I follow the JODI World Oil Database primarily because it is now four months ahead of the EIA international data base. I make some adjustments however. I use the OPEC MOMR “secondary sources” for all OPEC data where JODI also uses the MOMR but uses their “direct communication” data instead. The OPEC portion of the JODI data is “crude only” and will therefore be somewhat less than the EIA reports.

I use the Canadian National Energy Base data for Canada instead of the strange numbers JODI has for Canada. And I use the EIA data for the few small producers that JODI does not report.

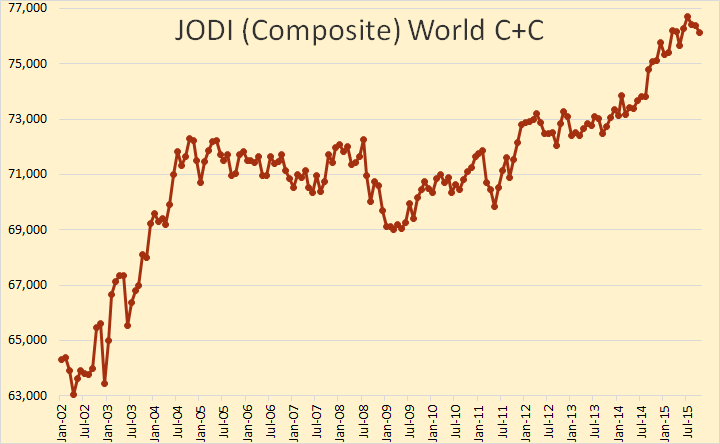

With these Changes I think I have composed an excellent World Oil Database from this composite data. And with the October data just released I have composed the below charts. The data is through October and is in thousand barrels per day.

World oil production peaked, so far, in July at 76,702,000 barrels per day and in October stood at 76,128,000 bpd or 574,000 bpd below the peak.

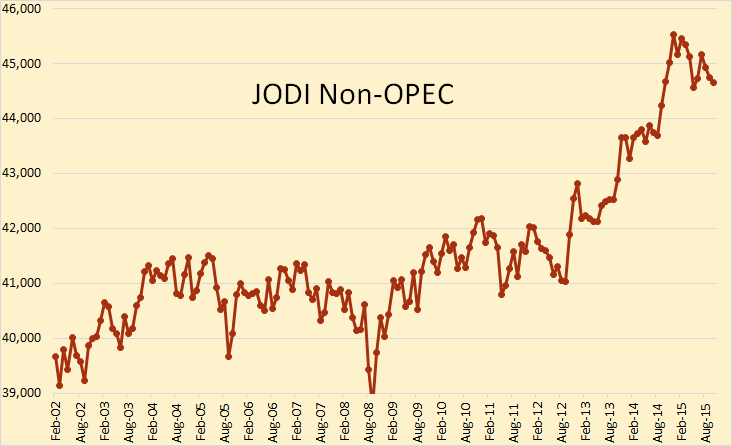

Non-OPEC peaked, so far, in December 2014 at 45,530,000 bpd and in October stood at 44,662,000, down 868,000 bpd or just under 2% in 10 months.

For the first time in 4 years Non-OPEC production has dropped below the level it was the same month the previous year. This means the 12 month trailing average has turned negative, though just barely.

