America: You’ve got three more years to drive normally! – Part 2

Part 1 of this series stirred up a lot of interest with Rag Blog readers, and it was reposted by Resilience.org where it was also popular. I imagine the article’s somewhat alarming title struck a nerve, calling attention to the repressed fears that challenge our suburban, car-centric American culture. Fears that stem from our culture of denial in response to business as usual.

In Part 2 we will further explore the constraints on our energy resources and will look at the role of finance capital in perpetuating our denial; denial that inhibits energy reform until there is a full blown crisis.

The context of our driving problem

As a nation we know that something is deeply wrong, starting with a politically gridlocked congress. The recent march against climate change underlined this high level of public concern.

Arguably the top issue of our times has become how long our physically expansive system of global finance capital can maintain profitable growth without wrecking the global environment. In this respect, public attention to global warming has become the leading example.

Business as usual justifies its legitimacy by maintaining that at least some plausibly improved version of our system can pay off its immense deficit of public and private debt by growing profitably forever. And can do so in a finite world that is clearly already struggling to deal with a human population of 7 billion. There is now a wealth of solid scientific research and useful information that shows that this goal is impossible; information easily available from a growing assortment of environmental awareness sites like the

Post Carbon Institute.

Expansionist economic control and free market fundamentalism have become like a state religion.

Expansionist economic control and free market fundamentalism have become like a state religion uniting politics and economics in support of corporate domination. In accord with this point of view, it comes as no surprise to see Paul Krugman, a liberal Keynesian advocate of a gentler greener kind of capitalist economics, blame the Post Carbon Institute for teaching about natural limits to economic growth.

This

recent exchange features Krugman as an economic expansionist, and Richard Heinberg, in response, laying out conflicting positions on the growth issue. Nobel economics prize winner Krugman seems to have blundered into an uphill debate against top scientists and their intellectual allies.

Now, with the help of recent geological data, we can see that peak oil will probably soon limit and affect an important aspect of American life, namely our driving. The global oil supply situation will probably only permit about three more years of easily affordable driving. So far we have been able mostly to ignore this problem, which has been nipping at our heels for most of the past decade by more than tripling oil prices.

Follow the oil

Oil, when burned, has the unique ability to supply the motive muscle power needed throughout our global civilization. The power to move stuff around; to physically expand global trade by powering nearly all the world’s ships, planes, trucks, and trains. The

Hirsch report laid out the difficulty of an economic transition away from oil about a decade ago, by predicting the need for about 20 years to properly prepare for peak oil. Everyone has become fond of solar panels these days, but there has not been nearly enough progress towards alternatives since conventional oil peaked in 2005, given the true scale of the problem.

Peak oil is here, or close enough for us to be able to sketch out important details.

Peak oil is here, or close enough for us to be able to sketch out important details. The current world oil glut is genuine, and we need to try to see why this situation is actually quite compatible with a globally peaking oil supply. We can closely examine the considerable body of evidence that suggests about three more years of easy driving. Anyone can study the same evidence and attempt a more optimistic interpretation.

Thanks to what could be seen as the increasingly disruptive side effects of maintaining our globally oil-dependent economy, we face unpredictable problems that could interfere with normal driving even sooner than three years.

Having made a horrible mess of Iraq, we now see rising conflict throughout the Middle East, largely as a result of an old agreement with the Saudis after the 1970s energy crisis. An agreement to maintain through military force the stable production and export of OPEC oil on the world marketplace. A second looming threat stems from the fact that the global economy was thoroughly disrupted by a severe oil price spike in 2008 and has not recovered. The world of finance capital has been kept solvent since then through transfusions of publicly funded credit, such as quantitative easing and low interest rates.

It is no accident that we sometimes call our dollars petrodollars. The British pound may have been backed by gold, but now our dollar is backed by its singular ability to buy oil and its combustion-derived mobile power on the global market. Oil is only globally traded in dollars, which are also the world’s standard reserve currency.

Our dollar-based global economy, led by finance capital centered in Wall Street and London, has managed to function successfully since WWII, but, distressingly, it is beginning to resemble an oil-addictive dollar-based global Ponzi scheme, sure to fail without an exponential growth in profit.”

The technical advance that is keeping the USA driving affordably, for now at least, is hydrofracturing or fracking, used to produce tight gas and oil from shale deposits. This U.S. fracking boom is now adding more than 3 million barrels of tight oil and closely associated liquid condensate fuel each day. This is enough new product that, when it is added to the world’s slowly declining conventional oil production, the resulting in obscuring and delaying the onset of the peak oil problem, if only for a few years.

For the moment, there is a global oil glut and a falling price due to an unusually weak global customer demand for the relatively constant stream of oil being produced and consumed globally, but that does not mean that this product is being produced at a profit. Over the short run, shifting consumer demand due to the economy or freezing weather conditions can have a much bigger faster effect on price than investment in new production, which is slow, and risky at best.

As a whole, domestic oil and gas from fracking is beginning to look like an investment bubble.

As a whole, domestic oil and gas from fracking is beginning to look like an investment bubble. U.S. production of tight oil by fracking can probably only increase and postpone another global oil price spike for a few years. Even if the current fracking boom should somehow give us five more years, it doesn’t change the picture much. Driving will get less affordable because of fuel, and there will be a painfully short amount of time to prepare. Gasoline-powered cars are expensive and last for more than a decade, and the USA doesn’t have any good mobility alternative to serve its suburbs.

