Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on October 14, 2015

Bakken Production Down plus IEA Predictions

The Bakken and North Dakota production data is in.

Bakken production was down 19,502 bpd in August while all North Dakota was down 20,552 bpd.

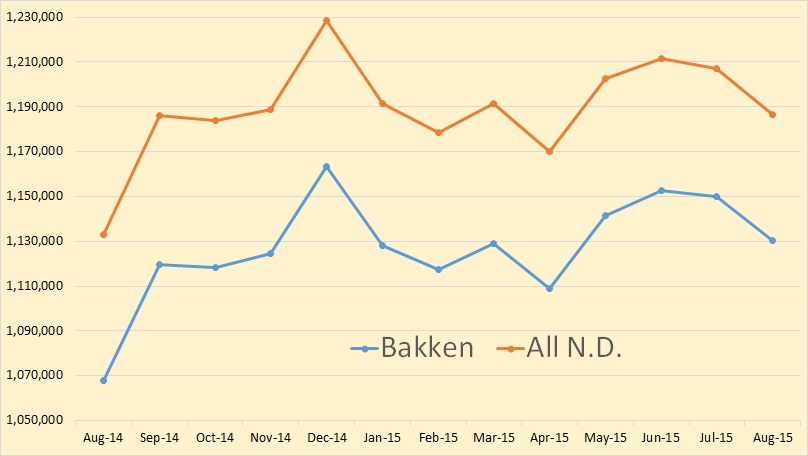

Here is an amplified chart of Bakken and all North Dakota production.

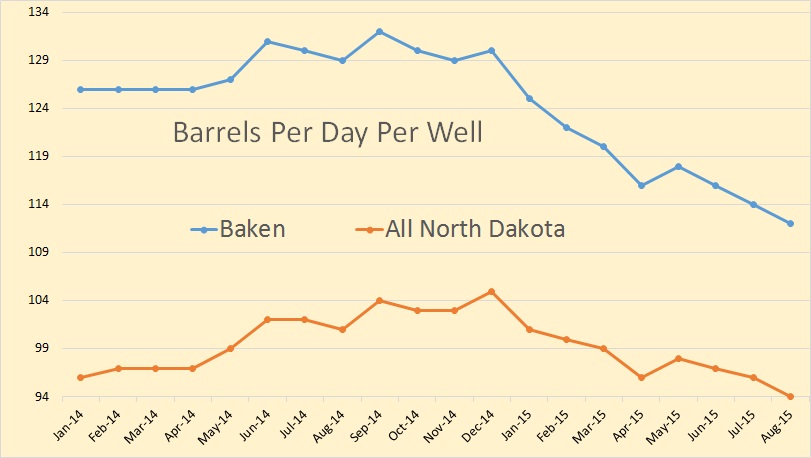

Bakken barrels per well per day is now 112 while all North Dakota gets 94 barrels per well per day.

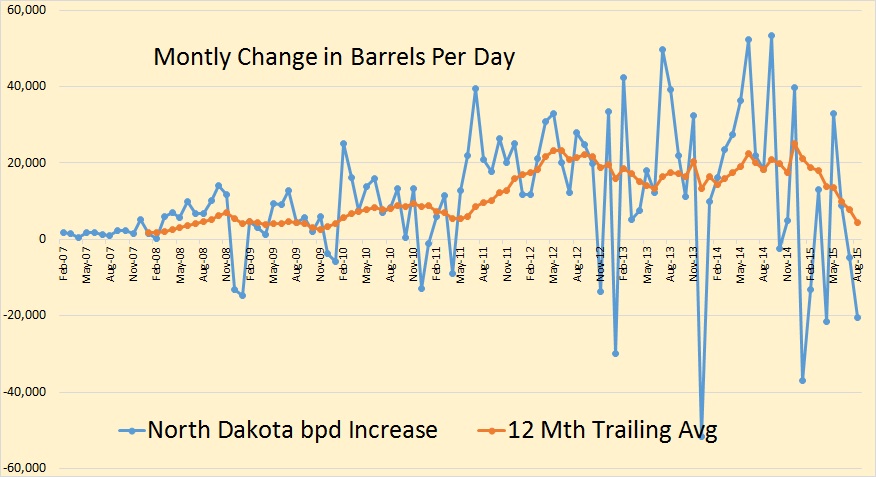

This chart shows the monthly change in North Dakota production. It is likely that by next month the 12 month average change in production will be negative.

