Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on February 12, 2015

Peak Nothing. Goldman Sachs Advisor Says “Too Much Physical Oil”

Goldman Sachs executive Gary Cohn says we could see so much oil, there would be no way to physically store it all, resulting in falling prices, at least in certain locational areas.

Further destabilization across the globe could, logically, follow.

Cohn told Bloomberg News:

“I think the oil market is trying to figure out an equilibrium price. The danger here, as we try and find an equilibrium price, at some point

we may end up in a situation where storage capacity gets very, very limited. We may have too much physical oil for the available storage in certain locations. And it may be a locational issue.”“And you may just see lots of oil in certain locations around the world where oil will have to price to such a cheap discount vis-a-vis the forward price that you make second tier, and third tier and fourth tier storage available.”

[…] “You could see the price fall relatively quickly to make that storage work in the market.”

And though prices have recently rebounded a bit, that could well mean prices below the $50 per barrel low point that has already shaken the foundation of the geopolitical structure, sending the ruble and other currencies into chaos while threatening new drilling operations and job bases in the United States.

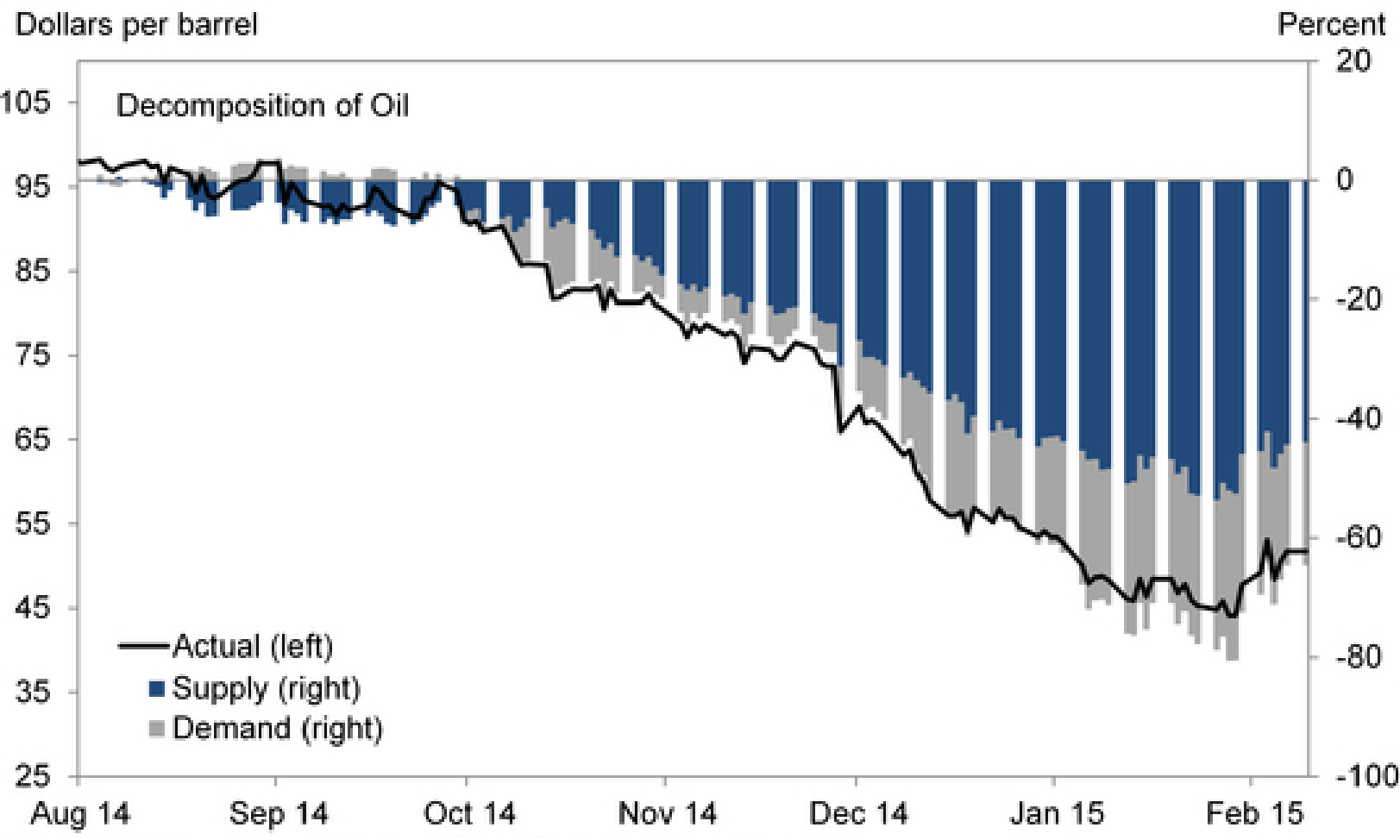

The big culprit in the oil crash has been an abundance of oil flooding the market. A massive supply shock in the second half of last year accounted for most of the decline. In December and January, slowing demand contributed to the continued sell-off. Goldman was able to quantify these effects.

The big take-away: “[T]he decline in oil has been driven by an oversupplied global oil market,” wrote Goldman economist Sven Jari Stehn. As a result, “the new equilibrium price of oil will likely be much lower than over the past decade.”

Here’s a chart to put it into pictures:

So much for peak oil, sold to the public since at least the 1970s to justify tighter supply controls and soaring prices.

Today, it is revealed as something much closer to economic warfare between competing producers, and market manipulation on the global market, in part to provide the backbone for the American petrodollar.

Back in December 2014, the Wall Street Journal wrote in a piece titled, ‘Peak Oil’ Debunked, Again:

The latest reckoning with reality is the end of the obsession with “peak oil,” which for years had serious people proclaiming that we were entering an era of permanent fossil fuels scarcity. It didn’t work out that way.

That’s a central lesson from this year’s dramatic fall in the price of oil, which reached $69.49 a barrel of Brent crude on Thursday from a June high of $112.12. As recently as early November, when oil hovered at $80, OPEC officials warned they would intervene to hold the price at $70. But Saudi officials conspicuously refused to support an output cut at last week’s OPEC meeting, and Saudi oil minister Ali al-Naimi has made clear that he’d be comfortable with lower prices.

