The standard way to make forecasts of almost anything is to look at recent trends and assume that this trend will continue, at least for the next several years. With world oil production, the trend in oil production looks fairly benign, with the trend slightly upward (Figure 1).

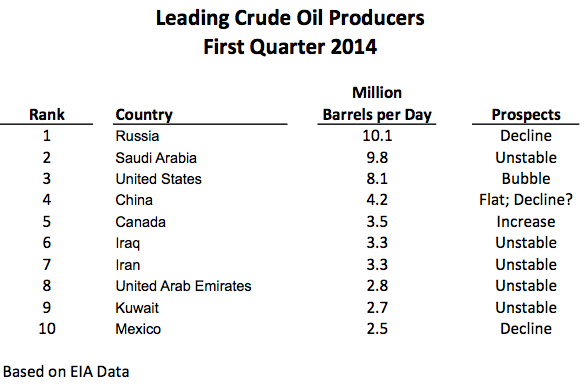

If we look at the situation more closely, however, we see that we are dealing with an unstable situation. The top ten crude oil producing countries have a variety of problems (Figure 2). Middle Eastern producers are particularly at risk of instability, thanks to the advances of ISIS and the large number of refugees moving from one country to another.

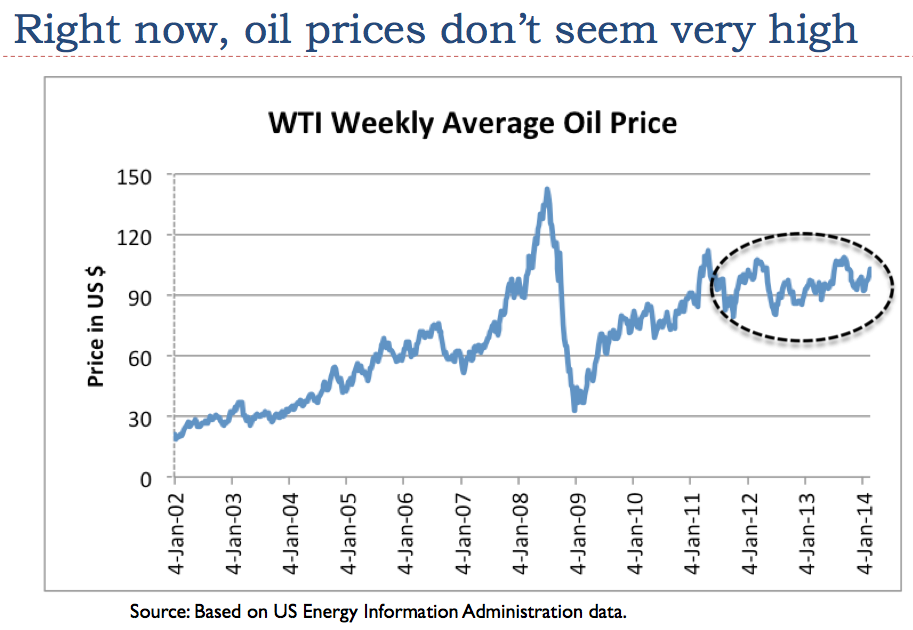

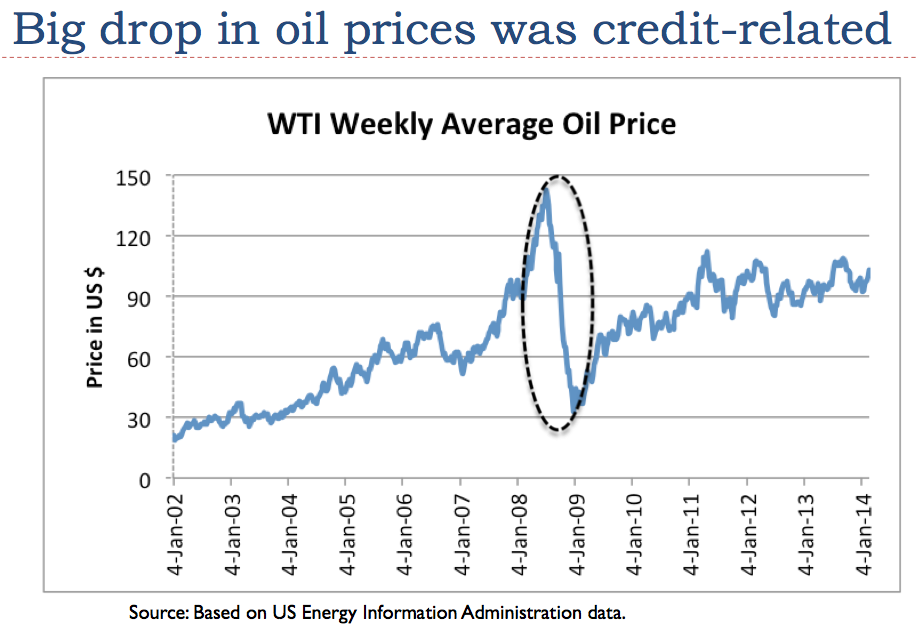

Relatively low oil prices are part of the problem as well. The cost of producing oil is rising much more rapidly than its selling price, as discussed in my post Beginning of the End? Oil Companies Cut Back on Spending. In fact, the selling price of oil hasn’t really risen since 2011 (Figure 3), because citizens can’t afford higher oil prices with their stagnating wages.

The fact that the selling price of oil remains flat tends to lead to political instability in oil exporters because they cannot collect the taxes required to provide programs needed to pacify their people (food and fuel subsidies, water provided by desalination, jobs programs, etc.) without very high oil prices. Low oil prices also make the plight of oil exporters with declining oil production worse, including Russia, Mexico, and Venezuela.