Bakken wells producing increased by 69 and ND wells producing increased by 65.

From the Director’s Cut

July Permitting: 233 drilling and 0 seismic

Aug Permitting: 153 drilling and 1 seismic

Sep Permitting: 154 drilling and 1 seismic

July Sweet Crude Price1 = $39.41/barrel

Aug Sweet Crude Price = $29.52/barrel

Sep Sweet Crude Price = $31.17/barrel

Today’s Sweet Crude Price = $35.00/barrel

(low-point since Bakken play began was $22.00 in Dec 2008)

(all-time high was $136.29 7/3/2008)

July rig count 73

Aug rig count 74

Sep rig count 71

Today’s rig count is 67

(in November 2009 it was 63)(all-time high was 218 on 5/29/2012)

Comments: The drilling rig count increased 1 from July to August, decreased 3 from August to September, and dropped 4 more this month. Operators are now committed to running fewer rigs than their planned 2015 minimum as drill times and efficiencies continue to improve and oil prices continue to fall. This has resulted in a current active drilling rig count of 10 to 15 rigs below what operators indicated would be their 2015 average if oil price remained below $65/barrel. The number of well completions fell from 119(final) in July to 115(preliminary) in August. Oil price weakness now anticipated to last well into next year is the main reason for the continued slow-down. There was one significant precipitation event in the Minot area, 6 days with wind speeds in excess of 35 mph (too high for completion work), and no days with temperatures below -10F.

Over 98% of drilling now targets the Bakken and Three Forks formations. At the end of August there were an estimated 993 wells2 waiting on completion services, 79 more than at the end of July.

The drop in oil price associated with anticipation of lifting sanctions on Iran and a weaker economy in China is leading to further cuts in the drilling rig count. Utilization rate for rigs capable of 20,000+ feet is about 40% and for shallow well rigs (7,000 feet or less) about 20%.

Drilling permit activity decreased sharply from July to August but stabilized from August to September as operators continued to position themselves for low 2016 price scenarios. Operators already have a significant permit inventory should a return to the drilling price point occur in the next 12 months.

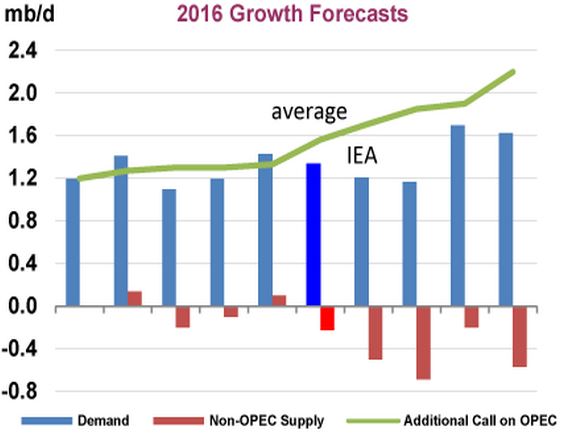

Highlights of IEA Oil Market Report had an interesting chart this month.

This is a chart of nine different demand growth and production forecasts, sorted left to right on the amount of shortfall in Non-OPEC production. Or, to put it another way, it is sorted on the amount OPEC will have to increase production to keep supply and demand in balance.

The IEA says demand will increase by 1.2 mb/d while Non-OPEC supply falls by .5 mb/d meaning the “call on OPEC” will be to increase production by 1.7 mb/d. The most optimistic prediction says the “call on OPEC” will be only 1.2 mb/d while the most pessimistic prediction says the “call on OPEC” will be 2.3 mb/d.

If the article below has any validity then the decline in Non-OPEC production will be a whole lot more than any of the nine prognosticators are predicting.

Offshore oil output to plunge as producers scrap field upgrades

(Reuters) – Global offshore oil production in ageing fields will fall by 10 percent next year as producers abandon field upgrades at the fastest rate in 30 years, in the first clear sign of output cuts outside the U.S. shale industry, exclusive data shows.

A drop in oil prices to half the level of a year ago has forced producers to slash spending and scrap mega projects that can take up to a decade to develop, but they are also taking less visible steps to cut investment in existing fields that will have an immediate impact on global supplies.

