Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on October 6, 2016

What Hubbert Practitioners, Art Berman, And The EIA Agree On With Shale Oil

Summary

The dramatic production resurgence of two countries that peaked over 30 years ago is ironically changing perception of peak oil today.

US shale oil is an indispensable prop keeping us from high oil prices.

There is close agreement among the minds that should know on the longevity of the US shale oil revolution.

Oil Is Oil

A big problem with energy thinking today is the notion that “oil is oil” and it doesn’t matter where it came from. Wrong! A major criticism you see of Hubbert is when they point to all the “oil” we’ve found (shale oil, tar sand, kindling wood) and throw it in the URR pot (Ultimate Recoverable Resource) and generate a production curve. This is not Hubbert’s method at all, and when you see them doing this, you can ignore the whole analysis. It totally misses the vastly different set of recovery physics between conventional crude and shale, or anything else. Each set of physics demands its own Hubbert tabulation. His method can be done, for example, with the coal production of Australia, or any resource that has and will have fairly consistent recovery geophysics.

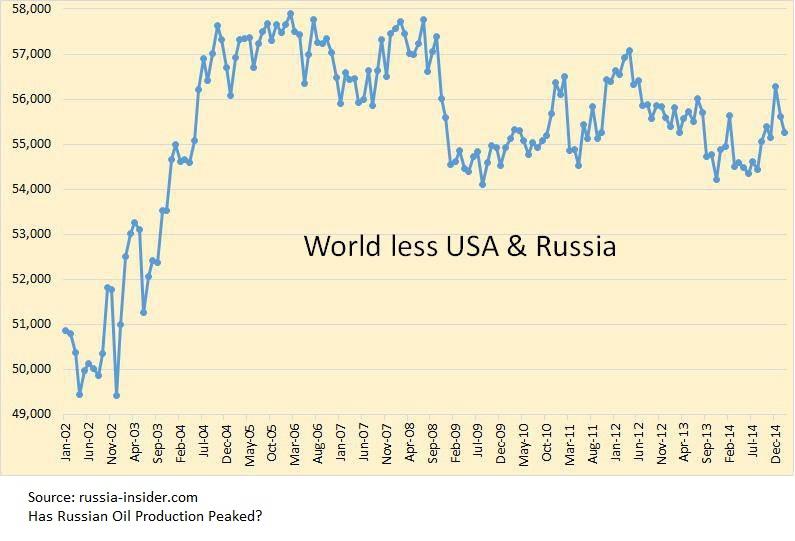

The shale oil of the US is ultra critical to oil prices and the world economy. A little considered fact with oil is that world conventional production has been declining since 2005 except for just two players:

Ken Deffeyes, using Hubbert knowledge he learned from him personally, wrote his book Beyond Oil: The View From Hubbert’s Peak in 2005 where he said the peak is:

postulated as 24 November 2005 (`Thanksgiving’ Day), after this date world oil will go into decline, slowly at first then more rapidly

This was for world conventional oil. Considering that the two players left out of the graph above are climbing almost entirely with shale (US) and bypassed oil (Russia) what you have shown is the world’s conventional oil production. Deffeyes missed the peak by maybe a few days.

Isn’t it ironic that these two big players, whose oil peaked over 30 years ago at the height of the cold war, are now both displaying a production resurgence that is changing perception of peak oil today. I discuss what’s up with Russia here , which may have a lot to do with the cold war. But what about the amazing shale revolution of the US? It is very critical to the global picture, so it would behoove us to use the best projection tool there is to see about the future of shale. This method requires a few years of actual production data to make its projection. Now that we’ve had a few years of shale oil production, has anyone bothered to tabulate a true Hubbert curve for our shale oil ?

Yes. Tad Patzek has done a Hubbert curve on the two big shale oil plays of the US and published them earlier this year – “Is US Shale Oil Production Peaking?”

Who Is Tad Patzek?

Tad Patzek is Professor of Petroleum and Chemical Engineering at the Earth Sciences Division and Director of the Upstream Petroleum Engineering Center in KAUST, Saudi Arabia. You can read his blog here.

He and Art Berman, a “good friend”, collaborate to make Hubbert curves for both gas and oil in the shale fields. Berman supplies the data and Patzek does the rest. According to Wikipedia,

“The focus of his research is mathematical modeling of earth systems with an emphasis on multiphase fluid flow physics and rock mechanics [spending] years as a researcher at Shell Development under M. King Hubbert”

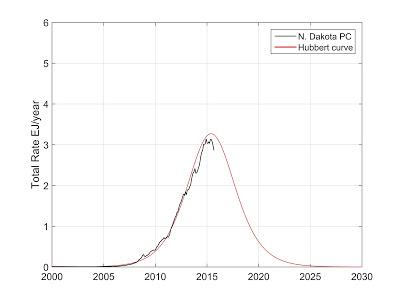

A fellow grasshopper of Hubbert, like Deffeyes, he generates curves per the methods used in his highly cited study “A Global Coal Production Forecast With Multi-cycle Hubbert Analysis”. If anyone on earth is qualified to make a Hubbert curve for Shale, it would be Patzek. Here is the Bakken:

And here is the Eagle Ford:

This is all very unsettling when you consider that the only thing propping us up from a return to Hubbert’s curve for conventional, where we were driven to over $100 a barrel in 2012, is the current US shale oil boom we are enjoying. That’s over 4 mb/d, and the two plays pictured above account for over 3 mb/d of that. Are we soon to lose our only prop saving us from peak net energy? This would have severe consequences on the price of oil out 5 years and beyond.