The short-term Saudi calculation is to drive oil prices down to squeeze their geopolitical adversaries and higher-cost producers. That goes especially for their adversaries across the Persian Gulf in Iran, which depends on oil exports for over 40% of its revenues, and where the regime had designed its budget based on $100 oil.

The Saudis also hope to slow the explosive growth of U.S. production, which, thanks to the tapping of domestic shale resources through the combination of horizontal drilling and hydraulic fracturing, has risen to some nine million barrels a day from five million in 2008. By some estimates, the price of oil needs to be as high as $90 a barrel for oil extracted from “tight” deposits such as shale, though oil market research firm IHS believes most tight oil wells have a break-even cost of between $50 and $69 dollars a barrel.

Ahead of that story, SHTF warned back in December how falling oil price were being used to ‘cripple’ Russia and push Putin into a posture for war, possibly escalating WWIII.

The Cold War 2.0 is going hot, and while it may someday be fought with planes, tanks, guns and bombs, the first front is being fought with oil and shale gas.

The U.S. and European sanctions against Russia will become more severe and crippling in the face of drastically falling oil prices – prices which are falling drastically because of the unprecedented boom of shale gas fracking both domestically in the U.S. and abroad in Ukraine and other locales. The oil & gas giants like Chevron and Exxon Mobil have created revolutionary conditions with now direct consequences on U.S. foreign policy and global war for dominance. Via Bloomberg:

Oil’s decline is proving to be the worst since the collapse of the financial system in 2008 and threatening to have the same global impact of falling prices three decades ago that led to the Mexican debt crisis and the end of the Soviet Union.

Russia, the world’s largest producer, can no longer rely on the same oil revenues to rescue an economy suffering from European and U.S. sanctions. Iran, also reeling from similar sanctions, will need to reduce subsidies that have partly insulated its growing population. Nigeria, fighting an Islamic insurgency, and Venezuela, crippled by failing political and economic policies, also rank among the biggest losers from the decision by the Organization of Petroleum Exporting Countries last week to let the force of the market determine what some experts say will be the first free-fall in decades.

“This is a big shock in Caracas, it’s a shock in Tehran, it’s a shock in Abuja,” said Daniel Yergin…

The destabilization in Ukraine and numerous spots in the Middle East – including the ISIS-threatened Iraq and Syria – have been mere preludes to what is coming.