As we saw in

Part 1, trying to convince the U.S. public that they might have a problem driving about three years from now is going to be a hard sell. Who is the driving public to believe, those who warn them about a problem a years from now, or their own eyes? This is especially true since anyone who fills up at the gas pump can see for themselves that gasoline has been getting a bit cheaper lately.

For now, oil and its products remain a buyer’s market. Here we see the

Wall Street Journal telling us that the reason that gas prices are going down is because of a

glut of gasoline.

A global glut of crude oil is the main driver behind the decline in gasoline prices. Relatively cheap oil has made it more profitable for refiners to produce gasoline and other fuels, and they have ramped up production to record levels. This boom in supplies has sent gasoline prices tumbling. Traders and other market observers expect the flow of both crude oil and gasoline to keep rising, likely exerting more downward pressure on prices.

We are now at the doorstep of globally peaking oil

When I say that Americans will probably have trouble driving in only three years, this means that I think another oil price shock causing widespread public driving anxiety is quite likely by then. It could be less than three years; James Howard Kunstler

gives us two years for reasons similar to mine.

Wait until they discover that the shale oil producers have never made a buck producing shale oil, only on the sale of leases and real estate to “greater fools” and creaming off the froth of the complex junk financing deals behind their exertions. Expect that mirage to dissipate in the next 24 months, perhaps sooner if the price of oil keeps sinking toward the sub $90-a-barrel level, where there’s no economically rational reason to bother drilling and fracking.

Gasoline is cheap for now only because oil production is relatively constant and the oil must be sold at whatever price the global market can bear, even during a time of global deflation due to the lingering effect of the 2008 oil price shock.

The estimate of three more years of easily affordable driving is an educated guess, based on looking at the work of a number of expert forecasters and analysts who predict that the global oil market will run out of profitable U.S. fracking plays in about this time. After another oil price spike we’re back to a bad recession like 2009, but this time with even less of the oil needed to recover.

The price of oil has a complex and partly hidden effect on the economy.

The price of oil has a complex and partly hidden effect on the economy. Since cheap conventional oil globally peaked in 2005, the higher price of fuel has acted like a slowly increasing but hidden tax on almost everything sold, since almost everything sold has some rising oil price costs embedded in its sales price. People cut back on discretionary spending in order to pay more for gas, which sent those sectors into recession. A hidden oil tax tends in this way to cause the pervasive economic stagnation we now see.

A rapid oil price spike is a much more politically visible target than the general stagnation effect of high energy prices, since an oil price spike leads to higher fuel and food costs fairly quickly. These two impacts of high oil prices, one faster and one slower, generate different types of political and economic responses.

Without an economic recovery, which is itself unlikely without cheap oil, another gasoline price spike to even $4 dollars a gallon might now cause a broad and angry public demand for Congress to do something fast, a sort of a political tipping point. A return to gasoline rationing,

like that used after the 1973 oil crisis, is one plausible way for politicians to try to ease the public’s driving pain.

Expert evidence for three more years of easily affordable driving

The estimate of three years of easily affordable driving depends primarily on estimating how long the current fracking boom, which is now holding down the global oil price, can be sustained. There seems to be almost a consensus, outside of government officialdom like the EIA, of maybe two or three more years.

Post Carbon Institute fellow and author Richard Heinberg has written an

exceptionally well-researched book, published in July 2013, titled

Snake Oil: How Fracking’s False Promise of Plenty Imperils our Future.

In

this interview, Heinberg reviews our energy situation; you can get a good idea where things stand just by listening to about the first 10 minutes. Following is a quote from

Heinberg’s recent writing: “Why Peak Oil Refuses to Die. ”

Let’s start with the common assertion that oil supplies are sufficiently abundant so that a peak in production is many years or decades away. Everyone agrees that planet Earth still holds plenty of petroleum or petroleum-like resources: that’s the kernel of truth at the heart of most attempted peak-oil debunkery. However, extracting and delivering those resources at an affordable price is becoming a bigger challenge year by year. For the oil industry, costs of production have rocketed; they’re currently soaring at a rate of about 10 percent annually. Producers need very high oil prices to justify going after the resources that remain—tight oil from source rocks, Arctic oil, ultra-deepwater oil, and bitumen. But oil prices have already risen to the point where many users of petroleum just can’t afford to pay more. The US economy has a habit of responding to oil price hikes by swooning into recession, and during the shift from $20 per barrel oil to $100 per barrel oil (which occurred between 2002 and 2011), the economies of most industrialized countries began to shudder and stall. What would be their response to a sustained oil price of $150 or $200? We may never know: it remains to be seen whether the world can afford to pay what will be required for oil producers to continue wresting liquid hydrocarbons from the ground at current rates.

Heinberg’s shale oil book is partly based on the work of a top Canadian resource geologist, David Hughes, who did a study of tight oil and gas economics for the Post Carbon Institute, titled “Drill Baby Drill.” The report can be downloaded

here. Basically what Hughes says is that there are only a few geographically large shale plays which contain within themselves much smaller sweet spots, those areas which are profitable when used to produce fairly high priced oil or gas. But these fracking wells tend to deplete rapidly, and the truly profitable sweet spots are being used up fast, implying that U.S. shale oil production

will peak about 2017.

Hughes explained that more than 80 percent of the nation’s shale oil comes from just two plays, the Bakken field in North Dakota and Montana and the Eagle Ford in Texas. He estimates that production in those regions will recede back to 2012 levels in 2019. Overall production across the nation’s shale oil fields will peak in 2017.

Readers who want to review and keep abreast of the evidence should become familiar with the peak oil blogs.

Readers who want to review and keep abreast of the evidence should become familiar with the peak oil blogs. Ron Patterson posts on

Peak oil barrel.