Patzek isn’t the only one using Hubbert’s method on US shale. David Archibald has done some curves that closely agree with the above in “The Imminent Peak In US Oil Production” posted over two years ago at Peak Oil Barrel, where the site’s subtitle reads “The Reported Death Of Peak Oil Has Been Greatly Exaggerated”.

The over-production problem I’ve discussed in other articles for the large conventional fields of Russia and Saudi Arabia may apply also to our shale oil when you consider that the shale drilling boom was fueled by free money and a massive debt frenzy. Instead of price wars or cold wars running the oil fields, we’ve had the bankers running our fields. The mechanics of shale over-production are different, but whatever they are, there has probably been a lot of it. A Bloomberg article “Refracing Is The New Fracking” points to one possible over-production mechanism, new fracking blasts before a well’s first fracking production is over:

It’s easy for things to go wrong. If poorly executed, the maneuver could take oil from the producing zones of other wells, or worse yet, ruin a reservoir. Then there’s the concern that some industry analysts have that a refrack only accelerates the flow without increasing the actual total output over the life of the well. EOG is among the drillers that remain reluctant to start using the procedure.

Patzek views refracking as a poor substitute for making a good well to begin with:

As to the refracking the jury is out. Very poor wells may see some increase of production. Very long wells cannot be reentered towards the toe. Other wells may see the new fractures linking back to the old ones with no incremental benefit. I think that the technology of controlled refracking will improve, but I doubt if it will change the picture dramatically. The key is to make a good well first time around and improve how this well is hydrofractured. There is a lot of work done everywhere on this subject, including yours truly.

Arthur Berman is a consultant to several oil companies and provides guidance to capital formation and investment conferences. He is an energy contributor at Forbes and is interviewed often on CNN, CNBC, and other major media outlets. Does Berman buy this popular notion that we have many decades worth of shale oil to rely on? Well, he recently wrote an article titled, “Why Today’s Shale Era Is The Retirement Party For Oil Production” wherein he states:

… looking at the Eagle Ford shale … even the EIA shows Eagle Ford oil production peaking in 2016… Where do we get this decades of production? … Eagle Ford isn’t going to stop in 2016; it will go on for many, many years, but at greatly reduced rates of production every year … They look at the US tight oil plays and they see a couple of years, maybe five years before things start to fall off.

Rex Weyler, a director of Greenpeace said of shale:

In spite of huge shale and tar reserve discoveries, peak discoveries remain well behind us, in the 1960s. My father, a petroleum geologist his entire life (and still, in Houston, Kazakstan…), knew about shale and tar deposits when I was a teenager in the 1960s. He called them “the dregs.” These deposits are not really news within the oil industry. And they are the dregs because of high cost, low EROI and rapid depletion.

It is only prices around $100 that brings dreg oil out. Fracking was invented in 1947. It is less a technology revolution than a price revolution. Berman doesn’t think the popular $60 figure for their profit point is right – more like $85-$95. He looks at free cash flow as a big measure of this. If you look at cash flow from operations on these companies, it’s typically good if oil stays above $60. With free cash flow including a lot of future building cap-ex, Berman seems to be stretching present costs to cover typical future ambitions. He claims in the above article that, “these plays cannot survive on anything other than sustained $100, $90, $95 oil prices and that is the bottom line.”

The profit points may be debatable, but the awestruck view of shale as new vistas of added oil supply seems like a pipe dream of either bad analysis or head-in-the-shale ignorance. Berman agrees:

… once your conventional production peaks, then you are going to be increasingly driven to more expensive, lower quality kinds of sources and that is exactly what we are seeing … Sure, we will find something more than what we have. Will we find the equal of what we found so far? Highly unlikely … I mean, these shale basins are not news … The big companies have had teams of geologists and geophysicists and engineers studying them for decades … so when the prices got high enough and the technology arrived … companies knew exactly where to go.