How close are we today to that scenario?

24 Comments on "Peak Nothing. Goldman Sachs Advisor Says “Too Much Physical Oil”"

Plantagenet on Thu, 12th Feb 2015 8:48 pm

The oil glut is affecting every country on earth. It’s not targeted at anyone—- the collapse of the price is just an economic reality that we’ll all have to deal with

Tom on Thu, 12th Feb 2015 9:01 pm

We sure don’t have an oil glut because the previously prevailing price was $50/barrel. At $100/barrel, it seems obvious that a whole lot of consumers can’t afford as much oil as earlier in the game. If the current “oil gut” prices are sustained for some time, we may get the chance to see if peak oil (i.e the total hodge podge that is now called oil) has arrived on the scene. The oil service companies and drillers are laying off massive numbers of workers. If the drilling slow down lasts for long, new oil won’t be forthcoming. So why is this idiot from Goldman Sachs so sure that the oil glut and cheap oil prices will continue into some indefinite future? Maybe it has something to do with minimizing GS’s losses from bad fracking investments or in how they are playing the futures market. Make a sucker out of the investing public while making off with the money?

bobinget on Thu, 12th Feb 2015 9:53 pm

Goldman, obviously, ‘talking their book’ .IOW’s

Goldman is strenuously taking the podium to protect massive short positions.

Just about everything Goldman says (about the current oil market is a ‘pants on fire lie’.

1) the unexpected double cross;

KUWAIT, 13 hours, 6 minutes ago

Bad weather has disrupted oil exports from Kuwait forcing it to halt both its crude and oil products exports, a spokesman for state-run Kuwait National Petroleum Co (KNPC) told Reuters.

The suspension will remain until further notice when the weather conditions improve, spokesman Khalid Al Asousi said.

The Gulf Opec member produces around 3 million barrels of crude per day. It has three refineries, Shuaiba, Mina Abdullah and Mina al-Ahmadi, with a total refining capacity of around 930,000 bpd.–Reuters

2) The “Glut”

So Iraq is off 400,000 BPD (+-) since December. Libya is off 150,000 BPD. Nigeria is off 200,000 BPD. That is 750,000 BOPD give or take. If Saudi would have cut 1,000,000 BOPD where would oil price be today? (Venezuelan imports lower)

3) Alleged by Goldman there is little or no more US storage:

http://www.reuters.com/article/2015/01/12/us-oil-tanks-analysis-idUSKBN0KL0AZ20150112

excerpt:

s a result, those onshore tanks are barely a third full, with less than 150 million barrels of the nation’s total 439 million barrels of shell storage capacity occupied as recently as October, according to a Reuters analysis of U.S. data. That’s by far the highest vacancy rate since the Energy Information Administration began a bi-annual survey of tank farm capacity — which exclude refinery stocks and oil in pipelines – in 2010.

4) Is Goldman shorting oil?

http://www.zerohedge.com/news/2014-10-27/wti-crude-tumbles-under-80-following-goldman-downgrade

4.5) http://pesn.com/2010/05/05/9501645_No_joke–Goldman_Sachs_shorted_TransOcean/

4.6) http://www.businessinsider.com/goldman-sachs-stocks-hedge-funds-short-2014-11

https://books.google.com/books?id=BRysaKZtNLkC&pg=PA217&lpg=PA217&dq=is+Goldman+Sachs+shorting+oil?&source=bl&ots=b8hw3qmxRO&sig=kwUXJF7G2P3HCDW86wWWfqpp1Lc&hl=en&sa=X&ei=sXLdVK2FONK3ogSo54LYCw&ved=0CDcQ6AEwAjgK#v=onepage&q=is%20Goldman%20Sachs%20shorting%20oil%3F&f=false

5) Biggest lie of all, “world slowdown in oil consumption” (GROWTH slowed a few basis points NOT actual consumption) In fact IEA projects

92.37 Million B p/d world consumption for 2015.

about 1.9 million barrels OVER 2014. With oil prices so low I’ll bet anyone here we exceed 92 Million B’s.

Every week EIA is showing good percentages higher then last year this time.

