The one chart about oil's future everyone should see

$this->bbcode_second_pass_quote('', 'W')hen people read about a long-term forecast of world oil supply--say, out to 2030--they often believe that the forecasters are merely incorporating our knowledge of existing fields and figuring out how much oil can be extracted from them over the forecast period. Nothing could be further from the truth. Much of the forecast supply has not yet been discovered or has no demonstrated technology which can extract or produce it economically. In other words, such forecasts are merely guesses based on the slimmest of evidence.

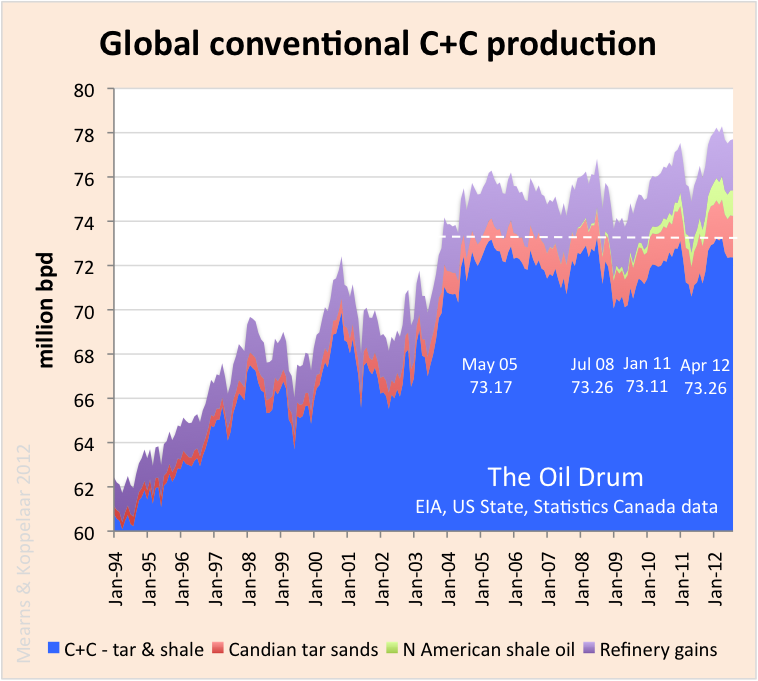

Perhaps the best ever illustration of this comes from a 2009 presentation made by Glen Sweetnam, a U.S. Energy Information Administration (EIA) official. The EIA is the statistical arm of the U.S. Department of Energy. The following chart from that presentation will upend any notion that we know exactly where all the oil we need to meet expected demand will come from.

PeakOil is You

The one chart about oil's future everyone should see

The one chart about oil's future everyone should see

![]() by Graeme » Sun 09 Dec 2012, 17:30:21

by Graeme » Sun 09 Dec 2012, 17:30:21

$this->bbcode_second_pass_quote('', 'T')he chart shows that by 2030 world output of oil and other liquid fuels from current fields is expected to drop to 43 million barrels per day (mbpd), some 62 million barrels below projected demand of 105 mbpd. (Though prepared in 2009, the chart takes into account known projects expected to be producing by 2012.) This drop is consistent with the observed decline in the worldwide rate of production from existing fields of about 4 percent per year. Certainly, there will be more projects identified in the 18 years ahead. And, many people will say that we already have a large new resource of tight oil (often mistakenly referred to as shale oil) which can be extracted through hydraulic fracturing or fracking. But even if the optimists are correct--and there can be no guarantee that they will be--this source of oil will only add 3 to 4 million barrels of daily production. What Sweetnam's chart tells us is that we must find and bring into production the equivalent of five new Saudi Arabias between now and 2030 in order to meet expected demand even if the volume of tight oil reaches its maximum projected output. (The Saudis currently produce about 11.7 mbpd of oil and other liquids.)

resourceinsights

Human history becomes more and more a race between education and catastrophe. H. G. Wells.

Fatih Birol's motto: leave oil before it leaves us.

Fatih Birol's motto: leave oil before it leaves us.

-

Graeme - Fusion

- Posts: 13258

- Joined: Fri 04 Mar 2005, 04:00:00

- Location: New Zealand

Re: The one chart about oil's future everyone should see

![]() by Plantagenet » Sun 09 Dec 2012, 17:36:45

by Plantagenet » Sun 09 Dec 2012, 17:36:45

Do you have EIA chart from a date more recent than 2009?

There is no point in discussing out-of-date charts from the EIA when the success of slickwater hydrofracturing in increasing oil producton in areas like the Bakken has significantly changed the EIA's view from what it was 3 years ago.

There is no point in discussing out-of-date charts from the EIA when the success of slickwater hydrofracturing in increasing oil producton in areas like the Bakken has significantly changed the EIA's view from what it was 3 years ago.

Never underestimate the ability of Joe Biden to f#@% things up---Barack Obama

-----------------------------------------------------------

Keep running between the raindrops.

-----------------------------------------------------------

Keep running between the raindrops.

