunities.

After combining population growth, rising wages, and infrastructure investments, it’s not surprising that African economies are growing more rapidly than most regions of the world. Over the past 10 years, Africa collectively posted a GDP annualized growth rate of 4.7% (compared with 2.7% globally) and is home to six out of the 10 fastest-growing economies, according to The Economist. Over the next several decades, we expect GDP growth in the region to increase exponentially, growing to potentially $30 trillion by 2050 from about $2 trillion today, rivaling Asia’s economic growth at the end of the past millennium.

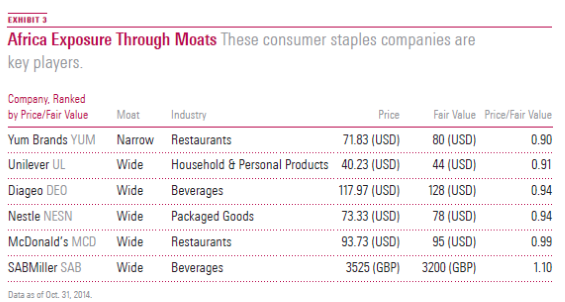

Africa’s wealth creation directly ties to the topic of premiumization. Many consumer product companies with exposure to Africa have reported stronger growth numbers among their more affluent brands in recent years, which we expect to continue. For this reason, we tend to find wider economic moats among those consumer staples companies with expansive product portfolios across a varied range of price points. In our view, this allows for natural trading-up opportunities and the ability to shape consumer preferences. Although luxury and other premium categories tend to be the most lucrative for consumer companies from a profitability standpoint, we believe entry-level products can be margin-accretive because of economies of scale advantages (one of the five moat sources Morningstar uses to assign economic moat ratings). Several large consumer staples companies, including  Diageo (DEO), Unilever (UL), and SABMiller (SAB) have noted that scale typically reduces per unit costs, enabling excess economic profits among mainstream brands as well.

Diageo (DEO), Unilever (UL), and SABMiller (SAB) have noted that scale typically reduces per unit costs, enabling excess economic profits among mainstream brands as well.

Living in the City

We also expect urbanization will be an important revenue driver for consumer staples companies with exposure to Africa. Roughly 40% of the African continent lives in cities–a percentage similar to China and surpassing India–compared with 28% 30 years ago. 2030 is estimated to be the tipping point when more Africans will reside in urban areas than in rural areas. By 2050, the United Nations estimates that two in every three Africans will live in cities. By 2050, nine African countries are expected to have urbanization rates of more than 80% with an additional 23 countries between 60% and 80% (Exhibit 2).

Urbanization is driving infrastructure investments. Since 2000, Africa’s annual private infrastructure investments have tripled, averaging more $19 billion from 2006 to 2008, according to data from McKinsey. We believe urbanization will change consumer consumption patterns across a wide number of consumer staples categories. Additionally, according to the U.N. data, 70% of African urban population growth is expected to take place in smaller cities, which are conducive to increased direct-to-consumer sales given current infrastructure limitations. Further, as population density and high Internet penetration rates increase, we believe this will lower the incremental cost of shipping (particularly among last-mile deliveries).

Regulatory Reform

Over the past several decades, direct investments in African companies have generally been an uncertain proposition, owing to fiscal mismanagement by governments, corporate corruption, rising inflation and monetary tightening by central banks, rapidly evolving marketplace structures (including the threat of nationalization in more extreme cases), and a constantly changing regulatory environment. Today, we see a much different picture for Africa’s regulatory environment. Government corruption is no longer the norm, corporate fraud has dwindled, and the regulatory environment is less volatile.

A key point of consideration in Africa from a regulatory standpoint is evolving tax and tariff practices, which can spur dramatic changes across consumer categories. This is relevant in the alcohol category, where we’ve observed many governments providing more balanced duties across different beverage categories. Diageo, in particular, has been active in working directly with many African governments, suggesting optimum duty collection practices and rates. (Multinational corporations often pay a larger percentage of duties than local players because of duty collection inefficiencies.) As a part of its discussion with governments, Diageo has also suggested tax structures that would encourage the use of local raw materials or reduce the presence of illicit alcohol, both of which have longer-term benefits for the company’s brand intangible asset (less black market competition) and cost advantages (garnering greater economies of scale through fair tax collection practices).

