On Monday, September 29, the Wall Street Journal (WSJ) published a story called “Why Peak Oil Predictions Haven’t Come True.” The story is written as if there are only two possible outcomes:

- The Peak Oil version of what to expect from oil limits is correct, or

- Diminishing Returns can and are being put off by technological progress–the view of the WSJ.

It seems to me, though, that a third outcome is not only possible, but is what is actually happening.

3. Diminishing returns from oil limits are already beginning to hit, but the impacts and the expected shape of the down slope are quite different from those forecast by most Peak Oilers.

Area of Confusion

In many people’s way of thinking, the economy is separate from resources and the extraction of those resources. If we believe economists, the economy can grow indefinitely, with or without the use of resources. Clearly, with this view, the price of these resources doesn’t matter very much. If one kind of resource becomes more expensive, we can substitute other resources, once the scarce resource becomes sufficiently high-priced that the alternative makes financial sense. Incomes can rise arbitrarily high–all it takes is for each of us to pay the other higher wages. And we can fix any problem with the financial system with more money printing and more debt.

This wrong version of how our economy works has been handed down through the academic world, through our system of peer review, with each academic researcher following in the tracks of previous academic researchers. As long as new researchers follow the same wrong thinking as previous researchers, their articles will be published. Economists were especially involved in putting together this wrong world-view, but politicians helped as well. They liked the outcomes of the models the economists produced, since it made it look like the politicians, with the help of economists, were all-powerful. All the politicians needed to do was tweak the financial system, and the world economy would grow forever. There was not even a need for resources!

Peak Oilers’ Involvement

The Peak Oilers walked into a situation with this wrong world view, and started trying to fix pieces of it. One piece that was clearly wrong as the relationship between resources and the economy. Resources, especially energy resources, are needed to make any of the goods and services we buy. If those resources started reaching diminishing returns, it would be harder for the economy to grow. The economy might even shrink. Dr. Charles Hall, recently retired professor from SUNY-ESF, came up with one measure of diminishing returns–falling Energy Returned on Energy Invested (EROEI).

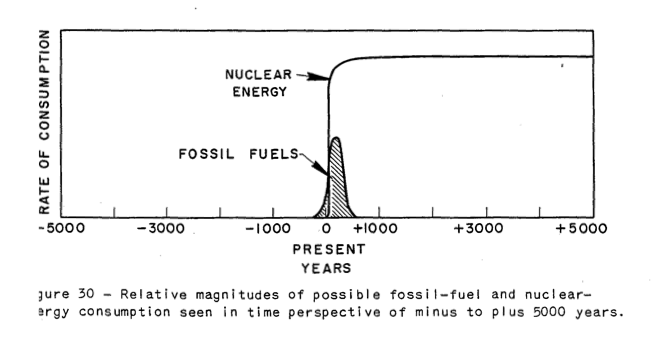

How would shrinkage occur? For this, Peak Oilers turned to the work of M. King Hubbert, who worked in an area of geology. He wrote about how supply of a resource might be expected to decline with diminishing returns.

Hubbert was not concerned about what effect diminishing returns would have on the economy–presumably because that was not his area of specialization. He avoided the issue by only modeling the special case where no economic impact could be expected–the special case where a perfect substitute could be found and be put in place, in advance of the decline caused by diminishing returns.

In the example shown above, Hubbert assumes cheap nuclear would take over, before the decline in fossil fuels started. Hubbert even talked about making cheap liquid fuels using the very abundant nuclear resources, so that the system could continue as before.

In this special case, Hubbert suggested that the decline in resources might follow a symmetric curve, slowly declining in a pattern similar to its original rise in consumption, since this is the pattern that often occurs in extracting a resource in nature. Many Peak Oilers seem to believe that this pattern will happen in the more general case, where no perfect substitute is available, as well. A perfect substitute would need to be cheap, abundant, and involve essentially no cost of transition.