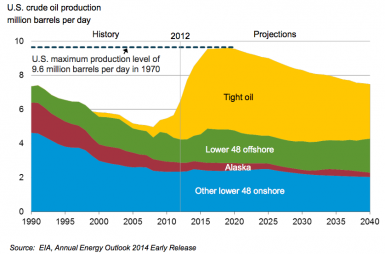

If you look at the EIA total shale oil projection, you can see this “sweet spot first” effect evident in their production profile:

Here we see pretty much the same peak time frame for shale (yellow) as the Hubbert curves for the Eagle Ford and Bakken plays, the two sweetest of the sweet spots, with the super-fast ramp-ups in production. The giant, high quality Permian Basin is also contributing to this profile, but with a slower climb and a slower projected decline. The sharp climb pictured closely reflects what Eagle Ford/Bakken has done while the EIA sees the Permian and the sum of all the lesser plays coming on line hereafter plateauing a top and making for a much slower decline than just the two big play Hubbert curves. But they still see about the same overall top that the two big, explosive plays may produce by Hubbert linearization.

You have all these independent means of analysis in Tad Patzek, Art Berman, and the EIA in close agreement. Patzek is using Hubbert’s math method (with Berman’s data) while Berman does meticulous well-by-well reserve data accounting. And they both agree on a shale oil production peak in 3 years or less. The EIA also is projecting this with a 2020 peak. If that’s all true, in just 3 years, conventional will be declining along with shale oil. With these declines, the only meaningful prop keeping us above Hubbert’s curve for conventional oil will then be buckling, and we will once more be in a losing battle with rising demand, as we were briefly before the shale sweet spots ignited in 2012. You will probably want to be long oil once this condition sets in, barring a really bad global economy.

Shale Oil outside the US

The EIA says the US has 78 of world’s 419 billion barrels of unproved technically recoverable reserves of shale oil. There is shale outside the US, but as explained in this study, “The Shale Oil Boom: A US Phenomenon” it is unlikely that the US shale explosion will be replicated elsewhere. The reason – logistics:

- The shale boom has depended on an exponential growth of wells drilled. Unlike conventional, shale oil requires punching holes in rock like crazy like a machine gun. No other country has anything like the drilling rigs of the US, where 60% of all the rigs in the world are. They simply don’t have the tools or crews to make it happen. The study concluded that this is unlikely to change in this decade because of the time needed to build and man the right rigs and equipment.

- Also a problem is that the thousands of new wells a year will be impossible in the more populated areas like Europe due to environmental and other concerns.

- And nowhere but the US do you have the small independent oil companies that are needed to take on the fast moving, high risk business profile of shale. And in most other countries with shale, the property is state owned with issues unlike the private and freely sold property rights of the US.

- Also in other countries, they don’t have the pipeline infrastructure or water supply needed by the water intensive shale business.

The study concluded:

For all these reasons. it is difficult to believe that a US style shale revolution may occur in any other part of the world in the foreseeable future.

The other shale plays in the world will be played – eventually. As oil stays high enough, these countries will deal with all the above logistic roadblocks, and this oil will find its way onto the market. If the “dreg” US shale card soon goes into a decline, there are other cards to play in global net energy supply. But how quickly can those cards be played? It will likely be in small, erratic doses.

This is why it is so critical to build the natural gas bridge away from oil, as I and others have been writing about for 10 years now. Fracked natural gas has much different dynamics and will peak much later than oil, (around 2040 by Hubbert and other means) and is a much superior transportation fuel than refined oil. The Pickens Plan is needed more urgently now than ever.

49 Comments on "What Hubbert Practitioners, Art Berman, And The EIA Agree On With Shale Oil"

shortonoil on Thu, 6th Oct 2016 7:11 am

“But what about the amazing shale revolution of the US? It is very critical to the global picture, so it would behoove us to use the best projection tool there is to see about the future of shale. “

OH, yes! The amazing “shale revolution”. An enterprise that has spent over $1 trillion to create an industry that has $362 billion in annual sales. Which means that if it generated a 10% profit margin on its gross sales (which it obviously does not) and paid no interest on its investment capital it would require 27 years to repay the principle.

It is absolutely amazing; that anyone can still be convinced to invest a nickel into it. What is amazing is the amount of credulity that exists. But as W.C. Fields said, “a sucker born every day; just enough to make a living”!

Boat on Thu, 6th Oct 2016 8:29 am

Alaska’s 10 Billion Barrel Oil Discovery: What You Need To Know

http://www.forbes.com/sites/ellenrwald/2016/10/06/alaskas-10-billion-barrel-oil-discovery-what-you-need-to-know/#42dcd9ac33dd

joe on Thu, 6th Oct 2016 8:54 am

I think the reason for a lack of fracking outside the US is more complex. Another reason is lack of interest, many nations are poorer and less energy intensive, they also have a less developed capital investment infrastructure and therefore dont have access to capital. The cost of money and taxes are higher in other countries, many countries are locked into contracts with the likes of Saudi and also get their oil from Libya, Nigeria and Iraq. Many countries use natural gas instead of oil so the demand is lower.