Another consideration from an industry structure perspective in Africa is the sizable potential that exists outside of the formal economy in the region. In many African regions, the informal economy is significant, ranging from 20% to more than 50% of personal consumption expenditures, according to estimates from a number of consumer companies operating in the region. While currently a competitive threat in many regions, this dynamic also offers a tremendous longer-term opportunity as consumers rotate out of the informal economy and gravitate toward formal consumer staples categories.

The Risks

While the African marketplace has become a safer investment for many companies, there are still inherent risks. Foremost is that emerging markets exports still depend largely on the fortunes of developed economies, which are facing widespread deleveraging by governments, corporations, and consumers; increasing saving rates; and unemployment rates above historical norms.

Additionally, with dependence on natural resource commodity prices, African markets are often subject to economic shocks, which can have a meaningful impact on the local currencies and in turn impair the competitiveness of local corporations. Inflation appears to have stabilized in a number of emerging markets over the past several years, though input costs for many consumer-facing companies remain well above historical norms, thereby constraining margin expansion opportunities over the foreseeable future.

Finally, we have concerns that the arrival of large, multinational companies in emerging markets (the controlling stake of Wal-Mart (WMT) in South African retailer Massmart, for example) have the potential to change the economics for all market participants (though potentially making it easier for global consumer staples companies to reach a wider audience).

Companies With Moats

Although we’ve discussed the different growth levers of Africa as a continent up to this point, the reality is that Africa is diverse spanning 54 countries and a wide variety of appetites for consumer product categories. When dealing with a wide range of geographies, evolving consumer preferences, and broad product categories, scale makes a meaningful difference in many functions, including sourcing, logistics, marketing, bargaining power over retail customers (particularly among highly fragmented retail markets like many Africa nations) and overhead/ back offices. Globally recognized brands make it easier to enter new markets, and can create cross-selling opportunities with local brands and across product categories.

The companies below, each of which has a stable economic moat, are best positioned to cater to African consumers.

Diageo (DEO)

Diageo has a strong portfolio of brands that are available in 40 countries across the continent (which represent 80% to 85% of the alcohol consumption in the region). Collectively, Africa represented 13% of Diageo’s sales in 2013. Beer is the dominant category for Diageo in Africa, representing approximately 60% of Diageo’s sales in the region, though the company expects to shift to spirits in the years to come on the back of favorable wealth creation and premiumization opportunities. Diageo has strong footholds in Nigeria and South Africa and has targeted other regions such as Ethiopia, Kenya, Angola, Uganda, Tanzania, and Mozambique.

McDonald’s (MCD)

McDonald’s remains the dominant player in the global fast-food restaurant space (accounting for about 12% of U.S. fast-food sales, 8% of the global informal eating-out marketplace, and about 4% of global restaurant sales); however, the firm operates a small base of restaurants in Africa. We think the young local consumer base combined with a growing middle class will create extensive opportunities for restaurant operators like McDonald’s. Management recently called out Nigeria as a particular area of focus for further expansion and established a licensee market in a number of African countries since the beginning of 2014, including South Africa, where the firm operates nearly 200 restaurants. As such, we expect expansion into Africa will be a driver of McDonald’s growth going forward.

Nestle (NSRGY)

More than 100 years ago, Nestle established its position in Egypt, and more than 50 years ago, it set up shop in Central and West Africa (a region that now boasts more than $1 billion in annual sales), signifying the innate understanding Nestle possesses of local consumers and local routes to market. With its portfolio of popularly positioned products (lower-priced products that still offer the same level of nutrition), Nestle caters to a consumer base with limited spending power. Given the firm’s vast resources, we anticipate continued investments behind product innovation and marketing support should increase its position in this up-and-coming region.