Crude Oil Peak is another excellent source Yet another is

Peak Oil News.

In

this article — “US shale oil growth covers up production drop in rest-of-world” — we see charts that tell us that that an increase in U.S. shale oil production is now the one factor that has kept otherwise declining global oil production increasing. Tight oil has been effectively obscuring the pricing signals that peaking oil in the rest of the world would give, as global oil need, if not ability to buy, continues to rise.

Here is what a top Saudi geologist, now in private practice as a consultant, had to offer in an interview with ASPO-USA earlier this year (“Ex-Saudi Aramco geologist Dr Husseini predicts oil price spikes of USD 140 by 2016-17: graphs”)

Husseini: My base oil price forecast in 2012 dollars still ranges between $105 and $120/barrel Brent with a volatility floor of $ 95/barrel and more probable upward spiking to $140/barrel within 2016/2017.

Dr. Husseini didn’t say how he predicted the oil price spike, but Crude oil Peak analyst Matt Mushalik comments on the Husseini interview. The last graphic predicts that rising demand will meet the falling production predicted by Dr. Husseini about 2016, and concludes as follows:

We see that the intersection point is somewhere in 2016. What is more important than the precise year in which the next oil crunch may happen is the widening gap in the 2nd half of this decade.

Conclusion: Whether the world wants to follow the New Policies Scenario of the IEA WEO 2013 is another question altogether. It seems governments are rather on a current policies track which increases oil demand and therefore pressure on oil prices.

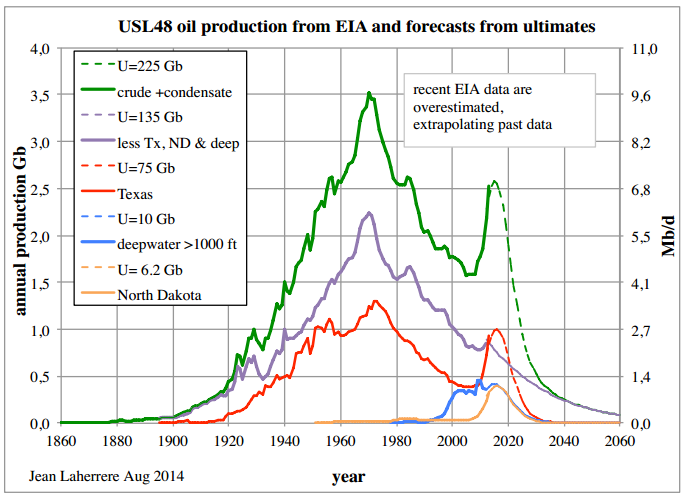

Here is a graphic that illustrates what might happen when fracking declines.

See Figure 1. The red region representing tight oil is the only thing that has kept total world oil production from having already peaked. This is evidence that only a continuation or increase in the current level of U.S. tight oil production from shale can prevent another oil price spike followed by an economic bust.

The Medium Term Oil Market Report of the International Energy Agency (IEA, Paris), published in June 2014, contains a graph which implies that US crude production will start to peak in 2016. Few took notice although the world is continuously occupied with oil and energy related conflicts and wars in Ukraine, Libya and Iraq. So far, oil prices increased only shortly when fights flared up. Apparently oil markets are at ease while the US tight oil “revolution” is underway. But for how long?

The graph [Fig 1: US tight oil and crude oil in rest of world vs oil prices] shows that US tight (shale) oil sits on top of a bumpy crude production plateau in the rest of the world which clearly started in 2005 (average of 73.4 mb/d since Jan 2005). Despite increasing tight oil production oil prices did not go down but stayed at a level of around US$ 100 a barrel. We can safely say that without US tight oil – in May 2014 around 2.9 mb/d – the world would be in a deep oil crisis. People got accustomed to a higher oil consumption level which will be hard to come down from. Between 2005 and 2007, oil production declined by around 2 mb/d (supply shock) and oil prices doubled. That gives us an idea what will happen when tight oil starts to decline. So it is important to know when tight oil reaches its tipping point.

Another prediction that tight oil from fracking will top out in its domestic production in only about three years comes from the U.S. federal government, via the Energy Information Agency (EIA) and its periodic Outlook report.

See how much difference a year can make in the “reference case” or business as usual expectations, about doubling the expected future output. However if fracking expectations can double in a single year, how accurate is the EIA tight oil production model? How sensitive is the model to oil price? Why not show the model and also show the expected tight oil output for a high, medium, and low oil price? If our future driving affordability is tied to this oil output, we deserve good data transparency.

Here is how top oil analyst Tom Whipple of

ASPO-USA reviewing the

tight oil production situation recently put it.

The two major forecasting agencies, Washington’s EIA and Paris’ IEA, are both more pessimistic than is generally known for they both foresee US shale oil production leveling off as soon as 2016. The reason for this is that drillers will simply run out of new places to drill and frack new wells. While new techniques of extracting more oil from a well are possible, there is need to look closely at the costs of these techniques vs. the potential payoff.

The shale oil situation in Texas is somewhat different than in North Dakota, for there you have much better weather and two separate shale oil deposits. The recent growth in Texas’s shale oil production has been much smoother than in storm-prone North Dakota and has been increasing at about 44,000 b/d each month. So far as can be seen from the outside of the industry, production in both states will continue to grow for at least another year or two — but then we will be at 2016.