Fracking is a way for America to stay relevant in the oil industry, without it they would be way down the list by now. Britain too is running out of oil, they are looking at ways to substitute fracked oil for the loss of North Sea oil. In my opinion Brexit is more about peak oil than anything. If Britain has to go cap in hand to Brussels to keep the lights on, they will lose everything and be nothing more than a German naval base and a US landing strip. Brexit now will give them a chance to develop new trade options and become very good middle men for trade outside the EU.

rockman on Thu, 6th Oct 2016 9:05 am

“Fracked natural gas has much different dynamics and will peak much later than oil, (around 2040 by Hubbert and other means)…

First, according to the EIA, the primary frac’d NG trends have already peaked. Will they peak at a higher rate in the future? Certainly a possibility if the number of new wells increases significant. But the longer it takes for the drilling to kick the more existing production will decline making it increasingly more difficult to get back to the former peaks in the Marcellus and Utica. And then there’s the obvious: even if prices increase enough to spur more drilling the unconventional NG trends are no different then EVERY oil/NG trends ever developed: there are a finite number of locations left to drill. Also typical: the better producing wells are drilled early in the plays with later wells yielding poorer results.

And in case some still don’t know: despite the great boom in unconventional NG production the US is still a NET NG IMPORTER. By just a tad but we still consume more NG then we deliver domestically.

“…and is a much superior transportation fuel than refined oil”. Obviously not…at least not yet. Perhaps in THEORY (subject to how one defines “superior”). Given the VERY small number of NG fueled vehicles on the road today and an almost nonexistent motor fuel distribution infrastructure NG is hardly worth mentioning let alone calling it “much superior” to oil today.

Boat on Thu, 6th Oct 2016 9:23 am

short,

http://www.eia.gov/petroleum/marketing/monthly/pdf/pmmtab20.pdf

Why is that camel pee you so often criticize so valuable to refiners. Look at the bottom line of the chart. seems to me refiners love the stuff.

What oil brings the highest price? api of 30-35. The Hills group didn’t even include that api in their model according to you. 35-45 was the only oil deemed worthy. The Hills group model is so bad it’s issues have issues.

90+ percent of US imports is oil with an api of less than 35. Bottom line, your model has nothing to do with reality.

https://www.eia.gov/todayinenergy/detail.php?id=26132

Boat on Thu, 6th Oct 2016 9:32 am

“90+ percent of US imports is oil with an api of less than 35.”

I meant to say 70+ percent of US refined oil has an api of less than 35 and over 45.

rockman on Thu, 6th Oct 2016 9:39 am

Joe – Actually the main reason we won’t see a global shale boom is rather simple: lack of drill rigs. During the height of the drilling boom the US and Canada had 65% of all the drill rigs ON THE ENTIRE PLANET. And you mention the UK: during the boom all of Europe (not just the UK) had 3.5% of the rigs. That’s 150 rigs compared to 2,300 for the US + C. Couldn’t find the UK specially but probably less the 1% of the global onshore drill rigs.

And even with what rigs are available frac’ng equipment is even much more scarce.

As you offer there are a host of reasons why there’s little global shale potential. If nothing else the almost nonexistent positive foreign results during the shale drilling boom proves it.

marmico on Thu, 6th Oct 2016 9:47 am

Why use the vintage 2014 early Annual Energy Outlook when the 2016 Annual Energy Outlook paints a different picture?

http://www.eia.gov/forecasts/aeo/images/fig_mt-54.png

The 2016 projection out to 2040 says ~11 million b/d production whereas the 2014 projection says ~7.5 million b/d.

Looks like more ass-covering from Artie ASPO Berman.

rockman on Thu, 6th Oct 2016 10:03 am

Boat – “I meant to say 70+ percent of US refined oil has an api of less than 35 and over 45.” Actually what you probably meant to say: “70+ percent of US PRODUCED oil has an api of less than 35 and over 45.

US refinery runs are typically made with BLENDED oils with a rather narrow range…31 to 33 API. Which is why the US had to import a lot of light oil before our shale boom to blend with our domestic and imported heavy oils. BTW no US refinery processes Canadian oil sands production. They refine blends made of it and a sh*tload of light condernsate. LOL.

For instance most folks think Cushing, OK (the largest single oil storage facility in the world) was created just to store oil. It wasn’t: common sense…why would so much oil be stored so far way from our primary refinery regions? Cushing is the largest BLENDING facility on the planet. And if you going to mix that much oil you need a lot of storage tanks.

But there’s been some changes. Much of the oil shipped from Cushing isn’t owned by producers but by oil BLENDING COMPANIES that don’t own a single well. But for the last couple of years refiners didn’t like much of the blends they were offered (depends on much more then just API gravity). So some refiners are buying oil directly from producers and designing their own blends.

marmico on Thu, 6th Oct 2016 10:07 am

Average API gravity, historical + projected.

http://www.eia.gov/forecasts/aeo/images/fig_mt-55.png

shortonoil on Thu, 6th Oct 2016 10:10 am

What part of a 27 year pay back (with no interest) are you folks having trouble with: the 2 or the 7?