In the special case Hubbert modeled, Hubbert indicated that production would start to decline when approximately 50% of reserves had been exhausted. Peak Oilers often used this approach or variations on it (so called “Hubbert Linearization“), to forecast future production, and to determine dates when oil production would “peak.” Of course, as technology improved, additional oil became accessible, raising reserves. Also, as prices rose, resources that had never been economically extractible became extractible. Production continued beyond forecast peak dates, again and again.

Peak Oilers got at least part of the story right–the fact that we are in fact reaching diminishing returns with respect to oil. For this they should be commended. What they didn’t figure out is, however, is (1) how the energy-economy system really works, and (2) which pieces of the system can be expected to break first. This issue is not really the Peak Oilers fault–it is the result of starting with a very bad model of the economy and not understanding which pieces of that model needed to be fixed.

How the Economic System Really Works

We are dealing with a networked economy, one that is self-organized over time. I would represent it as a hollow network, built up of businesses, consumers, and governments.

This economic system uses energy of various kinds plus resources of many kinds to make goods and services. There are many parts to the system, including laws, taxes, and international trade. The system gradually changes and expands, with new laws replacing old ones, new customers replacing old ones, and new products replacing old ones. Growth in the number of consumers tends to lead to a need for more goods and services of all kinds.

An important part of the economy is the financial system. It connects one part of the system with another and almost magically signals when shortages are occurring, so that more of a missing product can be made, or substitutes can be developed.

Debt is part of the system as well. With increasing debt, it is possible to make use of profits that will be earned in the future, or income that will be earned in the future, to fund current investments (such as factories) and current purchases (such as cars, homes, and advanced education). This approach works fine if an economy is growing sufficiently. The additional demand created through the use of debt tends to raise the prices of commodities like oil, metals, and water, giving an economic incentive for companies to extract these items and use them in products they make.

The economy really can’t shrink to any significant extent, for several reasons:

- With rising population, there is a need for more goods and services. There is also a need for more jobs. A growing networked economy provides increasing numbers of both jobs and goods and services. A shrinking economy leads to lay-offs and fewer goods and services produced. It looks like recession.

- The networked economy automatically deletes obsolete products and re-optimizes to produce the goods needed now. For example, buggy whip manufacturers are pretty rare today. Thus, we can’t quickly go back to using horse and buggy, even if should we want to, if oil becomes scarce. There aren’t enough horses and buggies, and there aren’t enough services for cleaning up horse manure.

- The use of debt for financing depends on ever-rising future output. If the economy does shrink, or even stops growing as quickly as in the past, there tends to be a problem with debt defaults.

- If debt does start shrinking, prices of commodities like oil, gold, and even food tend to drop (similar to the situation we are seeing now). These lower prices discourage investment in creating these commodities. Ultimately, they lead to lower production and job layoffs. If deflation occurs, debt can become very difficult to repay.

Under what conditions can the economy grow? Clearly adding more people to the economy adds to growth. This can be done by through adding more babies who live to maturity. It can also be done by globalization–adding groups of people who had previously only made goods and services for each other in limited quantity. As these groups get connected to the wider economy, their older, simpler ways of doing things tend to be replaced by more productive activities (involving more technology and more use of energy) and greater international trade. Of course, at some point, the number of new people who can be connected to the global economy gets to be pretty small. Growth in the world economy lessens, simply because of lessened ability to add “underdeveloped” countries to the networked economy.

Besides adding more people, it is also possible to make individual citizens “better off” by making workers more efficient at producing goods and services. Most people think of greater productivity as happening through technological changes, but to me, it really represents a combination of technological changes, plus a combination of inexpensive resources of various kinds. This combination often includes low-cost fossil fuels; abundant, cheap water supply; fertile soil; and easy to extract metal ores. Having these available makes possible the development of new tools (like new agricultural equipment, sewing machines, and vehicles), so that workers can become more productive.

Diminishing returns are what tend to “mess up” this per capita growth. With diminishing returns, fossil fuels become more expensive to extract. Water often needs to be obtained by desalination, or by much deeper wells. Soil needs more amendments, to be as fertile as in the past. Metal ores contain less and less ore, so more extraneous material needs to be extracted with the metal, and separated out. If population grows as well, there is a need for more agricultural output per acre, leading to a need for more technologically advanced techniques. Working around diminishing returns tends to make many kinds of goods and services more expensive, relative to wages.