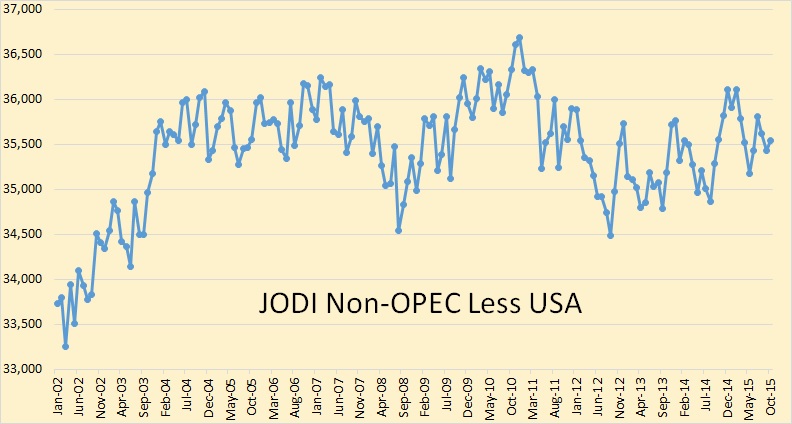

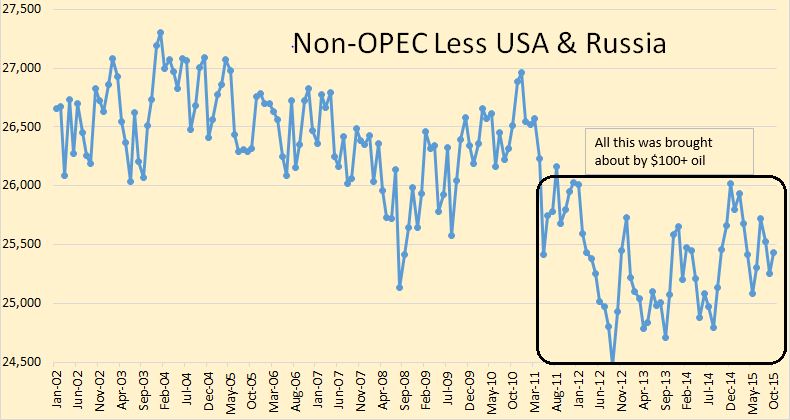

Non-OPEC less the USA has been on a 12 year bumpy plateau. In fact it stood at 35,422,000 barrels per day in October, 214,000 bpd less than the level reached in December 2003.

The data here, prior to 2012, is from the EIA. Russia and the USA are, by far, the two largest Non-OPEC producers. At best Russia has plateaued but most analysts predict she will begin to decline next year. I think that prognostication is correct. Russia, I believe, will slowly decline beginning in 2016.

The data for 2015 is the average for the first 10 months. Russia has increased production every year since 1999 except 2008 when we had the big crash. Some were expecting a similar crash in 2015. They were surprised: Siberian Surprise. I was not and I don’t expect a crash next year either. I just expect production in 2016 to be slightly less than this year.

Non-OPEC less USA and Russia is clearly in decline. Five years of oil prices above $100 could not prevent the decline. But $100 oil has brought a lot of Non-OPEC oil on line. What it did do was prevent this decline from being a lot steeper had oil been in the $60 or below range.

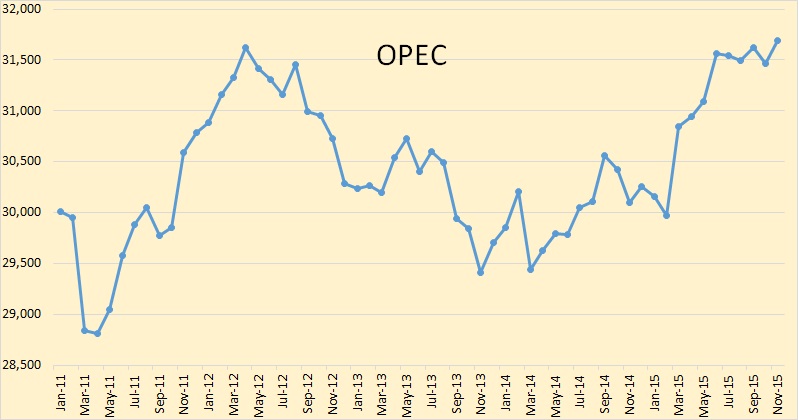

Of course if we are talking peak oil we must include OPEC. Above is OPEC crude only production through November. It is obvious, to me anyway, that OPEC is producing flat out. Only Iran has much potential to increase production. Most analysts think they can only production about half a million barrels per day. But that will only likely replace decline in other OPEC nations. OPEC production will likely hold steady for the next four or five years before starting a steady decline. OPEC production will not prevent peak oil.

Rockman, who posts now over on PeakOil.com, recently posted the following which I though was so clear and to the point that it deserved a post here also.

Looker: <i>“So in fact peak oil will really bite when it is not so economically viable to find and produce oil for the market.”</i>

Rockman replied: <i>Good point and there’s a great visual to emphasize that point: look at the US oil production curve. We peaked about 35 years ago. And during those decades the inflation adjusted price of oil was less the current prices…and considerably less then during the height of the shale boom.