SABMiller (SAB)

SABMiller benefits from a first-mover advantage in many parts of Africa (establishing its operations in South Africa back in 1895), where it possesses monopolistic control over the beer and soft drinks bottling markets in geographies such as Botswana, Mozambique, Swaziland, Zambia, and South Africa. An entrenched position in several African markets creates a cost advantage that allows the firm to offer products at low price points that cannot be economically replicated by multinational new entrants. The strength of the firm’s brand intangible assets in the region is evident in its balanced growth between volumes and pricing, which is particularly notable in light of the challenging economic backdrop. We forecast low-double-digit growth in Africa throughout most of our five-year forecast period, but regard a mid- to high-single-digit rate as a more realistic long-term assumption.

Unilever (UL)

Unilever has called out Africa as being the next big growth market. (The company is already operating as one of the largest consumer goods firms in South Africa.) But given a lack of infrastructure across the continent, we anticipate Unilever’s penetration throughout the region will be at a measured pace. However, we can’t ignore the adeptness Unilever has shown in tailoring its products to consumers around the world, and as such, we ultimately anticipate that the firm’s brands and broad portfolio, which spans food and beverages as well as home care and personal care offerings, will win with consumers across the continent as well.

Yum Brands (YUM)

Despite its vast presence in other emerging regions, such as China, Yum remains fairly underpenetrated in Africa, with just 7% of KFC’s system sales resulting from the continent. Despite more than 1,000 KFC stores across Africa (including nearly 700 in South Africa), the firm’s operations are fairly concentrated, competing in just 16 countries (which is up from just 10 in 2010). As such, we still believe that KFC possesses significant space for expansion. However, management seems to recognize the challenges posed by the varying (and in some instances volatile) political and economic environments throughout the region and subsequently plans to pursue its rollout at a measured pace, which we view favorably. We ultimately expect African markets will become vital drivers of long-term free cash flow.

Long-Term Story

The appeal of markets such as Africa to consumer staples companies is understandable. Populations are expected to grow exponentially, urbanization and private investment are likely to create favorable disposable income tailwinds, and a base of younger consumers with a lifetime of transactions lie ahead. Nevertheless, with growth potential come investment needs, and in the case of Africa and other frontier and emerging markets, there are significant infrastructure requirements necessary to stimulate economic growth, indicating that consumer companies shouldn’t expect to monetize their emerging-market exposure overnight.

We think that those companies with economic moats–more specifically, those companies with brand portfolios across multiple pricing tiers and expansive distribution networks–are the best positioned to monetize Africa’s tremendous growth.

5 Comments on "A Continent of New Consumers"

Dredd on Sat, 20th Dec 2014 8:31 am

Let’s face it, Africa is a new place to plunder (Journalism: Facts vs. Fantasy).

The “we are there militarily to serve customers” ruse does not pass the smell test.

Plantagenet on Sat, 20th Dec 2014 8:34 am

One year ago today I was in Tanzania climbing Killimanjaro Urbanization and the creation of a middle class of consumers is occurring very rapidly in Africa— there are still traditional villages in tribal areas off the grid but these areas are shrinking rapidly

Perk Earl on Sat, 20th Dec 2014 11:54 pm

Plant, since you’ve been to Africa maybe you have a handle on this question. Will the wild animals be eliminated for food and to make room for expansion?

bobinget on Sun, 21st Dec 2014 7:06 am

Caliphate AFRICA:

Boko Haram is growing faster then IS

MAIDUGURI, Nigeria — Thousands of members of Nigeria’s home-grown Islamic extremist Boko Haram group strike across the border in Cameroon, with co-ordinated attacks on border towns, a troop convoy and a major barracks.

Farther north, Boko Haram employs recruits from Chad to enforce its control in northeastern Nigerian towns and cities.

In Niger, the government has declared a “humanitarian crisis” and appealed for international aid to help tens of thousands of Nigerian refugees driven from their homes by the insurgency.

RELATED STORIES

Boko Haram executing elderly in northeast Nigeria

These recent events show how neighbouring countries are increasingly being drawn into Nigeria’s Islamic uprising. Thousands of people have been killed in Nigeria’s 5-year insurgency and some 1.6 million people driven from their homes.