6) AS oil price move higher watch Goldman’s dour predictions become even louder and shriller. .

gdubya on Fri, 13th Feb 2015 12:24 am

I think we have determined that the amount of oil is sufficient to destroy the ecosphere. I’m not sure why some people think this is good news.

GregT on Fri, 13th Feb 2015 1:21 am

Three very intelligent and considerate comments guys.

Makati1 on Fri, 13th Feb 2015 5:12 am

Related…

http://libertyblitzkrieg.com/2015/02/12/u-s-falls-again-in-world-press-freedom-index-now-ranked-49-globally/

http://charleshughsmith.blogspot.jp/2015/02/empire-of-lies.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed:+google/RzFQ+%28oftwominds%29

The Imperial Ministry of Propaganda at work.

Makati1 on Fri, 13th Feb 2015 5:14 am

Plant, you are correct. Those countries that do not export oil can now buy it much cheaper and benefit from the other’s pain.

Ralph on Fri, 13th Feb 2015 5:17 am

Brent back over $60. Will we still have

a glut at $70? $80?

Go Speed Racer. on Fri, 13th Feb 2015 5:22 am

Hell ya, unlimited cheap free oil, and we will never run out. Send your Prius to the crusher. Buy an F-350 and drive it to Texas with nothing in the back. Buy an Escalade. Back up into the driver’s door of a Smart car. We will never run out of oil, a banker at GS told me so. And Fox News, Rush Limbaugh, and the pastor at my church said it too.

rockman on Fri, 13th Feb 2015 6:21 am

M – “Those countries that do not export oil can now buy it much cheaper and benefit from the other’s pain.” You unsympathetic bastard!!! You really can’t appreciate the suffering I’m going thru today selling my oil for just 60% more than I was about 10 years ago. LOL.

Davy on Fri, 13th Feb 2015 6:56 am

Adjustment to the Mak agenda:

http://en.rsf.org/press-freedom-index-2013,1054.html

In Eastern Europe, Russia (148th, -6) has fallen again because, since Vladimir Putin’s return to the presidency, repression has been stepped up in response to an unprecedented wave of opposition protests. The country also continues to be marked by the unacceptable failure to punish all those who have murdered or attacked journalists

For the second year running, the bottom three countries are immediately preceded by Syria (176th, 0), where a deadly information war is being waged, and Somalia (175th, -11), which has had a deadly year for journalists. Iran (174th, +1), China (173rd, +1), Vietnam (172nd, 0),

Ralph on Fri, 13th Feb 2015 7:08 am

Brent WTI spread back to $8. Oil storage in the US is brimming full. Drilling rigs are falling like dominoes. Yet USA is IMPORTING nearly 7 million barrels of OIL a day. So what is in all that storage?

Condensate.

The USA has a glut of condensate. The world is past the all time peak of crude OIL production.

westexas on Fri, 13th Feb 2015 7:31 am

Mexico’s Pemex aims to start importing light crude this year (2014)

http://uk.reuters.com/article/2014/08/28/mexico-pemex-idUKL1N0QX2TL20140828

Aug 28 (Reuters) – Mexican state-owned oil company Pemex wants to launch light crude oil imports later this year, potentially reaching up to 70,000 barrels per day (bpd) and aimed at boosting refinery output, the head of its commercial arm said.

The imports would mark an abrupt shift from a decades-old devotion to crude oil self-sufficiency in Mexico, long a major exporter to the United States. It also comes after a sweeping energy sector overhaul which seeks to reverse many years of declining output and export volumes.

“Our objective is that (crude imports) will begin this year,” said Jose Manuel Carrera, chief executive officer of PMI Comercio Internacional, Pemex’s oil trading arm. His comments are the strongest signals to date on both the timing and potential volumes of light crude imports to Mexico. . . .

While U.S. companies Pioneer Natural Resources and Enterprise Products Partners have secured permission to ship a type of ultralight oil known as condensate to foreign buyers, Carrera all but ruled out the possibility.

“Condensate is not necessarily what Mexico needs. It needs crude,” he said.

shortonoil on Fri, 13th Feb 2015 8:06 am

“Condensate.”

You hit that nail right on the head with that one. 37% (1.2 mb/d) of LTO has an API of over 50, and that stuff does not make transportation fuels. That is why the US is still importing huge amounts of foreign crude, and storage is constantly building. There is no market for much of what the shale industry produces.