And the shales boomed when oil price boomed. And not due to technology: horizontal drilling for unconventional reservoirs, like the Austin Chalk in Texas, was well established 15 years earlier. And fracking has changed very little for decades.

In other words US oil production peaked because oil prices essentially peaked decades ago. Yes: up and down but no great movement like we saw when the shales boomed. And US oil production almost reached a new peak because oil prices reached near peak levels once again. Which means that we may not only be at global PO but the longer it takes for oil prices to significantly increase we may never again approach current production levels as depletion continues to take its toll. The recent increase in global oil production actually is the result of low oil prices…not higher. The oil price collapse has forced some producers, like the KSA, to bring their reserve capacity into play so as to increase the revenue stream. Which also means the lower oil prices are also increasing the depletion rate of existing proven reserves as well as hampering the development of new reserves.

The recent oil price collapse may eventually be viewed as the ultimate “Oh shit” moment in the global energy dynamics.</i>

The upsurge in OPEC production that began in March 2015 is what Rockman is talking about when he says: <i>”The recent increase in global oil production actually is the result of low oil prices…not higher.”</i> That point should not be taken lightly. While high oil prices drove most nations to invest heavily in infill drilling and a few new fields, now that prices have collapsed they must produce every barrel possible to maintain their budgets.

Bottom line, I am more convinced than ever that 2015 will be the year world crude oil peaked.

rockman on Mon, 21st Dec 2015 2:59 pm

I’ll expect my royalty certificate for 1 gallon of Blue Bell before then end of the year. lol.

Pete Bauer on Mon, 21st Dec 2015 6:23 pm

At <= $35/barrel, we may have reached peak oil, but if the prices go up, the oil supply will also go up, but only by smaller percent.

Alternatives are coming in and picking up some share from Oil.

makati1 on Mon, 21st Dec 2015 8:07 pm

“All Roads Lead To Peak Oil”

SHeadline should read:

“All Roads Lead To Peak Burnable Liquids”

We passed peak petroleum about 10 years ago. Not worth my time to read.

Twocats on Mon, 21st Dec 2015 11:16 pm

The non opec less us and russia is an key chart. Iraq is another key one he could have taken out. But with us shale, world shale, and iran it seems like the world will have one more legit chance at peak. I mean 2005, 2008, 2010 were high production years. So ignoring the ever changing definition of oil for a second, we just wont know until price rebouds for several months with no concurrent like production increase. So until 2018 at a minimum i cant see how we can know.

Twocats on Mon, 21st Dec 2015 11:21 pm

*i said 2010 but that third undulation wss 2012 i think. But my point that you can bounce around for years only to pop up is a demonstrated potential. Oh and we’re powned either way. Merry Christmas.

makati1 on Mon, 21st Dec 2015 11:29 pm

Twocats, you cannot ignore the definition of oil. “So ignoring the ever changing definition of oil for a second,…” Oil is oil. It is NOT moonshine, grease drippings or any other pseudonym (fictitious name) that the oil company pimps use to keep the suckers on board for one more year.

True petroleum peaked in 2005. You can pretend all you want but facts are facts. The energy road is all downhill from here, getting steeper and the cliff is in sight. No brakes. Buckle up!

joe on Tue, 22nd Dec 2015 12:43 am

https://en.wikipedia.org/wiki/Fischer%E2%80%93Tropsch_process

Much of what we call ‘oil’ is literally made in giant kettles. Germany was able to substitute as much as 25% of its transport fuel with synthoil even as the Red Army overran its country. This was way back in 1945! We are capable of doing much more now.

But, heres the thing.

‘Peak Oil’, is really peak ‘easy oil’. Anyone interested in honest peak oil debates knows that ‘peak’ always meant easy oil, and that true speculators always imagined that ‘Tough’ oil would play a large role in the post peak world.

https://www.youtube.com/watch?v=TDgDKNr7aNY

The real issue in the last 10 years has been price volatility, and its likely that volatility will continue. Given the fact that easy oil mixed with all kinds of tough oil production combined with nuclear and renewables as well as gas we don’t have an energy issue, right now.