There have been few signs of how cost cuts of around $180 billion will impact near-term production until now. They could erode the glut that has forced down prices, and help balance global production and demand by the middle of next year or earlier, Oslo-based oil consultancy Rystad Energy said.

Data provided exclusively to Reuters by Rystad show a sharp decline in investment to upgrade mature offshore oil fields in order to arrest their natural decline, in what is known as infill drilling.

In three major offshore basins — the Gulf of Mexico, Southeast Asia and Brazil — infill drilling dropped by 60 percent between January and July this year compared with the same period last year, according to the Rystad Oil Market Trend Report, whose data is based on company data and regulatory filings.

The drop dramatically exceeds previous downturns in infill drilling going back to 1986, the data shows.

For example, according to the data, in the Gulf of Mexico, infill drilling on mature wells dropped from 149 wells between January and July 2014 to a total of 61 wells during the same period this year.

Based on this trend, Rystad Energy estimates that global offshore oil production in mature field will decline next year by 1.5 million barrels per day (bpd), or 10 percent, to 13.5 million bpd from 15 million bpd in 2015.

10 Comments on "Bakken Production Down plus IEA Predictions"

JN2 on Wed, 14th Oct 2015 7:36 am

Essentially flat since September last year. Robert Rapier’s “undulating plateau”? We’ll see…

BobInget on Wed, 14th Oct 2015 8:43 am

Letter from the Bakken;

Bakken and Powder River Basin Update – some quick thoughts

I was in Casper all day today and talking to some of the guys at the Petroleum Club and a few others as I made my rounds. it’s beginning to look more ugly than even I could have imagined. Unless we see a quick and sustained rebound in prices the rig counts will drop hard and fast. i talked with a couple of the partners on our Bakken wells and our Wyoming Powder River Basin holdings. We re holding on by the skin of our teeth. Not sure we will make it but so far we still have cash reserves. Seems a lot of hedges are starting to come off the books and we will see credit lines pulled (if not done already) and some projects shelved and yet more rigs laid down.

Another old contact I met at his office who runs a couple wellsite geologist crews said that logging companies are undercutting each other and the going rate dropped from over $2200/day to just under $1000/day for a two mn logging crew and for the equipment. Obviously the crews will be taking huge day rate cuts. Many geologists are going contract so the companies don’t have to pay for benefits such as medical, 401K, etc. It’s dog-eat-dog in the patch now. Even not this bad in the 1980s. At least we saw some light at the end of the tunnel. One friend in management at a large energy service company said that they expected a “V” shaped recovery, then a “U” shaped recovery and now they are talking an “L” shaped funk with low price long term.

Anyway, that the buzz from the energy patch as seen by the guys in Casper. Gonna get mighty interesting in the next few weeks.

– Black Blade

Following is BB’s response to another question:

I work in the U.S. On the service side. We saw some rig count deterioration, about 10%, in the weeks leading up to and after end of Q3. What order of magnitude are you thinking for further rig reductions do you see coming this quarter? the service side of this business is just getting worse and worse. Companies giving away what were premium services for “free” if the Operator will select them as the contractor. Office staffs have been reduced to bones. Hardly anyone left in HSE or Service Quality type positions. Gas plays just as bad, if not worse than oil too BTW…

Sounds like you see the same thing. I actually thing Bakken rig counts will fall to the mid 40s to low 50s range. I am just amazed it hasn’t already collapsed by now. I didn’t want to push it as I talked to my friends in management but they are making a new list for layoffs later this week and into next. I was gonna call some contacts up north but will hold off now as I don’t think they know exactly how many of them will be on the chopping block. I really feel for them as I have many friends who will be badly hurt. Already know of one divorce due to money issues and job loss. I suspect there will be many more. Really though, I saw dozens of new subdivisions being built and apartments and condos under construction – now the contractors and banks will be left holding the bag. Looks very grim.

– Black Blade

BobInget on Wed, 14th Oct 2015 8:48 am

It’s as if NA producer’s and consumers are being led into ambush canyon.

Combine this forced decline with Russia’s, Iran’s

Iraq’s determination to raise oil prices and we have some serious economy killing shortages looking ahead.

Inget

BobInget on Wed, 14th Oct 2015 8:54 am

Another analyst reports.