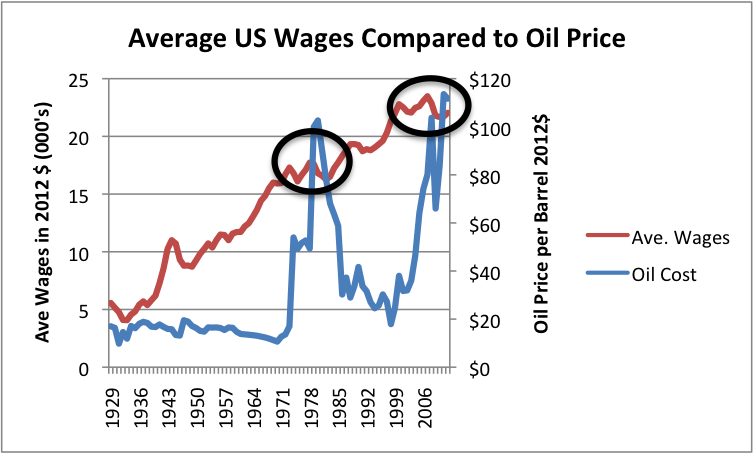

Rising commodity prices would not be a problem, if wages would rise at the same time as the price of goods and services. The problem, though, is that in some sense diminishing returns makes workers less efficient. This happens because of the need to work around problems (such as digging deeper wells and removing more extraneous material from ores). For many years, technological changes may offset the effects of diminishing returns, but at some point, technological gains can no longer keep up. When this happens, instead of wages rising, they tend to stagnate, or even decline. Figure 3 shows that per capita wages have tended to grow in the United States when oil was below about $40 or $50 barrel, but have tended to stagnate when prices are above that level.

What Effects Should We Be Expecting from Diminishing Returns With Respect to Oil Supply?

There are several expected effects of diminishing returns:

- Rising cost of extraction for oil and for other commodities subject to diminishing returns.

- Stagnating or falling wages of all except the most elite workers.

- Ultra low interest rates to try to make goods more affordable for workers stressed by stagnating wages and high prices.

- Rising governmental debt, in an attempt to stimulate the economy and in order to provide programs for the many workers without good-paying jobs.

- Increasing concern about debt defaults, as the amount of debt outstanding becomes increasingly absurd relative to wages of workers, and as all of the stimulus debt runs its course, in countries such as China.

- A two way problem with the price of oil. On one side is recession, when oil prices rise to unaffordable levels. Economist James Hamilton has shown that 10 out of 11 post-World War II recession were associated with oil price spikes. He has also shown that there is good reason to expect that the Great Recession was related to the run-up in oil prices prior to 2007. I have written a related paper–Oil Supply Limits and the Continuing Financial Crisis.

- The second problem with the price of oil is the reverse–price of oil too low relative to the cost of extraction, because wages are not high enough to permit workers to afford the full cost of goods made with high-priced oil. This is really a problem with inadequate affordability (called inadequate demand by economists).

- Eventual collapse of whole system.