The government has never gotten around to publishing the assumptions that go into the forecast that U.S. shale oil production will stop growing circa 2016. The biggest difference between EIA/IEA and independent analysts is the government forecasters do not see a precipitous drop in shale oil production following the peak. Instead they see a period of flat production followed by a gentle decline stretching well into the next decade. Such a gentle end to the shale oil “bubble” can only assuage fears of a calamity. This projection on a gentle end to U.S. shale oil is at variance with outside forecasters who note that shale oil wells are pretty well gone in three years and simply do not see where the oil to maintain production levels will be coming from for another 10 or 15 years after the peak…

Independent analyses of U.S. shale oil generally come to the same conclusion that production will peak in the 2016-2017 time frame, but as noted above see a much faster decline than does the government.

Hydrofracturing for tight oil and gas is now about all that is left to maintain global oil production

Hydrofracturing for tight oil and gas is now about all that is left to maintain global oil production, as Art Berman points out in

this interview: “Shale, the Last Oil and Gas Train”

Oil companies have to make a big deal about shale plays because that is all that is left in the world. Let’s face it: these are truly awful reservoir rocks and that is why we waited until all more attractive opportunities were exhausted before developing them. It is completely unreasonable to expect better performance from bad reservoirs than from better reservoirs. The majors have shown that they cannot replace reserves. They talk about return on capital employed (ROCE) these days instead of reserve replacement and production growth because there is nothing to talk about there. Shale plays are part of the ROCE story–shale wells can be drilled and brought on production fairly quickly and this masks or smoothes out the non-productive capital languishing in big projects around the world like Kashagan and Gorgon, which are going sideways whilst eating up billions of dollars. None of this is meant to be negative. I’m all for shale plays but let’s be honest about things, after all! Production from shale is not a revolution; it’s a retirement party. [emphasis mine]

Finally, lets conclude this section with a

peak shale oil prediction for 2016 made by one of the most skillful resource data analysts, Jean Laherrere, who along with Colin Campbell coauthored “The End of Cheap Oil” in

Scientific American in 1998, when oil cost less than $20 a barrel. Scroll toward the end of the link and see a big green hump in a chart that represents the official EIA Outlook prediction of a peak in shale oil in 2017. Laherrere’s peak for shale oil is followed by a much steeper decline rate as can be seen in the subsequent chart.

As Laherrere says:

It seems that most oil companies are spending more than their revenues by increasing their debts. Countries can live for a long time with huge debt increase, not companies. They count on the stock market by delivering optimistic reports and keep drilling to avoid the production to decline. With shale oil or shale play, in contrary with conventional where wells are dry or producing, oil can be produced even for a while if not economical.

Such behavior explains why most peak forecasts are wrong. But the main question is about the slope of the decline after the peak. EIA forecast a LTO (light tight oil = shale oil) peak in 2017 it is not too far after my forecast, the big difference is the slow EIA LTO decline.

Why fuel prices probably won’t fall much more

Why won’t the price of driving, as affected by fuel cost, go down very much or for very long? The Saudis alone can produce about 10 million barrels of oil a day mostly for export. This gives the Saudis the ability, acting as one country with a centralized oil production policy, to put a floor under the global oil price simply by cutting back on their oil offered for export. Abundant Saudi oil exports remain vital to a world of commerce built with and quite dependent on affordable oil.

The Saudis lack the excess oil production capacity that they once had, so they cannot flood the market to lower the oil price.

The Saudis lack the

excess oil production capacity that they once had, so they cannot flood the market to lower the oil price. However the Saudis still have the critical market power, through cutting production, to keep global crude oil prices from sinking.

“We are swimming in crude, and they [the Saudis] know that better than anyone because they are the biggest exporter,” Mike Wittner, the head of oil market research at Societe Generale in New York, said by phone Sept. 9. “History shows that the Saudis will just do what’s necessary.” … Saudi Arabia made the biggest contribution to OPEC’s production cuts in 2008 and 2009 as demand contracted amid the financial crisis. The group took almost 5 million barrels of daily output off the market, reviving prices from about $30 at the end of 2008 to almost $80 a year later.

At its current price, “Brent has traded since early July within the

range of $95 to $110 described as ‘fair’ by Saudi Oil Minister Ali Al-Naimi at a meeting of the Organization of Petroleum Exporting Countries in June.”

The Saudis have an incentive to pump at or near their maximum capacity, but to

cut back when the global price sinks below their favored price range, neither so high as to hurt the global economy, nor so low that it puts other higher cost oil producers, which together supply most of the world’s other oil, out of business.

Both Saudi and Iran recently warned that declines in crude prices will be short lived. It is an ominous sign for motorists in the UK who were hoping that recent declines in the cost of a gallon of petrol would be sustained.

The Saudi’s favorable price band is shrinking and may not even exist any more because global oil customers are getting poorer, even while oil producers, especially private oil investors outside the Middle East, are losing money by producing oil under increasingly costly and difficult circumstances.

A timeless pattern of periodic energy investment overshoot

The human effort required to obtain and channel the energy needed to build and maintain an economy is a key feature of all civilizations, which ultimately limits their complexity and type of economic organization, as

Tainter has pointed out. For this reason, changes in the supply and cost of motive power, whether this is derived from oxen and slaves consuming grain or from diesel engines burning oil, can cause civilizations to rise and fall and to win or lose wars.

The oil industry has always been characterized by boom and bust investment cycles.

As a primary and vital source of such power, the oil industry has always been characterized by boom and bust investment cycles, a pattern of exuberant investment in production followed by ruinous periodic production gluts. Frenzied oil production in the giant East Texas field during the early depression years caused the oil price to fall as low as 13 cents a barrel. The Texas governor called out the Texas Rangers

to halt and regulate excessive production, which was permanently damaging oil fields.