Apneaman on Thu, 6th Oct 2016 10:40 am

Oh yeah, I’m a dedicated Hubbert practitioner. I do 1/2 an hour every morning just before I do my cardio.

Davy on Thu, 6th Oct 2016 10:46 am

Good read on bad if oil prices go lower and dollar goes higher

http://www.zerohedge.com/news/2016-10-06/global-economic-nuclear-options-oil-pinned-below-30barrel-us-dollar-rising

Kenz300 on Thu, 6th Oct 2016 11:00 am

Climate Change is real. It will be the defining issue of our lives.

Go electric. No emissions.

Electric cars, electric trucks, bicycles and electric mass transit are the future. Fossil fuel ICE cars are the past.

Think teen agers vs your grand father. cell phones vs land lines.

Save money. .no stopping at gas stations. no oil changes. less overall maintenance

Geogeezer on Thu, 6th Oct 2016 11:10 am

Several problems here.

1) The “peaks” shown for the Bakken and Eagle Ford don’t quite rise to the level of irrelevant. Production from both has fallen recently because of a near cessation of drilling. The current price drop is the controlling factor.

2) With “shale” exploitation being primarily in the US and only 25 years old there is insufficient data for a Hubbert type analysis. I have no quarrel with making the attempt but it should be done with the clear knowledge that (a) short-term fluctuations such as the current price downturn will lead to a jagged irregular curve and (b) we’ll have a MUCH better probability of getting it right when the rest of the world has been “adequately” tested.

3) To point out that knowledgeable industry professionals were well aware of the hydrocarbons in the Eagle Ford, Barnett, etc. is on target. However, to state that industry was just waiting for the right price is a miss. when George Mitchell opened the Barnett the entire industry was in shock. It was the unique application of technologies – horizontal drilling and fracking – that made these resources available. Price was NOT the prime driver.

4) Many of the “sweet spots in shale” were well-known and have been exploited for decades. It was the unique combination of technologies that turned them from sure-things with low profitability to apparent bonanzas. In the mid 1980s I convinced a client to include a couple of Spraberry wells in the Permian Basin in a package of two corner shots in established fields and two wildcats. The logic was simple – two probable dry holes (wildcats), two probable good wells (corner shots), and two weak wells that would still be producing when we were all dead. and that’s how it worked out. The Karnes County and westward as well as the Leon County sweet spot were known decades ago as “shaley lime” and “sandy shale” zones in the Eagle Ford.

Are these “sweet spots in shale” less desirable to producers than the prolific fat sands of 50 years ago? Of course. Do they contain more (or less) reserves? The jury is still out.

The path on which the petroleum industry finds itself is a well-worn one. In the year 1900 economic copper ore had to contain in excess of 1% Copper. Today the economic limit is about 0.4% Copper. Gold ore used to contain visible Gold. Since the late 1800s the typical grade has declined from about 20 g/ton to less than 5 and in the US is currently about 1 g/ton. In the process the availability of both Copper and Gold has increased exponentially. Guess what’s happening with petroleum!

rockman on Thu, 6th Oct 2016 2:49 pm

“With “shale” exploitation being primarily in the US and only 25 years old there is insufficient data for a Hubbert type analysis”. Actually even worse: Hubbert studied the distribution of production from unique and geographically separated “fields”. The EFS is not a field but a TREND. The Texas Rail Road Commission may list about 25 EFS “fields” but that’s just formality because each producing well has to be designated as part of a field. But some fields share a lease line with another field. Call them Field A and Field B. I could drill a new well close to those two fields and fill in the FIELD blank on the paper work as Field A, Field B or even a brand new Field C. And the TRRC couldn’t care less what I choose. It’s just an accounting protocol.

Speaking of which no company reports the production from each of its wells. If a company has 5 EFS wells on the same lease the state only gets one production number for all 5 wells. So if Lease B in Field C produces 10,000 bbls in September it might be from 5 wells or 1 well. And even if you research and discover those 5 wells there’s no way to determine if each made 2,000 bbls or if one made 9,000 bbls and the other 4 made the 1,000 bbls.

IOW it can be very difficult to impossible to characterize an EFS “field”. IOW no ” Hubbert curve”. But the Bakken tends to be different. Those accumulations tend to be more unique and geographically separated areas.

“However, to state that industry was just waiting for the right price is a miss. when George Mitchell opened the Barnett the entire industry was in shock. It was the unique application of technologies – horizontal drilling and fracking – that made these resources available. Price was NOT the prime driver.”

Completely unsupportable by the FACTS. Years before George jumped on the Barnett the hottest oil play on the planet was the drilling of thousands of HORIZONTAL wells in the Austin Chalk carbonate shale in Texas. And before the play ended covered an area much larger the the current EFS extent. And the AC play was commercial at a lower price because it DID NOT require expensive frac’ng. The Rockman drilled horizontal AC wells with laterals much longer then most EFS wells.