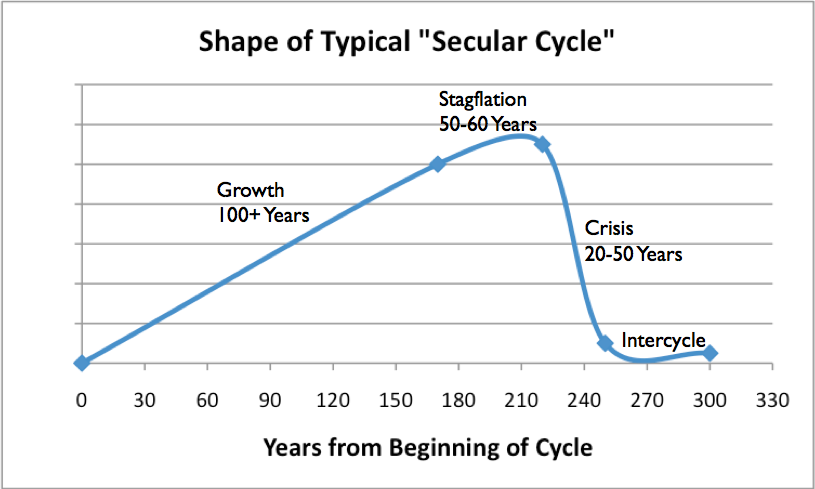

There have been many studies of collapses of past economies. These collapses tended to occur when the economies hit diminishing returns after a long period of growth. The problems were often similar to ones we are seeing today: stagnating wages of common workers and growing debt. There were more and more demands on governments to fix the problems of workers, but governments found it increasingly difficult to collect enough taxes for all the needed programs.

Eventually, the economic systems have tended to collapse, over a period of years. The shape of resource use in collapses was definitely not symmetric. Figure 4 shows my view of the typical shape of the collapses in non-fossil fuel economies, based on the work of Peter Turchin and Surgey Nefedof.

In my view, the date of the drop in oil supply will be determined by what appear to on-lookers to be financial problems. One possible cause is that the oil price will be too low for producers (a condition that is occurring now). Governments will find it unpopular to raise oil prices, but at the same time, will be powerless to stop the adverse impacts the fall in price has on world oil supply.

Falling oil prices have especially adverse effects on oil exporters, because they depend on revenues from oil to fund their programs. We are already seeing this now, with the increased warfare in the Middle East, Russia’s increased belligerence, and the problems of Venezuela. These issues will tend to reduce globalization, leading to less world growth, and a greater tendency for the world economy to shrink.

Unfortunately, there are no obvious ways of fixing our problems. High-priced substitutes for oil (that is, substitutes costing more than $40 or $50 barrel) are likely to have as adverse an impact on the economy as high-priced oil. The idea that energy prices can rise and the economy can adapt to them is based on wishful thinking.

Our networked economy cannot shrink; it tends to break instead. Even well-intentioned attempts to reduce oil usage are likely to backfire because they tend to reduce oil prices and have other unintended effects. Furthermore, a use of oil that one person would consider frivolous (such as a vacation in Greece) represents a needed job to another person.

Should Peak Oilers Be Blamed for Missing the “Real” Oil Limits Story?