Later regulation from the Texas Railroad Commission established allowable oil production limits that effectively set world oil prices from the 1930s until the 1960s. This Texas regulation of private producers later served as the regulation model for OPEC, created to prevent ruinous price volatility in the unregulated global oil market.

In

Part 1, we saw the federal data compiled by the EIA, which indicates that not only are the top 127 energy companies losing money on oil and gas, but that meanwhile most OPEC oil producing countries are also having trouble meeting their costs by selling oil to a depressed global market.

Deep water oil production in the Gulf of Mexico was expanding fairly rapidly until recently. Since deep water oil is very expensive and risky — and not very profitable — production by the private majors like Exxon, those who can afford $180 million for a deep water well, have been shifting back onshore with the advent of fracking, which is more predictable in outcome and might only cost $8 million per well. Nobody would be doing deep water drilling in the Gulf of Mexico if there were profitable places left to drill on dry land, but now even the

deep water drilling has tapered off.

“Deepwater is providing lower returns and has shown no production growth while U.S. unconventionals have much higher returns (at least on paper), [and] enough scale of reserves to be of interest to the majors … so according to them, they will shift spending,” Wicklund noted.

With current economic uncertainty, investors don’t know what the price of oil will be a few years into the life of the well. Until about 2012, the global price of oil was rising nicely, comfortably over $100 a barrel, but over the last two years it has been almost flat and is now decreasing due to a stagnant or deflating global economy.

But oil producers are tied to the existing market price, for better or worse. The market demand for oil-based fuel can rise or fall much faster than the supply tends to change. A low rate of drilling sets the stage for a future price rise when the return of a tight market causes global oil prices to rise again.

Since fracking is what is has been holding U.S. driving costs down, it stands to reason that when this rapidly depleting oil source goes into decline, fuel prices will rise and we will be obliged to drive less.

Military events which could seriously interfere with driving in less than three years

There are looming but plausible threats to widely affordable American driving that are widely understood to exist but are nearly impossible to accurately predict in their severity and timing. Two major “black swan” events are first, an interruption in steady oil exports from the Middle East, and second, a swiftly developing global economic crisis which could affect the U.S. and global economies.

Our current effort to militarily contain the Sunni-based Islamic State in Iraq and deescalate regional conflict is plagued with uncertainties, if not impossibilities. Nobody can easily anticipate how military turmoil in the Sunni regions to the north might affect oil production from the Shiite dominated oil-producing regions of Iraq to the south, which are currently producing and exporting about 3 million barrels of oil a day.

Trying to use U.S. military power to keep the Middle East reliably producing its oil for export has become a daunting military juggling act.

There is much to go wrong in a conflict that could spill over into nearby Saudi Arabia, which is itself increasingly unstable. Trying to use U.S. military power to keep the Middle East reliably producing its oil for export has become a

daunting military juggling act. The new Prime minister of Iraq tells us that all

foreign troops will be unwelcome at the same time our generals tell us that the conflict cannot be won from the air.

In light of this situation, we might be better off

using diplomacy rather than relying on military power to achieve our goals.

Economic events which could seriously interfere with driving in less than three years

Gasoline has gotten a little cheaper at the pump lately, headed toward $3 a gallon, which has the welcome effect of stimulating the U.S. economy by putting some extra dollars in the pockets of most drivers. But it doesn’t change the big picture much.

The USA remains in an economic crisis because of low growth, a dependence on easy money from the Fed, and an inability to revive the U.S. economy despite a

massive level of quantitative easing.