-

Plantagenet - Expert

- Posts: 26765

- Joined: Mon 09 Apr 2007, 03:00:00

- Location: Alaska (its much bigger than Texas).

Re: The one chart about oil's future everyone should see

![]() by dissident » Sun 09 Dec 2012, 18:31:06

by dissident » Sun 09 Dec 2012, 18:31:06

The Bakken is a joke. Some CRI clown highballs the estimate to 24 billion barrels and people think there are trillions. The US consumes over 6.6 billion barrels per year so the whole Bakken with the unverified highball estimate from CRI is worth 3.6 years of US oil consumption. The Bakken is not a precedent for the world's oil reservoirs. Following your logic if the USGS estimate of 3.65 billion barrels of Bakken reserves become the unverified 24 billion claimed by CRI then every major oil field in the world could be scaled up by a factor of 7. This is BS, the major oil reservoirs such as Ghawar will not experience any increase from frakking technology.

So the OP highlights the main problem that frakking can't address and that is where to find 62 million barrels per day of oil production by 2030. Where are the dozens of Bakkens around the world? Nowhere.

So the OP highlights the main problem that frakking can't address and that is where to find 62 million barrels per day of oil production by 2030. Where are the dozens of Bakkens around the world? Nowhere.

- dissident

- Expert

- Posts: 6458

- Joined: Sat 08 Apr 2006, 03:00:00

Re: The one chart about oil's future everyone should see

![]() by Plantagenet » Sun 09 Dec 2012, 19:31:14

by Plantagenet » Sun 09 Dec 2012, 19:31:14

$this->bbcode_second_pass_quote('dissident', 'T')he Bakken is a joke.... The US consumes over 6.6 billion barrels per year so the whole Bakken with the unverified highball estimate from CRI is worth 3.6 years of US oil consumption.

Yes, of course, but in the real world oil production doesn't work that way Oil fields aren't drained in sequence so first one is used up in 3.6 years and then the next one is drained. In the real world a new oilfield like the Bakken is going to be producing oil for many decades.

Surely if we are going to discuss peak oil we should look at the most current and accurate data, rather then data from 2009.

-

Plantagenet - Expert

- Posts: 26765

- Joined: Mon 09 Apr 2007, 03:00:00

- Location: Alaska (its much bigger than Texas).

Re: The one chart about oil's future everyone should see

![]() by meemoe_uk » Mon 10 Dec 2012, 15:42:54

by meemoe_uk » Mon 10 Dec 2012, 15:42:54

Well yeah, but isn't the one chart peakers and running-outers have been peddling since the invention of graphs? - i.e. now is peak, the future is collapse. We've seen it all before, years ago.

-

meemoe_uk - Tar Sands

- Posts: 948

- Joined: Tue 22 May 2007, 03:00:00

Re: The one chart about oil's future everyone should see

![]() by rockdoc123 » Mon 10 Dec 2012, 16:26:52

by rockdoc123 » Mon 10 Dec 2012, 16:26:52

$this->bbcode_second_pass_quote('', 'F')racted tight-shale oil will follow the same pattern as fracted tight-natural gas; explosive production increase followed by exponential decline rate, but worse. Oil, (thicker than natural gas) will fill in the fractures and pores in shale faster, requiring ever more multiple, expensive, time consuming fracts. The industry is ripe for a collapse, just like natural gas. Where will the rigs go to then? A museum?

Nonsense. The decline rates in oil shale wells is well established for a number of reservoirs including the Bakken. There is a range of declines and hence associated EUR/well but the type curve and EUR can be fairly well established from IP rate. The production profile is step initially but then flattens out and becomes hyperbolic. And the oil will not behave as you suggest, it is not heavy nor particularily viscous, generally with very high GOR. The fracs that occur are propped with porous and permeable sand or ceramic beads. This is the pathway by which the oil can migrate into the borehole. A pressure drop is induced via downhole pumps which allows for the flow. New wells are added in order to increase both production and reserves. An example would be a single well that might produce initially at 500 barrels per day and then decline to 150 barrels per day where it remains relatively flat for a number of years might end up with ultimate production of say 2 MMB. If instead 6 wells are drilled from the same wellpad with spacings of 200 metres you will have drained nearly a section of land (640 acres) with total reserves of 12 MMB and a flat production for a number of years of close to 1000 bpd.

And once again the gas industry is in tough times not because of a failure in shale gas but the exact opposite. It was so successful that the market was flooded with gas, storage facilities nearly filled year round and hence the commodity price dropped as supply and demand would dictate. This could happen to oil if they are as successful and would result in an even bigger split between WTI and Brent. The difference in this case is that oil is much more transportable than gas. At the right price buyers would acquire cheaper WTI and ship it to Europe. If enough export were to occur then you would see WTI and Brent converge again. So unlike gas I think there is a natural mechanism which will limit how bad of a crash North American oil producers might endure.

-

rockdoc123 - Expert

- Posts: 7685

- Joined: Mon 16 May 2005, 03:00:00

Up, up, and away!!

Up, up, and away!!