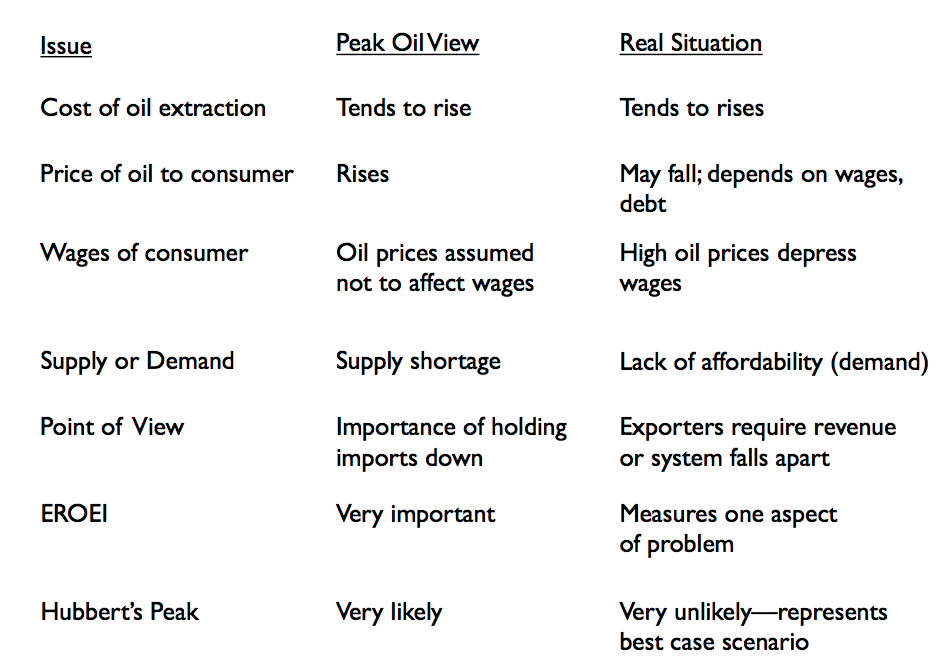

No! Peak oilers have made an important contribution, in calling the general problem of diminishing returns in oil supply to our attention. One of their big difficulties was that they started out working with a story of the economy that was very distorted. They understood how to fix parts of the story, but fixing the whole story was beyond their ability. The following chart shows a summary of some ways their views and my views differ:

One of the areas that Peak Oilers tended to miss was the fact that an oil substitute needs to be a perfect substitute–that is, be available in huge quantity, cheaply, without major substitution costs–in order not to adversely affect the economy and in order to permit the slow decline rate suggested by Hubbert’s models. Otherwise, the problems with diminishing returns remain, leading to declining wages and rising costs of making goods and services.

One temptation for Peak Oilers has been to jump on the academic bandwagon, looking for substitutes for oil. As long as Peak Oilers don’t make too many demands on substitutes–only EROEI comparisons–wind and solar PV look like they have promise. But once a person realizes that our true need is to keep a networked economy growing, it becomes clear that such “solutions” are woefully inadequate. We need a way of overcoming diminishing returns to keep the whole system operating. In other words, we need a way to make wages rise and the price of finished goods fall relative to wages; there is no chance that wind and solar PV are going to do this for us. We have a much more basic problem than “new renewables” can solve. If we can’t figure out a solution, our economy is likely to reach what looks like financial collapse in the near term. Of course, the real reason is diminishing returns from oil, and from other resources as well.

westexas on Tue, 7th Oct 2014 1:31 pm

2013 was down to 42.7 mpbd:

http://i1095.photobucket.com/albums/i475/westexas/Slide1_zps3161a25b.jpg

marmico on Tue, 7th Oct 2014 1:48 pm

Wrong chart. That’s your 2002-2005 “gap”.

Produce the GNE chart since 2005.

Erik Townsend on Tue, 7th Oct 2014 2:05 pm

Excellent piece, Gail! 🙂

As I have long argued, the only thing the “Peak Oilers” got wrong was that they focused on the wrong issue. Peak Oil, when defined as the moment when the world reaches its maximum rate of oil production never to again be exceeded, is a topic of great academic interest, but has only limited indirect impacts on society and the economy.

The far more interesting topic is Peak Cheap Oil, which I define to describe the major inflection points in the ongoing increase in the real cost of energy over time. Conventional crude oil production (which I define as oil that can be produced for 10,000′ depth) has never even been explored for oil! Without a doubt, technology will continue to advance and we’ll always be able to find and produce more oil for some price. The key question is how far need that price rise before the cost of energy breaks the back of the global economy?

This comes in stages, or “waves”. In the 1950s, nobody cared about the cost of energy. Fuel efficiency wasn’t even measured, and the last thing an automobile purchaser thought about was how much the fuel would cost to run his new toy.

After the 1970s shock, we started caring more about the cost of energy, and fuel economy became a significant consideration in the purchase of any automobile, power yacht, or other high-consuming device. But frankly, we could still easily afford energy. The percentage of middle class earnings consumed by energy purchases was still low enough that although people liked to gripe about the price of gas, the bottom line was they could still afford it and energy cost didn’t markedly damage the economy or fundamentally change the way of life of most people.

Since 1999, we’ve been adjusting to a new (irreversible, one-way) increase in the cost of energy in real terms. We’re never going back to $20/bbl oil *because the incremental cost of production is much higher now that fracking and other technologies must be employed to meet energy demands*.

Some have argued that the present economic weakness (slow recovery from the 2008 financial crisis) has persisted specifically because the cost of energy is impeding the ability of the economy to recover. I think that’s an interesting argument, but hardly one I see hard evidence to make conclusively.