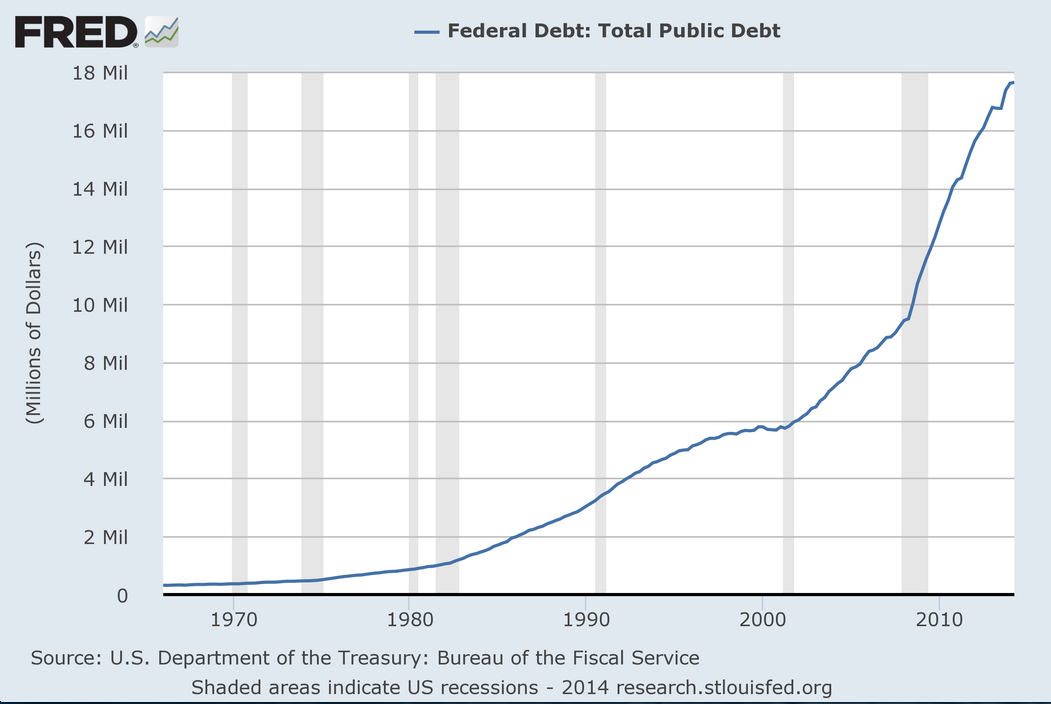

It is hard not to see that the easy credit and low interest rates are tied to the new public debt shown in Figure 5, and that this cash is seeking out stocks. It looks like the Fed’s quantitative easing is inflating stock prices, which are soaring, but that this cash is avoiding investment in the stagnating economy of high unemployment and minimum wage jobs familiar to those who don’t own stocks. The Nasdaq composite index looks even more peaky. Looking like an asset bubble in search of profitable investment in the self-promoting world of finance, rather than in the struggling hard times economy unable to keep growing without cheap oil. How high will the latest shark tooth get before it falls again?

It is is not widely understood that the great recession of 2008 was initiated when oil surged to $147 a barrel in mid-year, followed by a banking liquidity paralysis and a steep oil price collapse. This same event also tells us roughly what to expect when the current oil glut is succeeded by another oil price spike. Dr James Hamilton has done

a lot of economic analysis that strongly links oil price rises to subsequent recessions.

The USA is slowly moving in the right direction, burning less oil and we are driving less than ever, but the easy progress has already been made. We still have to import roughly the same amount of oil that we produce domestically just to keep driving normally. There is essentially one big global oil market which has Americans bidding against the Chinese and everyone else for fuel, in the context of a shrinking supply of globally traded oil.

The Chinese economy now seems to be headed into its own growth slump.

The Chinese economy now seems to be

headed into its own growth slump. For a decade or more, investments in many sorts of raw materials, including oil, have depended on strong Chinese demand that acted as an economic engine to maintain global trade and support rising commodity prices.

…In other words, we are now in a world in which the biggest economy, Europe, is about to enter a triple-dip recession, and the third largest standalone economy, China, is undergoing an economic standstill, and all hopes and prayers are that China will join the ECB in activating monetary easing once again. But yes, the Fed will not only conclude QE but will supposedly begin rising rates in just over two quarters. Good luck with that.

With a global economy depressed for years by the stress of about $100 a barrel oil prices, and with attempts to revive the US. economic growth ineffective, aside from what looks like a stock bubble, we could easily slip into a global deflationary spiral. It is not apparent that the global economy can grow at all without cheap oil. As a result, we have a world flush with dollars that have a

very low velocity of circulation and a cautious deflationary spending psychology prevails.

Richard Heinberg’s book

The End of Growth pointed out that, with the end of cheap oil, the global economy is likely to be incapable of real material growth, as opposed to financial sector growth. Good economists are starting to realize that the future

doesn’t work very well without cheap oil.

Peak oil could be the catalyst for global collapse. Some see new fossil fuel sources like shale oil, tar sands and coal seam gas as saviours, but the issue is how fast these resources can be extracted, for how long, and at what cost. If they soak up too much capital to extract the fallout would be widespread.

Gail Tverberg in her excellent blog

Our Finite World, thinks

global deflation is happening now. (“Low Oil Prices: Sign of a Debt Bubble Collapse, Leading to the End of Oil Supply?”)

I would argue that falling commodity prices are bad news. It likely means that the debt bubble which has been holding up the world economy for a very long time — since World War II, at least — is failing to expand sufficiently. If the debt bubble collapses, we will be in huge difficulty…

Tom Whipple, who we saw comment earlier, points out that social and economic problems related to peak oil

are already global, and are around us everywhere whether or not we are able to understand the connections.

If we step back and acknowledge that the shale oil phenomenon will be over in a couple of years and that oil production is dropping in the rest of the world, then we have to expect that the remainder of the peak oil story will play out shortly. The impact of shrinking global oil production, which has been on hold for nearly a decade, will appear. Prices will go much higher, this time with lowered expectations that more oil will be produced as prices go higher. The great recession, which has never really gone away for most, will return with renewed vigor and all that it implies…

All this is telling us that the peak oil crisis we have been watching for the last ten years has not gone away, but is turning out to be a more prolonged event than previous believed. Many do not believe that peak oil is really happening as they read daily of surging oil production and falling oil prices. Rarely do they hear that another shoe has yet to drop and that much worse in terms of oil shortages, higher prices and interrupted economic growth is just ahead. We are sitting in the eye of the peak oil crisis and few recognize it. Five years from now, it should be apparent to all.

Part 3 of ‘America: You’ve got three more years to drive normally!’

This is yet to come, and will examine what might happen when the tangle of problems that come with a faltering economy finally exceed our cultural capability for denial. Could an end to affordable driving create enough of a political shock to spur even our gridlocked congress to take decisive action? If so, what action? Gas rationing? Peak oil and global warming are two branches of the same denial syndrome, but of these two, driving affordability definitely has a shorter fuse.

Easy driving remains basic to American lifestyle and social identity. For now, Americans are still managing to drive nearly as much as they did a decade ago. But what happens in a few years, when gasoline prices keep going up as wages remain flat, when drivers bid for the same oil needed to heat homes in New England. Who gets the oil and who gets the blame? Will the loss of mainstream driving ability finally create a political tipping point that could lead us to broadly confront and accept natural limits to growth?