“We are concerned about the increasing regionalization of Boko Haram,” said Comfort Ero, Africa director for the International Crisis Group. The countries have been slow to recognize “the gravity and extent of the threat from Boko Haram.”

Ero cautioned that co-operation between the neighbouring countries is weak. “None of the sides is willing to share information with the other,” Ero said. “There’s always been a lack of confidence in terms of shared regional security.”

She said there is also distrust of the capabilities of Nigeria’s once-proud military, which has been battered by Boko Haram. A court-martial this week sentenced 54 soldiers to death by firing squad for refusing to fight the extremists.

Chad responded this week by opening a regional “counter-terrorism cell” against Boko Haram in N’Djamena, Chad’s capital 40 miles (60 kilometres) from the Nigerian border, according to an adviser to French Defence Minister Jean-Yves Le Drian.

Boko Haram’s threat to neighbouring countries was highlighted on Wednesday, when some 5,000 insurgents launched simultaneous attacks on border towns in Cameroon, that country’s Ministry of Defence said. During the fighting, the militants set off a roadside improvised explosive device that hit a military convoy. They also attacked the main border barracks at Amchide town, the defence statement said.

Cameroonian troops repelled the attacks and killed 116 militants, while losing a sergeant and a lieutenant, it said, adding that Boko Haram must have suffered additional casualties on the Nigerian side caused by Cameroonian artillery fire.

Fighters from Chad, Niger and Cameroon long have been identified among Boko Haram fighters in Nigeria. But residents fleeing Boko Haram now report that Chadian recruits are enforcing Boko Haram’s rule in northeast Nigerian border towns in Borno state. People who escaped from Gajigana village, which was attacked a week ago, said fighters they called “Chadian mercenaries” have taken charge of most communities, even sitting in courts to adjudicate local disputes.

“They monitor every movement, all the things we do, the kind of people you meet with,” said Kalli Abdullahi, who escaped to Maiduguri this week and spoke to The Associated Press. If residents break the strict Shariah law “they will get you and kill you so as to instil fear in people,” he said.

Nigerian government officials confirm that Boko Haram controls 12 of 27 local government areas in Borno state, as well as some in Adamawa and Yobe states. And they long have had camps in Chad, Cameroon and Niger, say experts.

The area where the four countries’ borders meet is generally poor and long has been ignored by governments. Desertification has intensified tensions. High unemployment means there are groups of disgruntled youths who are an easy target for Boko Haram recruitment. Across borders, people often belong to the same tribe and speak the same local languages. Boko Haram offers signing bonuses and monthly pay to those who join, say residents.

Boko Haram leader Abubakar Shekau long has expressed his international ambitions, saying his group is fighting to make “the entire world” an Islamic state.

SEE:

Analyst Ely Karmon wrote in a paper for the Terrorism Research Initiative that Boko Haram is “an immediate and infectious regional threat.”

Read more: http://www.ctvnews.ca/world/boko-haram-extremists-striking-across-nigerian-border-1.2157476#ixzz3MXLwYdOA

Apneaman on Sun, 21st Dec 2014 12:12 pm

Signing bonuses. Sounds very corporate. These types of alternative groups eventually attract many malcontents when the dominate society has nothing to offer except poverty and oppression. They are as old as humanity itself. Religions and ideologies are just tribes.

It’s part of an ancient behavioral loop.

Step 1. Individuals and groups evolved to maximize fitness by maximizing power, which requires over-reproduction and/or over-consumption of natural resources (overshoot), whenever systemic constraints allow it. Differential power generation and accumulation result in a hierarchical group structure.

Step 2. Energy is always limited, so overshoot eventually leads to decreasing power available to the group, with lower-ranking members suffering first.

Step 3. Diminishing power availability creates divisive subgroups within the original group. Low-rank members will form subgroups and coalitions to demand a greater share of power from higher-ranking individuals, who will resist by forming their own coalitions to maintain power.

Step 4. Violent social strife eventually occurs among subgroups who demand a greater share of the remaining power.

Step 5. The weakest subgroups (high or low rank) are either forced to disperse to a new territory, are killed, enslaved, or imprisoned.

Step 6. Go back to step 1.

http://www.dieoff.org/