I contend, however, that the *next* wave is the one that’s going to swamp the global economy. At some point the U.S. tight oil plays will run out of steam, and we’ll realize that the “shale revolution” taking us to 12.5mm bpd by 2020 of domestic U.S. production is not actually a permanent endowment that will last centuries, but rather a flash in the pan that will last a few years, then peter out due to profoundly steep decline rates associated with tight oil plays.

Of course there will be more technological innovation, and more oil will be discovered and produced. But at what cost? I contend that there is some price level above which the global economy will be stuck in permanent depression until such time as a much cheaper energy alternative is adopted. It’s impossible to model such an outcome with complete accuracy, but my gut feeling says that if the floor on oil prices due to incremental cost of production moved up from $85ish presently to $150 (in today’s dollars), we’d be screwed. The cost of energy will have reached a level where it consumes too great a percentage of global GDP, and the economy won’t be able to grow organically until a cheaper alternative is first discovered and then implemented, which could take decades if we have to replace liquid fuels in transportation.

In summary, when we reach peak global oil production was never the important question to ask. The important question is and always has been, At what point does the cost of oil production become prohibitive, such that the economy simply cannot function the way it used to? I’m pretty sure the correct answer is “soon”, but when you consider that the age of oil has already lasted 150 years, “soon” is a concept that has an inherent +/- several years error factor.

Erik Townsend on Tue, 7th Oct 2014 2:11 pm

Website weirdness… The comment “can be produced for 10,000′ depth” obviously makes no sense. Here’s the original wording, before the web gods ate my homework! 🙂

… Conventional crude oil production (which I define as oil that can be produced for $40/bbl or less) most assuredly peaked in 2005. But on the other hand, fully 1/2 of the planet’s surface (below oceans deeper than 10,000′) has never even been explored for oil!…

marmico on Tue, 7th Oct 2014 2:13 pm

Ooops, I screwed up. So global GNE declined from 43.7 to 42.7, 2013 over 2012 because U.S. LTO production increased from 7 to 8. Got it.

As indicated upthread with my WAG, GNE is 42 mb/d plus 8% on the upside and 1% on the downside. I overestimated GNE in the last 10 years. 🙂

You underestimated it materially.

Northwest Resident on Tue, 7th Oct 2014 2:36 pm

Erik asks: “The important question is and always has been, At what point does the cost of oil production become prohibitive, such that the economy simply cannot function the way it used to?”

Erik, you can be one hundred percent certain that the break point for too-expensive oil has already been reached, and some time ago.

The economy today is most definitely not functioning “the way it used to”. We always had debt — that was BAU — but the debt was paid off by profits skimmed from a growing economy and rising consumption of natural resources.

Now our debt is many trillion$, and it will never be paid off. What the governments of the world have been hiding but will not be able to hide for much longer is that the global economy is shrinking, not growing. The stock market values are highly manipulated and grossly inflated. The only thing keeping the undead economy lurching forward is continued massive injections of debt combined with ZIRP. In summary, we left the “normal” economy a long time ago and it has already faded out of sight in the rear view mirror.

Your points are all valid and right on. Except, there is no need to ask at what price for oil the economy will cease to function normally — we’ve already hit that price and it has devastated the economies of the world. The global economy and most national economies are mortally wounded, bleeding out, stumbling forward bravely, but they’ll all bite the dust sooner rather than later.

marmico on Tue, 7th Oct 2014 2:37 pm

I think some people come here to prove how “smart” they are

You are the smartest dude on the intertubz I have ever met. Congrats.

Do you have a problem that I can single handily take on your heroes–shortonoil, westexas, Rockman.

Listen, I give kudos to Jeffrey Brown even though I disagree. Shortonoil is a quart shy and Rockman reeks of hubris.

Erik Townsend on Tue, 7th Oct 2014 2:43 pm

@Northwest Resident

We’re not as far apart in opinion as you think.