In the 90’s we had the hz drilling tech to drill the EFS. We had the frac tech decades before the EFS boomed. In fact much of the frac’ng equipment used on the EFS wells existed in the 90’s…and earlier.

We didn’t develop the KNOWN reserves in the EFS in the 90’s when we had the HORIZONTAL TECH to do so because oil prices weren’t high enough.

Jasonstroberts on Thu, 6th Oct 2016 3:39 pm

I have the answer! I have the answer to peak oil! https://penzu.com/p/5a59bb84 There will be an Armageddon right when the Bible and the Koran say there will be an Armageddon! And exactly in the same place! The first 6 trumpets of Revelation have already sounded!

Davy on Thu, 6th Oct 2016 3:46 pm

Jason, your rapture will come and go but that dull achy feeling in your stomach will remain once collapse starts. When it gets bad enough you will be hoping for an Armageddon because you probably don’t have the guts to end things yourself.

Lucifer on Thu, 6th Oct 2016 6:57 pm

Jason, here is the good news, there will be no Armageddon for at least a few years. Trust me i know about these things. But just before the collapse starts i will let you know.

Boat on Thu, 6th Oct 2016 10:09 pm

rock,

We didn’t develop the KNOWN reserves in the EFS in the 90’s when we had the HORIZONTAL TECH to do so because oil prices weren’t high enough.

Even after fracking 40-90 percent is left waiting for the next round of tech/high prices.

rockman on Thu, 6th Oct 2016 10:51 pm

“…is left waiting for the next round of tech/high prices.” I wouldn’t my breath for the next “round of tech”. The same tech is being deployed to drill 18,000′ laterals with 100+ frac stages that was used back when the started doing 1,000′ laterals with 6 frac stages. All they been doing these is what they were doing years ago…just more of it.

I’ve often visited with the real tech developers, like Halliburton. They don’t even have fantasy ideas about anything more then what they’ve frtom the start. And now with the rig count cratered they don’t have much incentive to invent anything new.

As I posted several days ago Maersk Oil drilled 600 hz wells in the Persian Gulf starting over 10 years ago and were routinely drilling 30,000’+ hz laterals.

As I said: doing the same thing as we were in the EFS and Bakken. Just more of it. We’ve had the same hz drilling and frac tech for 25 years.

GregT on Thu, 6th Oct 2016 11:15 pm

Plenty of gold still out there Boat, just waiting for the next round of tech/high prices.

shortonoil on Fri, 7th Oct 2016 6:55 am

“Trust me i know about these things. But just before the collapse starts i will let you know. “

As the internet will be gone by the time the collapse has progressed very far, how do you intend to notify everyone? Greeting Cards?

Boat on Fri, 7th Oct 2016 7:34 am

Your learning greggiet.

Lucifer on Fri, 7th Oct 2016 8:39 am

Shorty,I suppose i could send my army of benevolent spirits to warn people just before the coming collapse, the people that want to be saved that is.

mx on Fri, 7th Oct 2016 9:30 am

IF Oil goes up Solar goes up too:

Solar at bargain prices now:

Yes, ALL the solar stocks are a BUY right now, most are below their 50 day moving average.

So, pick up some TAN, SPWR, FSLR, CSIQ, below their 50 day moving average = Bargains.

And also: SCTY, and RUN, good stocks with a big future.

Dredd on Fri, 7th Oct 2016 10:12 am

Humble Oil-Qaeda has pointed out that Oilah Akbar wants us to call it “Shale energy” not “Shale oil” …

In the next life in oil-qaeda heaven, those who do so will be given 70 jugs of shale energy to pour on the dead bodies of 70 virgins who were honor killed.

(Oilah Akbar! Oilah Akbar!)

yoshua on Fri, 7th Oct 2016 10:28 am

The world has now reached Peak Energy and Peak GDP.

The productivity growth has fallen to zero, profits have fallen to zero, interest rates have fallen to zero, government and corporate bonds have fallen to zero, the velocity of money is tanking and investments are grinding to a halt.

This is it. Things will get very nasty from here on.

shortonoil on Fri, 7th Oct 2016 10:42 am

“This is it. Things will get very nasty from here on. “

It is sort of like watching a safe fall from a 10th story window heading for the sidewalk. All one can hope for is that it is filled with helium.

Cloud9 on Fri, 7th Oct 2016 10:47 am

Prophecy has a way of being fulfilled. I am reminded of Bernal Diaz’s mention of the Aztec belief that white bearded gods would one day appear in Mexico bringing the end of the Aztec world with them. That belief combined with the insatiable demand for victims for sacrifice helped bring Indian allies to Cortez and his boys.

Then there is the association of the Aboriginal rainbow serpent with veins of uranium in Australia putting forth the notion that disturbing those veins will awaken the serpent and end mankind.