The Rag Blog

Plantagenet on Fri, 3rd Oct 2014 9:15 am

As the oil glut continues the price of oil drops lower and lower. An oil glut is not what one would expect if we are at peak oil.

Davy on Fri, 3rd Oct 2014 9:33 am

Planter not sure if you are being sarcastic or serious. PO dynamics is all about shortages and gluts in a vicious cycle of produced/consumer volatility. The oil goldilocks range is compressing and this spells doom for globalism. It may take a few years but the tension and pressures this vital resources exerts on the wider economy will exasperate all the other predicaments we are in. If these other predicaments and or black swans don’t get us then negative PO dynamics will. PO dynamics is the glass cieling of doom.

Northwest Resident on Fri, 3rd Oct 2014 11:03 am

“…our cultural capability for denial.”

That capability for denial is of course aided, abetted and to a large extent created by the massive inundation of lies and propaganda being pumped through all media channels, originating from the entrenched interests who seek to keep the masses IN denial.

bobinget on Fri, 3rd Oct 2014 11:10 am

http://www.eia.gov/petroleum/supply/weekly/

Read this inventory report for last week and this coming Wednesday. Then… tell us with a straight face, “there is a real oil glut”.

Don’t wait for gasoline shortages, read it today.

Unsurprised at this morning’s favorable employment report BECAUSE I read this above report

Wednesday morning.

Oh, BTW, it’s only the growth RATE slowing oil imports to China, (up 4.2%) NOT actual amounts.

China’s oil imports latest, images. Google question.

http://www.eia.gov/countries/cab.cfm?fips=ch

In fewer then ten years China will need to import every available oil barrel worldwide.

http://businessdayonline.com/2014/09/chinas-oil-imports-surge-by-17-5-percent/#.VC7FzEu5JBU

If a Western public understood these numbers they would not buy any SUV’s whose sales are back to old levels.

Oil prices have been talked down so;

Hedge funds to make quick bucks in both directions,

promote auto sales, return to full employment, sell houses off public transportation routes, ‘sanction’ Russia, Iran, eliminate wildcatter E&P, permit ‘big oil’

to buy up nearly bankrupt mom and pop operations.

maybe biggest reason of all; keep Allied fuel costs lower in the as yet unspoken World Oil War #3.

(modern warfare requires inordinate oil consumption)

Count the number of nations currently involved fighting Ebola. Now, do a count on those fighting I.S.

While your at it, weigh the INK splattered on both current crisis vs the more important climate change issues.

ghung on Fri, 3rd Oct 2014 11:18 am

Of course, seeding denial (propaganda) is viewed as a necessary tool when there isn’t much capacity for response. We see it with climate change, the debt, and I get the feeling it’s going on with this ebola epidemic. The last thing TPTB want is more fear, even when fear is appropriate. Reality is a double-edged sword for a population that’s been told to “just go shopping” for so long.

penury on Fri, 3rd Oct 2014 11:39 am

The only important date to remember for U.S. is Nov 2016. This country will continue with wars, invasions sending soldiers to fight Ebola in countries which have oil, building bases in countries (Africa) where the possibility of FFs are present. i don’t know how long the lies and distortions can continue to blind the Amer Sheeple, but I do think that at this point the only goal of the PTB is to maintain the facade until after 2016. My personal belief is that they will fail dismally in 2015.

Davy on Fri, 3rd Oct 2014 11:48 am

Oh, Pen, fighting Ebola for oil. Come on friend their is very little oil in west Africa worth getting. Pen can you review Shell’s experience in Nigeria. Get back to me after chewing on that. Stay focused don’t join the Star Wars crowd here on this board.

Plantagenet on Fri, 3rd Oct 2014 11:53 am

@Davi

If an oil glut and falling oil prices are signs of peak oil, then what do oil shortages and high oil prices mean?

Face facts—we are close to peak oil but we aren’t there yet—in fact because of fracking we currently have a global oil glut and falling oil prices.

Perk Earl on Fri, 3rd Oct 2014 11:54 am

“Since cheap conventional oil globally peaked in 2005, the higher price of fuel has acted like a slowly increasing but hidden tax on almost everything sold, since almost everything sold has some rising oil price costs embedded in its sales price.”

And these higher prices are increasing the cost of extraction, etc. described below:

“However, extracting and delivering those resources at an affordable price is becoming a bigger challenge year by year. For the oil industry, costs of production have rocketed; they’re currently soaring at a rate of about 10 percent annually.”

The governments try to prop the BAU system up with all sorts of stimulus, but as tax revenue flattens and debt skyrockets, those tactics wane, and as they do consumption of all products worldwide declines, leading to our recent drop in oil price.

Dropping oil price puts pressure on non-conventional sources, shrinking profits. When some of those sources start to go offline, serious concerns by TPTB should ensue, but to what avail? Descending EROEI can only be fought for so long.

marmico on Fri, 3rd Oct 2014 12:11 pm

but as tax revenue flattens and debt skyrockets

Nope and nope.

Davy on Fri, 3rd Oct 2014 12:15 pm

Planter, what part of the face the facts of a dynamic system do you not understand? When a dynamic system hits turbulence you aren’t going to use Econ 101 like Marm and Noo show try to do to explain a market dysfunctions. Add to the PO turbulence market distortions, manipulations, and corruption and you get dysfunction. Planter you are at a higher PO understanding level then the corn-tellectuals here on this board.

Plantagenet on Fri, 3rd Oct 2014 12:25 pm

Davi—of course economic systems are dynamic. Prices respond to supply and demand. I’m just pointing out that the world is not yet at peak oil—in fact we currently are in an oil glut. The ongoing decline in oil prices is due to an oversupply of oil at a time when most economies around the world are growing slowly at best.