Personally, yes, I am convinced that cost of energy is impeding economic recovery, and I also consider the possibility that cost of energy was the catalyst that caused the 2008 financial crisis. Clearly, excessive and undercollateralized debt was the primary driver, but the housing bubble had been raging for several years against the fundamentals. It all came crashing down just after the June 2008 peak in WTI crude oil prices, and I think cost of energy was likely the catalyst to bring the reckless borrowing bubble to an end.

But my point is, neither of us can CONCLUSIVELY argue the point that energy cost is a primary driver of the present economic malaise. My INTUITION says you’re right in most of what you say, but I respectfully observe that we don’t have sufficient evidence to make the case persuasively as a statement of fact.

Northwest Resident on Tue, 7th Oct 2014 2:44 pm

marmico — I’m just a casual observer. My impression of you is that you’re a class A asshole. I don’t see that you are “single handedly” taking on anybody — I see an ego-driven piss ant desperately trying to get attention and prove that he’s smart. We’ve already been over this before. You like to throw out big words to impress people, but you don’t even know what those words mean. You are most assuredly, absolutely demonstrably a total egomaniac and an asshole. But hey, that’s just one dummy’s opinion. Go ahead, use a few big words, just us what a BIG man you are (asshole).

BTW, disagreeing with anybody is fine, happens all the time. But to do it in such a disrespectful, in-your-face and obnoxious manner — that’s your specialty. In any case, supposing you’re one hundred percent correct about all the nitpicky minor points that you’re making, you still clearly demonstrate that you can’t see the forest through the trees — you are totally oblivious to the bigger issues, so you focus on the minor nitpicky details. Hey man, I pity folks like you, I know how hard it must be to be you.

Northwest Resident on Tue, 7th Oct 2014 2:48 pm

Erik — Right on. We agree on everything. One point however is that even though I don’t claim to be expert or educated enough to make this determination, I have read several or more informative articles by people who I think probably are experts on the subject, who argue that the price of oil is exactly what is behind the astronomical debt — compensating for the too-high cost of oil. I just take that “fact” for granted, but you are correct, I don’t know it for a fact — I just think it and believe it.

GregT on Tue, 7th Oct 2014 2:50 pm

Marmico,

In your mind only, have you ‘taken on’ Short, West, or the Rock. Your focus is narrow, and in no way presents even a tiny fraction of the big picture.

Playing the fiddle, while Rome burns. I can’t think of a more appropriate analogy.

Davy on Tue, 7th Oct 2014 3:06 pm

Thanks NR for the opine on Marm. He is a cocky ass corn. He has slapped me upside the head a time or two. When Marm slaps me it tickles when short or Rock slap me it hurts.

marmico on Tue, 7th Oct 2014 3:19 pm

Apologies, repetitive GregT…

Rockman and the Quart Shy of Oil won’t come near me on this website when they are challenged.

Westexas doesn’t have a problem going head to head.

Why is that?

GregT on Tue, 7th Oct 2014 3:33 pm

“Why is that?”

Has it ever occurred to you, that you are only wasting people’s time? There is no point in flogging a dead horse.

marmico on Tue, 7th Oct 2014 3:38 pm

Oh, Davy-boy, you are such a cutie. Is it raining in the Ozarks?

Go out in the back forty, slice a piece of BAU sod, carry it back on your broad bifurcated shoulders, slap it on the compressed roof to protect against the descent leak.

Did I get enough doomer stuff in the word salad. 🙂

Northwest Resident on Tue, 7th Oct 2014 3:54 pm

Davy — My sister used to live next door to a very poor, ugly, grossly overweight woman who had a kid that was the biggest brat I’ve ever seen. The kid was constantly running around making noise, doing crazy-stupid things to get attention, breaking things, crying when he didn’t get his way, being a loud obnoxious brat. He always had a snot-filled nose, a dirty face and grubby stinking clothes. I’m sure that brat (or one like him) grew up to become marmico. Personalities like marmico’s don’t just happen — they are molded and formed by the intense unhappiness of being a kid like that brat I just described. That’s why I pity people like marmico — but they’re still assholes… 🙂

marmico on Tue, 7th Oct 2014 4:09 pm

That’s why I pity people like marmico — but they’re still assholes… 🙂

I bow down to your compassion. Your preacher daddy taught you so at the same time he bought your pampers with the proceeds from the church service basket.