Volatility is the watch word in the future. Given the fact that in the future price volatility will damage oil dependent nations global politics will reflect that. This uncertainty will probably stunt growth and even if the dollar value of oil is low or high, its utility will be impacted, and so its true economic cost will be higher.

https://en.wikipedia.org/wiki/Utility

Its the same with most commodities. For example diamonds

https://en.wikipedia.org/wiki/Blood_diamond

http://www.kitco.com/ind/Zimnisky/2014-03-10-The-State-of-Global-Rough-Diamond-Supply-2014.html

Just as there synth oil, there are synth diamonds.

However, oil is unique, it moves people, and people are the economy.

makati1 on Tue, 22nd Dec 2015 4:39 am

Synth oil is just other energy form converted into a liquid that can be used in vehicles. Not more energy and likely much less than the original source be it coal, plants or cow farts. As I said, NET energy is on the down hill slide. There is less and less of it every year, while there are more and more people to consume what there is. The energy cliff is fast approaching.

Davy on Tue, 22nd Dec 2015 5:26 am

Peak easy oil is the key when one interjects economy into the equation. Our economic infrastructure was built on easy oil and a smaller population.

We have an economy under stress at the same time its foundational supporting resources is suffering a variety of depletion dynamics. Peak oil is an abstract analysis that is misused and little understood. It MUST be considered in relation to the economy. Shorts ETP is very useful for this.

My point is economy is as important as ETP. We will likely see economy a bigger factor than oil depletion soon. Once our complex global economy decays enough we will get a spiral of demand destroying supply.

I say the best word for it would be peak status quo. Everything revolves around economic activity in the end. There is no need for industrial supplies of oil without a global economy and no one knows how far economic activity will drop in a status quo collapse.

JuanP on Tue, 22nd Dec 2015 6:48 am

Excellent article! What can I say about such a good piece. There are no mistakes that I could find and I am a mean proofreader and copy editor. The graphs are excellent, too, they are very clear and each and everyone of them makes an important point. But nothing was more satisfying than having our Rock star, I meant to say Rockman but my unconscious betrayed me, quoted! 😉

All I could find wrong in this article was just one missing word, “Most analysts think they can only production about half a million barrels per day.” I think he meant to say that they can only INCREASE production about half a million bpd.

My congratulations to the author. It is a real pleasure to read a well written and illustrated article like this one for a change since most of the articles posted here at PO suck.

I come to this place for the comments and links provided by people like Apneaman, but I don’t read most of the articles posted at the forum. I start reading most of them, but I usually can’t finish them because reading all that crap is a painful experience for me.

Good job!

JuanP on Tue, 22nd Dec 2015 6:57 am

Rockman “Which means that we may not only be at global PO but the longer it takes for oil prices to significantly increase we may never again approach current production levels as depletion continues to take its toll.”

This is such an important point that it can’t be repeated enough, and I couldn’t agree more. It is exactly for comments like that one by Rock that I come here almost every day. I would have quoted the whole comment again because it was sooo good.

Thank you very much for your contributions, Rock. They make me smile and happy and give me a brief respite from my cronic and acute depression.

JuanP on Tue, 22nd Dec 2015 7:00 am

Twocats “Iraq is another key one he could have taken out.” But Iraq is an OPEC country so it was not included in that non OPEC list by definition, Twocats.

twocats on Tue, 22nd Dec 2015 7:01 am

“True petroleum peaked in 2005. You can pretend all you want but facts are facts. The energy road is all downhill from here, getting steeper and the cliff is in sight. No brakes. Buckle up!”

sooo if there is no debate facts are facts that peak oil is definitely past, why is this magical “cliff” of which you speak IN THE FUTURE? Why didn’t it happen years ago?

twocats on Tue, 22nd Dec 2015 7:03 am

Juan P, good catch, but my point wasn’t to put Iraq in the chart, my point is you’ve got three to five countries that are keeping the ENTIRE PLANET together, and that’s why Cheney wanted Iraq so badly, and that’s why invading Iraq was not only a good idea, but a roaring success (from an Imperial stand point), no matter what liberals say.

onlooker on Tue, 22nd Dec 2015 7:09 am

Yes Rock is unique for his expertise and acumen. Oh I also like that I appear also in this article haha. Seriously, though it appears that peak economy is intersecting with peak oil, in so much as consumers are maxed out and can hardly afford more expensive oil which in part explains the fall in prices. So demand has spurred maximum production but cannot stimulate it more because of the profit/cost ratio. Now we are positioned to really feel the effects of peak oil as a sputtering economy confronts eventual oil price rise as supply is lacking relative to a certain minimum level of demand.