Northwest Resident on Fri, 3rd Oct 2014 12:35 pm

“…the world is not yet at peak oil…”

Sure, just like the convicted cattle rustler wasn’t hanged yet — until milliseconds later when the hangman pulled the lever.

IF we aren’t at peak oil just yet, we most certainly are teetering on the brink with no chance in hell of backing away from that steep ledge.

I’m not so sure I would think of it as an “oil glut” — very misleading MSM term. That “oil glut” isn’t even a day’s worth of global oil consumption, is it? So let’s stop using that term, please. I’m not even sure that “glut” is actually “oil” — more likely it is a bunch of fracked liquids some of which is oil.

steve on Fri, 3rd Oct 2014 12:53 pm

Three years seems way high a number here I think at most it should be two years….unless of course we have a great depression or ww3…and then numbers could change a lot…

You need to google one of Steve Kopits talks to get the real story….there is no way we make it past 3 years…

marmico on Fri, 3rd Oct 2014 1:00 pm

more likely it is a bunch of fracked liquids some of which is oil.

Read the EIA report on LTO crude types. Most of it is oil.

Northwest Resident on Fri, 3rd Oct 2014 1:11 pm

Some of it. Most of it. Basically the same thing, whatever. And how big is that “glut”? Is it anywhere close to 100 million barrels of actual, real oil? Because if not, then it isn’t even enough for one days worth of global consumption — which would make that much ballyhooed “glut” nothing more than a drop in the bucket.

“World consumption will increase by 1.4 million barrels a day, or 1.5 percent, this year to a record 92.7 million a day, or about 95,000 a day more than forecast last month, according to the IEA, a Paris-based adviser to oil-consuming nations.”

penury on Fri, 3rd Oct 2014 2:17 pm

Davy, the U.S has just built a new base, I believe it is called CAC in (of course the Central Africa Republic. We have built bases in Sudan, Nigeria and have troops in other locations to assure that we can maintain access to the FF. But out of curisoty, do you know how many troops we sent after Joseph Kony? How many troops did we send to Nigeria to “Return our Girls?” How many troops are we sending to fight Ebola? After you disregard all of those, how many drone strikes have we used in Sudan? If you are of the opinion that none of this is related to the current oil situation I will apoloogize for wasting your time.

Davy on Fri, 3rd Oct 2014 2:26 pm

Pen, come on please. I will go along with your line of thinking with the war on ISIL but Africa is just not a FF Meca. We are in Africa for multiple reason and the usual American FF piracy aurgument is wasting my time. So as Planter does when he tires of an aurgument…CHEERS

Don on Fri, 3rd Oct 2014 4:34 pm

Ya know Davy, just to point out, this is really one of the things you have asked for many times. 3 more years, if Baker’s prediction is correct to be prepared. Could you ask for a better start to those 3 years? The dollar is stronger than it’s ever been, yes it is propped up on QE and that is terrible in and of itself but still, ~$3 gal gas, ~$17 tr oz silver, and AF having a 40% harvest sale.

This is really a dream come true for most anyone that is worried about the effects of PO and was worried they might not have time to prepare, like myself. I can tell you my shelves are filling quick right now with commodities dropping the way they are.

In short don’t look a gift horse in the mouth. You have been praying for 3 more years to get the farm in order and it’s possible those prayers were answered. Be happy and take advantage of the peaks when they come so you can weather the valleys.

Davy on Fri, 3rd Oct 2014 4:51 pm

Don, I am not sure where our thinking got crossed but I am exactly where you are and happy and thankful. Don, sometimes I try to be funny (dry), sarcastic, or talk word salad (marm phase) when discussing issues there by coming across different from what I mean to say. I may have done that with you. I am right with your thinking in the above comment.

Craig Ruchman on Fri, 3rd Oct 2014 6:42 pm

plant – Prodigious outpourings of energy are the norm at the point of death or depletion: a mortally wounded dog dashes madly about; older stars that have used up their store hydrogen burn what remains at ever faster rates and become red giants. I got a raise at work last month that was lower than the rate of inflation, so I know there is nothing wrong with the oil based economy.

Kenz300 on Fri, 3rd Oct 2014 9:09 pm

Walk, buy a bicycle or use mass transit……….. the less you rely on a car the better……..

Some cities and states encourage bikes………. they provide safe walking and biking lanes and trails. Cities also should encourage businesses and apartments to provide safe places to lock or store a bicycle. Encourage your elected officials to do more. Speak up.. become an advocate for bicycle use in your city.

Top 10 Cycling-Friendly Cities – YouTube

https://www.youtube.com/watch?v=ycKXeKfu4lo

———————

Bike Friendly Cities, The Journey to School – YouTube

https://www.youtube.com/watch?v=4-XenU6UEp8

Makati1 on Sat, 4th Oct 2014 5:32 am

Let’s see:

2014

Lower oil/gas prices (glut). Other events: November election in US.

2016

Still chugging along and probability of lower oil/gas prices 80% Other events: Hillary gets her wish and sleeps in the White House again, this time openly wearing the pants.

2017

The SHTF and we go to war, ending in a nuclear exchange? And/or, the world is leveled to 3rd world economic status. Any other ideas?

Dredd on Sat, 4th Oct 2014 9:49 am

Psychology is the main driver of peak oil concepts.

Denial is a part of the “group-mind trance” … a psychologist phrase.

(Comparing a Group-Mind Trance to a Cultural Amygdala).