In an attempt to understand this on going phenomena, of how the shale industry can even exist, we are attempting to look at the debt to production numbers. Our conclusions are preliminary because the entire shale debt structure is lumped into one big pile. NG, condensate, and oil have been included together. But our early figures, which are likely to be revised, put the debt formation since 2008, on a boe bases, at $347 per barrel. Or stated otherwise, it has required $347 of debt formation to produce one boe.

This corresponds closely with our thermodynamic analysis of shale production that indicates that the average shale production well hits the “dead state” in less than eight months. This entire fiasco appears to be one of the largest misappropriations of capital in history. It makes the construction of Chinese ghost cities look like the efforts of the gold mining industry.

We will continue attempting to unravel the reports of various sources to get a more accurate determination of the situation, and we will keep you posted.

http://www.thehillsgroup.org/

gamilon on Fri, 13th Feb 2015 8:44 am

Great comments on the condensate issue, everyone. I haven’t seen any reporting on it in the MSM, and I think it is key to unwinding what is going on with storage and price. Is WTI$ being unfairly punished based on US production/storage numbers that include condensate when WTI is supposed to represent oil usable for fuel?

Makati1 on Fri, 13th Feb 2015 9:11 am

Rock, I have no control over oil. I can only see the plus and minus. There is always a winner and a loser. I suspect that you are intelligent enough to have seen the future and are prepared. I am happy that the 3rd world can afford a few more plus’ while the 1st world has to cut their wasteful habits. I am just a spectator that finds world events more interesting than the mind slop on TV.

shortonoil on Fri, 13th Feb 2015 9:13 am

Is WTI$ being unfairly punished based on US production/storage numbers that include condensate when WTI is supposed to represent oil usable for fuel?

By our calculations it seems to be so by about $25/barrel:

http://www.thehillsgroup.org/depletion2_022.htm

Of course this does not bode well for future reserve development. Capex has already taken a serious hit because of the price crisis. This is likely to put significant pressure on supply a few years from now. A few years from now, however, is completely off the MSM radar. They are not going to inform the public that cheap gas prices today translates into something very ugly tomorrow. That just doesn’t fit into their play book that everything is, and always will be OK. The MSM has a concentration span that is about the same as the general public; the length of one football game!

http://www.thehillsgroup.org/

Plantagenet on Fri, 13th Feb 2015 9:48 am

Its stupid for Mexico to be importing oil. The Eagle Ford shale play underlies NE Mexico. All the Mexicans have to do is drill and frack and they could start exporting oil again

westexas on Fri, 13th Feb 2015 10:18 am

Plant,

Mexico remains (for the time being) a net oil exporter, but they no longer have sufficient light/sweet crude oil production to meet their domestic refinery demand (for light/sweet feedstock).

marmico on Fri, 13th Feb 2015 10:25 am

Once [Cushing is] full, the market will puke, said one trader.

Ralph on Fri, 13th Feb 2015 10:51 am

Once Cushing is full, the US shale market will puke.

The rest of the world, less so.

shallowsand on Fri, 13th Feb 2015 10:56 am

RBOB Unleaded has bounced from low of 1.23 to 1.62. Wonder if it would fall with crude, in the event crude storage issues caused price to crater into 30s or 20s like GS and CITI are hoping? Looks like pickup in gasoline demand could cause its price to not go back to lows, even if crude were to touch new lows. That appears especially true if crude bottom occurs in May or later, due to seasonal demand pick up. Field day for refiners?

shallowsand on Fri, 13th Feb 2015 11:06 am

Also note that WTI Brent spread has widened from almost nil to $8.5 per bbl. KSA has to be loving that. Inability to export our large inventory of ultra light, our refiners still need the heavier OPEC basket grades, could lead to continued low WTI price, but higher US gasoline prices.

Remember WTI Brent spread has been $20-$30 for significant periods of time. Wouldn’t that be a heck of a deal? Gasoline back to $3, Brent at $85, WTI at $55, still stifling most shale, but OPEC “back in the saddle again”?

rockman on Fri, 13th Feb 2015 11:06 am

M – I hope we’re not having a language problem and you understand I was just teasing with you. The point was that while oil producers are making a lot less money then they were last year we’re still making a lot more revenue from the same production then we were 8 years ago.