Such narratives are usually so vague that with a little imagination current circumstances can be configured to fit the prophecy. My problem with my some of my fellow Christians who tend to assume that we are in the end times lies with their presumption that they will be raptured out of the coming difficulties. This unfortunately fosters a do nothing attitude.

While I believe that the horde cannot be saved from the ongoing devolution, I do believe that enclaves of holdouts will form the remnant that will continue the species.

We all know that certain steps can be taken to mitigate collapse. Reasonable preparations are part of that strategy.

In the hysterical preparation for hurricane Mathew, I rushed out and bought three loaves of bread for the three households I am responsible for. That is all we wanted. We did not need to fill the pantry or buy generators or rush out to fill our gas tanks because we had already addressed those needs.

Robert Spoley on Fri, 7th Oct 2016 10:47 am

The reason we are drilling for “shale oil” is because we (the industry) are not allowed to drill for conventional oil by various governments and protest groups right here in the US of A. We have a north coast and a south coast in Alaska. An east and west coast of the lower 48 as well as the east 1/2 to 2/3ds of the east Gulf coast that have, for all practical purposes, not been touched. When prices get high enough, long enough, the folks who want their cake and eat it too, WILL CRATER and we will drill these areas. So much for shale oil. Oh yes! Then there’s methane hydrates. Once again “we have met the enemy and they is us”.

ghung on Fri, 7th Oct 2016 10:57 am

Robert Spoley said : “…. are not allowed to drill for conventional oil by various governments and protest groups right here in the US of A.”

It couldn’t be that we don’t want our coasts trashed by fuckups like happened at Macando, could it? Nah, that couldn’t be the reason….

Face it, Robert. You guys have such a bad a PR problem that even Oklahoma has to declare a “Pray for the Oil Industry” day. Meanwhile, investors keep losing their asses….

Apneaman on Fri, 7th Oct 2016 11:18 am

Robert Spoley , it does not and will not matter what “folks want”. I have long predicted (no brainer really) that as the great unwinding continues eventually environmental laws will be rolled back and/or unofficially ignored. Too bad for the plebs living nearby. Whatever it takes to kick the can a little longer. I do agree that most folks who are almost all NIMBY’s will either remain silent or cheer on the can kick no matter the cost. Just saying that their wants barely matter now and much less so as the unraveling continues.

Are you sure “protest groups” have the power to stop the industry? Sounds fishy to me.

Boat on Fri, 7th Oct 2016 12:16 pm

yoshua on Fri, 7th Oct 2016 10:28 am

The world has now reached Peak Energy and Peak GDP.

Apparently you don’t google much as a fact checking exercise. Start with “world btu consumption”. If you have trouble with other key word searches like “world gdp” just ask.

Step #2. Copy your link with one of your assertions. Then you will have proof that your an idiot by information you looked up your self.

marmico on Fri, 7th Oct 2016 12:36 pm

yoshua is a Turdburger. He is usually served up 2 shit sandwiches a month from the Turdburg. He recently lacks protein turds. Only one shit sandwich was plated in September and no shit sandwich so far in October.

yoshua on Fri, 7th Oct 2016 12:39 pm

Boat – Peak energy:

https://yearbook.enerdata.net/

shortonoil on Fri, 7th Oct 2016 1:01 pm

“The reason we are drilling for “shale oil” is because we (the industry) are not allowed to drill for conventional oil by various governments and protest groups right here in the US of A. We have a north coast and a south coast in Alaska. An east and west coast of the lower 48 as well as the east 1/2 to 2/3ds of the east Gulf coast that have, for all practical purposes, not been touched. “

If you have picked northern Alaska as a new source of oil for the US, you are beating a dead horse. Most of that oil is in the North Sack region, and with an API of 10 to 20.3 that is exactly where it is going to stay. Its estimated 9 Gb of oil, has never been economically feasible to extract and never will be; it is even farther out of reach with oil at $50/ barrel.

Here is a the study on Sack Alaska heavy oil;

http://repository.icse.utah.edu/dspace/bitstream/123456789/11235/1/ms_thesis_jonathan_wilkey-evaluation_of_the_economic_feasibility_of_heavy_oil_production_processes_for_west_sak_field.pdf

The industry has been spinning a lot of tall, tall tales lately; even more so than usual. If you aren’t familiar with the Hill’s Group this is a good time to get acquainted. We do our own research, and don’t just buy every yarn that some promoters would like to sell.

We have been around this whole scenario long enough to know that if it sounds too good to be true – it probably isn’t!

This one isn’t!

http://www.thehillsgroup.org/

Apneaman on Fri, 7th Oct 2016 1:14 pm

When the Next Hurricane Hits Texas

“Imagine a hurricane, a hurricane like Matthew, aimed straight at the heart of the American petrochemical industry.”

http://www.nytimes.com/2016/10/09/opinion/sunday/when-the-hurricane-hits-texas.html?_r=0

Apneaman on Fri, 7th Oct 2016 1:35 pm

Boat worships the Almighty GOOGLE.