JuanP on Tue, 22nd Dec 2015 7:13 am

Twocats, I understood your point and agree with it completely. The world is running out of places that could increase production even if prices went up again. I just clarified the detail because I think it’s very important to make these things very clear to people who are new to this subject and could get confused.

I agree with Rock that 2015 will very likely be the final peak and I know that both Rock and I agree with you that we will only be certain about it after a few years have passed. We are just manifesting an opinion, not stating a fact.

rockman on Tue, 22nd Dec 2015 12:32 pm

Cat – “…sooo if there is no debate facts are facts that peak oil is definitely past, why is this magical “cliff” of which you speak IN THE FUTURE? Why didn’t it happen years ago? You make some good points. To avoid the “what the f*ck is real oil” debate perhaps we should start thinking more about the PP…Peak Products. No one here buys oil. Virtually none of the public buys oil. The consumers all buy refinery products. And their focus is on price first and availability second. Probably everyone here has bought some gasoline in the last few weeks. Can anyone tell me how much of that fuel was made at least partially from Canadian oil sands production? From Eagle Ford light oil? From Venezuelan heavy? From Saudi light? From NGL’s that were added to blended Eagle Ford/Vz heavy? From corn?

I doubt anyone can. And more important: none of you give a f*ck either. lol. Granted there’s not a complete disconnect with the hydrocarbon sourced to make refinery products but there’s not a direct and consistent relationship either. And again, no one here cares what came in the back gate of the refinery…just what comes out the front gate and how much it costs.

And as explained to Pops in another post I see no “magical” or any other kind of cliff in future “oil” production. At least in the US but probably not globally either. I won’t repeat the details but simply say that the US has a base of production that’s in a relative low decline fate phase of its life. And while we did get a huge uptick in production thanks to the shale that won’t result in a shark fin curve either…at least no one lasting very long before it reverts back into a nice steady decline we’ve had for the 40 years prior to the shale boom.

Even the shale wells drilled 2+ years ago won’t themselves fall into a shark fin profile: while they might have declined 60% to 80% over the first 24 months afterwards that decline in their later years has fallen to 20%…or less. Those thousands of older EFS and Bakken wells have converted into slower declining rates more similar to our old (and extensive) conventional heritage wells.

Prior to the shale boom US oil production was only declining about 80k bbls/yr. About 20+ years ago US oil production was declining about 120k/bbls per year. So as fewer new high rate shale wells are drilled and as those drilled in the last 24 months will be producing a lot less NEW production as we’ve seen in the last 5 years, we’ll still have our relatively slowly declining base production fueling the economy.

Yes: still declining. But not falling off a cliff IMHO.

makati1 on Tue, 22nd Dec 2015 10:26 pm

NET energy is falling.

How many barrels of oil energy does it take to get one barrel of oily products to the end user?

How much oil energy does it take to get any burnable moonshine to the end user?

How many barrels of oil energy to get that degraded stuff we now call ‘coal’ to the end user?

Energy available at the user position has been falling since at least 1970.

How many barrels means nothing except to the oil pimps selling their lies. NET energy is what we have to work with and produce what we need. THAT is decreasing faster and faster and why economies are also decreasing faster and faster.

Davy on Wed, 23rd Dec 2015 4:41 am

Rock, I like your “peak products” as another definition in your “peak oil dynamics”.

Davy on Wed, 23rd Dec 2015 5:08 am

I see the oil production cliff as always possible because of the economic component of oil. It takes a robust global economy to produce and distribute oil products and employ them in the economy to bring a return on society’s macro investment.

The economy is now clearly in turbulence. It is growing here and there and decaying here and there. I don’t care who you are, knowing the real economic story has become an activity like knowing the long term weather. Human nature at a global level through trillions of economic decisions is beyond modeling at the level we see people commenting on it. In other words we have experts who are deceiving themselves often times by being in over their heads.