You are a real winner, NWR.

Northwest Resident on Tue, 7th Oct 2014 4:29 pm

hey marmico — Sorry I hurt your feelings. I can understand why you’d feel the need to lash out. Stay your obnoxious self, don’t change a thing.

marmico on Tue, 7th Oct 2014 4:38 pm

My feelings are not hurt.

Stick with seeds since you know squat about energy.

Davy on Tue, 7th Oct 2014 4:58 pm

Marm, at the cardinals game now. I am so glad you did not leave me out of your banter. That would have hurt. Stick around the doom grows on you.

Northwest Resident on Tue, 7th Oct 2014 5:11 pm

Erik — If you’re still paying attention to posts on this article after that little mud fight…

I tried to find one or two of the articles that I read in the past that made me a firm believer in the premise that too-high “energy cost is a primary driver of the present economic malaise” as you so eloquently put it.

I don’t think I have run across any in-depth statistic laden studies that conclusively prove it, but I think this might be one of those cases where common sense goes a long way toward proving the point.

From the Christian Science Monitor:

“The growth in government debt occurs because of a mismatch between income and expenditures. There is a cutback in government revenue because high oil prices make some goods using oil unaffordable, causing a cutback in production, and hence employment. The government is affected because unemployed workers don’t pay much in taxes. Government expenditures are still high because many unemployed workers are still collecting benefits.”

And…

“The real issue is increasingly high oil prices, which adversely affect both government finances and wages.”

Of course, Gail at Our Finite World has a lot to say on the subject in her post titled “Ten Reasons Why High Oil Prices are a Problem”:

1. It is not just oil prices that rise. (rising oil prices result in corresponding price increases in food, transportation, product manufacturing, mining — everything.

3. Salaries don’t increase to offset rising oil prices. Less wages equates to less taxes collected, equates to less extra money to spend on discretionary consumption, which leads to business slowdown, closure, etc…

4. Higher oil prices reflect a need to focus a disproportionate share of investment and resource use inside the oil sector. This makes it increasingly difficult to maintain growth within the oil sector, and acts to reduce growth rates outside the oil sector.

These two and other articles seem to make a very straight-forward, logical and common sense argument that too high oil prices are directly responsible for our economic malaise, or as I would put it, our coming economic doom.

Agree? Disagree?

marmico on Tue, 7th Oct 2014 5:17 pm

Thanks for your kind words, Davy.

Nothing like attendance at a home game where a win advances. Good luck Cards!

As a kid, Mantle was fav, Musial was twilight.

Sheesh, if baseball was the deal I wouldn’t have tricked out westexas with the NFL rules, I should have done MLB.

GregT on Tue, 7th Oct 2014 5:24 pm

Anyone else smell a dirty sock, puppet?

eriktownsend on Tue, 7th Oct 2014 6:11 pm

@NWR

I think we’re still on the same page we left off from with your last post. Yes, I am personally persuaded by these arguments. But no, I don’t feel able to “prove” anything in the sense of arguing that sufficient data are in evidence to conclude that oil prices are the cause of the economic problems we face.

We now return to the sophomoric discussion of marmico’s anal orifice dimensions already in progress… 😉

J-Gav on Tue, 7th Oct 2014 6:14 pm

NR- re: a few comments back – You might be the one to give that speech you were talking about! Sounds to me like you’ve got it together pretty well, so why not?

Okay – I give my own little speeches without great results – but after the next big financial hit, people might start to listen, you never know …

Northwest Resident on Tue, 7th Oct 2014 9:29 pm

erik, J-Gav:

I haven’t seen any scientific studies that prove too-high oil problems are the cause of our economic problems either. But we agree, it seems pretty obvious that is the case.

J-Gav — I’ve given a lot of speeches in my time, mostly back in college, and I’m always ready to give another one. But after the next big financial hit I’d be preaching to the choir!