Google is at the top of Boat’s authoritarian secular pantheon.

Lesser deities include: IEA, EIA, Texass RailRoad Commission, IMF, World Bank, CIA, and any econ 101 think tank that puts out conformation bias reinforcing graphs N charts.

Like the monotheistic deities, boats pantheon is all knowing and infallible even when they contradict themselves (it’s a god thing) and make blatant errors as they often do.

All mortal monkey people, bow to the Almighty GOOGLE and the lesser gods for they are your all knowing masters.

Boat on Fri, 7th Oct 2016 2:05 pm

ape,

https://search.usa.gov/search?utf8=%E2%9C%93&affiliate=eia.doe.gov&query=methodology&search=Submit

Estimating the technically recoverable oil and natural gas resource base in the United States is an evolving process. For shale gas and oil, the evolution of resource estimates is likely to continue for some time. The size of the technically recoverable oil and natural gas resource base in the United States becomes evident only as producers drill into geologic deposits with oil and gas potential and attempt to produce from them on a commercial basis. As producers find plays to be more or less bountiful than expected, resource estimates are adjusted to reflect that information. As time passes and our knowledge of the resource base and future technologies and management practices improves, estimates of the technically recoverable resource base will be refined. Consequently, the resource estimates in the current report will be modified over time as more wells are drilled and completed, technologies evolve, and the long-term performance of shale wells becomes better established.

The estimates of shale oil and shale gas resources provided here represent a reasonable estimate of the resource potential for those shale plays for which public information is currently available. The potential impacts of the current uncertainty regarding shale gas resources on projected natural gas supply, consumption, and prices are described in the AEO2011 Issues in Focus article, “Prospects for shale gas

http://ir.eia.gov/ngs/methodology.html

GregT on Fri, 7th Oct 2016 2:42 pm

“Then you will have proof that your an idiot by information you looked up your self.”

That would be; You’re an idiot, Boat.

Boat on Fri, 7th Oct 2016 3:04 pm

yoshua on Fri, 7th Oct 2016 12:39 pm

Except for 2010 every year is a new total energy peak including the last. Is this not correct?

GregT on Fri, 7th Oct 2016 3:09 pm

Still having trouble with the exponential function Boat?

Here try this:

The most important video you’ll ever see

https://www.youtube.com/watch?v=DZCm2QQZVYk

Simple enough for most 6 year olds to understand.

Truth Has A Liberal Bias on Fri, 7th Oct 2016 3:26 pm

@Kenz300

“Go electric. No emissions.”

lmfao where do you think electricity comes from dumbass, unicorn farts?

Oh and how about those turbines and solar panels, are they zero emissions to manufacture, maintain and replace?

You’re living in a dream world. You should worry more about the famine you’re gonna die in fairly soon.

Truth Has A Liberal Bias on Fri, 7th Oct 2016 3:27 pm

Boat has said at least once before that he’s an expert and you can be too, just use Google to find the answers you seek. You’ll be a subject matter expert by noon.

yoshua on Fri, 7th Oct 2016 3:40 pm

Boat – Sure, there was a minuscule growth from 2014 to 2015 if you like, but try to squeeze in economic growth in there. It looks more or less like we reached a plateau.

Here is an interesting speech to the Feds central bankers: http://www.zerohedge.com/news/2016-10-06/

godq3 on Fri, 7th Oct 2016 5:49 pm

China coal production down 10% so far this year.

http://www.reuters.com/article/china-economy-output-coal-idUSL3N1BO2R1

USA coal production down 25% in the second quarter

http://www.eia.gov/coal/production/quarterly/pdf/t1p01p1.pdf

Indonesia coal production drops 16% in first half of the year

http://news.xinhuanet.com/english/2016-07/21/c_135530947.htm

India coal production down 5% yoy in September

https://in.news.yahoo.com/coal-india-production-grows-0-2-april-september-150804654.html

godq3 on Fri, 7th Oct 2016 5:55 pm

^^ These four countries are responsible for 3/4 of world coal production. And coal provide our civilization almost as much enenergy, as oil.

Michael Andersen on Sat, 8th Oct 2016 8:08 pm

Howdy shortonoil, If you have not seen this article yet over on Zero Hedge I thought I would link it here for you and all the other peak oilers. The author of the article is referencing The Hills Group work and I commented that you were a regular here at Peakoil.com and have been spreading this gospel for quite some time. I threw my two bits in about easy and cheap oil causing this massive population overshoot which will result in a classic die off condition to occur when the forward momentum stops. I almost immediately got two down votes and likely will see many more over there. Folks are not willing to accept what I think is the easy math involved in all this. The comforting lies are much more preferred than the painful truth.

curlyq3

http://www.zerohedge.com/news/2016-10-08/warning-coming-collapse-us-net-worth-will-wipe-out-millions-americans