The economy is producing oil as much as any oil patch company is. These production entities are supported by a broad based economy at multiple levels of abstraction. This web of support means oil’s behavior is as much economic as geologic.

We no longer have a critical mass of cheap oil sources. We now have sources produced through intensive economic activity. Oil’s demand at the level we see today includes a high degree of complexity and energy intensive activities.

Oil is a commodity that clearly needs economies of scale to be global and at the volumes we see. Those of us who talk about this daily know oil is still plentiful geologically it is now a matter of what can be considered actual economic oil. Economic oil is the key today.

The economy is as much dependent on oil so we see a codependency of supply and demand both ways. What is so amazing now is the unstable codependency is in both directions. We have multiple adverse peak oil dynamics and multiple economic disturbances converging in a spiral of demand and supply destruction.

How long will this vital economic codependency remain at a level of economic activity to maintain economic confidence. It then becomes a systemic question of how long can human confidence provide the liquidity of exchange to maintain this global economic system with its vital oil products components. Economics is beginning to trump geology in many cases today as the key peak oil dynamic.

JuanP on Wed, 23rd Dec 2015 5:36 am

Rock, I agree that a shark fin outcome is unlikely. Oil production’s decline is likely to be gradual and take decades. Geopolitical events could cause some large drops along the way, though,but overall I believe it will be a long slow fall in production for the reasons you explained in your comment. It is not reasonable to expect a shark fin based on current trends and past experience with depletion.

Nony on Wed, 23rd Dec 2015 4:51 pm

EIA puts world crude oil and condensate at 80 MM bpd. Definitely up from the 73-74 MM bpd plateau of ~20005-2010.

https://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?tid=50&pid=57&aid=1&cid=&syid=2011&eyid=2015&freq=M&unit=TBPD

How that translates into a reasoned argument for an imminent peak eludes me. Ron tries an argument based on country by country analysis but he is always ready to believe some countries have to decline and skeptical that others can increase. But there’s no reason to support his comments. And he’s gotten his butt kicked time and time again on these predictions. (Russia in decline (2013), Iraq can’t go up (2014), etc. etc.)

Nony on Wed, 23rd Dec 2015 5:44 pm

Consider how Ron could have made the same argument in 2010:

*look, base decline blablabla…how much we have to replace where will it come from?

*what countries will go up? Maybe Canada and Brazil.

*Going down will be Saudi Arabia because Simmons, Staniford, Ghawar, blabla.

*Russia is peaked and in decline.

*The US is mature and dead.

*Iraq is all screwed up…don’t believe any of those comments about how it could increase…that is Yergin lies.

*And [even a stronger argument than currently available] look at the plateau from 2005 to 2010.

—-

And what happened 2010 to 2015:

*World production rose 5 MM bpd

*SA not only hung in there but is up 1-2 MM bpd. So much for super scientist Staniford. Back to computer jock.

*And the US, that last bastion of in your face capitalism is up 4+ MM bpd. DRILL BABY DRILL.

*Oh…and The Oil Drum closed down from terminal embarrassment.

Stewart Erickson on Wed, 23rd Dec 2015 10:30 pm

The Cliff is Arab Spring in Saudi Arabia. I recently went back an re-read Matt Simmons’ book Twilight in the Desert. Its a good book; worth serious study and re-review. All seven of the major Saudi fields now have gas caps and are entering what I believe will be steep decline. Based on production declines of other giant oil fields, I expect Saudi to lose a million barrels per day of production by 2017. The recent Saudi oil rhetoric is just that. Then “just connect the dots” as to what will unfold; higher cost of capital, no one will touch their debt, current “pay-off” system decays….

GregT on Wed, 23rd Dec 2015 11:33 pm

“And what happened 2010 to 2015:

*World production rose 5 MM bpd

*SA not only hung in there but is up 1-2 MM bpd. So much for super scientist Staniford. Back to computer jock.

*And the US, that last bastion of in your face capitalism is up 4+ MM bpd. DRILL BABY DRILL.

*Oh…and The Oil Drum closed down from terminal embarrassment.”

And the world’s economies continued to stagnate. Even with PRINT BABY PRINT. Strange that…….