I added another column for the average 24 test of Completed Non Confidential wells. This should provide a correlation to the quality of the wells being brought on. I started tracking this in May and it appears to have peaked in August Declined in September and has dropped dramatically so far in October.

August’s drop in production of approximately 20,000 bbls a day is not bad considering that the well count grew by only 69. This does happen to coincide with some very good test results for August (1,609 BOD average for 67 non confidential wells reported via the Dailies).

Based on this analysis it would appear that backlog of uncompleted wells grew by about 57 (Comparing wells placed on line to spuds for the month).

September and October could be challenging months for production figures based on the drop in completion test results. The drop is likely due to 1)deferred completions, 2)Completion of older wells that were not drilled in sweet spots as they reach their time limits, 3)running out of sweet spots, 4)lower quality sweet spots, 5)interference due to continued down spacing and in fill drilling, 6) choking wells back

Time will tell, but the time of ever increasing productivity appears to at least paused. For now it is not clear what the main drivers are. Numbers 3, 4, and 5 would be cause for concern. Over time we should get more clarity as to what is happening.

Will the Bakken continue to reign as Champ? Or is it headed to Palookaville?

buddavis on Wed, 14th Oct 2015 9:52 am

Question

At this rate of new wells per month, when will the backlog of wells be brought online, so there are none waiting on completion? They have one year from TD to complete, is this correct?

Or will we just see a significant percentage of wells drilled and waiting on completion, hoping prices tick up in the year they have to complete?

rockman on Wed, 14th Oct 2015 11:34 am

I don’t know about the Bakken but I suspect it’s not very different then the Eagle Ford. Yes: there’s a back log of EFS wells waiting for frac’ng/completion. But there was a 6+ month back log when oil was $100/bbl.

Despite press releases from just a few companies I haven’t spoken to one Texas operator that isn’t busting there ass to get wells on as fast as possible. And that includes the ones that aren’t producing their wells at max rate. Cash flow is still King even if it isn’t maximized.

buddavis on Wed, 14th Oct 2015 12:56 pm

I agree, but my understanding for the backlog was the relative shortage of frac crews. I would think that at some point the backlog starts to dwindle.

BC on Wed, 14th Oct 2015 2:07 pm

https://research.stlouisfed.org/fred2/graph/fredgraph.png?g=28MQ

https://research.stlouisfed.org/fred2/graph/fredgraph.png?g=28MA

https://research.stlouisfed.org/fred2/graph/fredgraph.png?g=28MZ

Bob, WRT BB, TX, ND, and WY are in recession.

coffeeguyzz on Wed, 14th Oct 2015 4:04 pm

Buddavis

The three man ND commission has indicated that they will waive the 12 month time frame in which wells must be brought online (or plugged) after spud date.

The number of DUCs in the Bakken is close to double its norm for the past few years (although Enno has a chart showing the number quite a bit higher).

EOG said a few weeks back that they currently have just under 300 wells drilled but not frac’d and they expect that number to increase to 325 by year end.

As a side note, EOG has just started in the Bakken completions that they call ‘high density’. These were introduced in the EF last summer wherein they use massive amounts of water and sand.

The first Bakken well frac’d this way, the Riverview 102-32H was the highest producing Bakken well in its first full month’s production – 87,531 barrels.

This lateral was only 4,300 ‘ long

rockman on Thu, 15th Oct 2015 7:32 am

bud – I’m not sure availability isn’t even wosre now then during the boom. I’m having difficulty getting increased services from a variety of companies. I just had Baker Hughes drop out of bidding for two projects (one being a small frac job) because they lack the capability in this area that they had just a few months ago. I’m stuck with one company for the frac: Halliburton. And that’s taken a bit over a month to schedule and I’m still having trouble lining up other services (like the frac tree) for that project. I had one company turn down the bid for the frac tree because the closest one they had to Mississippi was OK: too far to drive.

Remember the latest count I’ve seen is 150,000 laid off: there might be dozens of frac trucks sitting in yards collecting dust. And they’ll continue to rust away as long as there aren’t crews to run them. A frac truck sitting in a yard costs a company very little. Paying 100 hands to just drink coffee while waiting for a project does. Eliminating staff has always been the primary savings approach during a bust.