Many people when looking at future oil supply concern themselves with the amount of reserves (or resources) remaining, or perhaps Energy Return on Energy Invested (EROEI). None of these is really the right limit, however. The limiting factor is how long our current networked economic system can hold together. There are lots of oil reserves left, and the EROEI of Middle Eastern oil is generally quite high (that is, favorable). But instability could still bring the system down. So could popping of the US oil supply bubble through higher interest rates or more stringent lending rules.

The Top Two Crude Oil Producers: Russia and Saudi Arabia

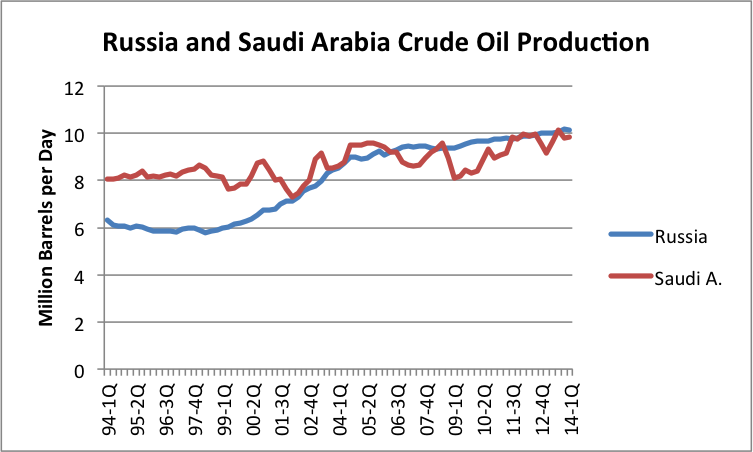

When we look at quarterly crude oil production (including condensate, using EIA data), we see that Russia’s crude oil production tends to be a lot smoother than Saudi Arabia’s (Figure 4). We also see that since the third quarter of 2006, Russia’s crude oil production tends to be higher than Saudi Arabia’s.

Both Russia and Saudi Arabia are headed toward problems now. Russia’s Finance Minister has recently announced that its oil production has hit and peak, and is expected to fall, causing financial difficulties. In fact, if we look at monthly EIA data, we see that November 2013 is the highest month of production, and that every month of production since that date has dropped from this level. So far, the drop in oil production has been relatively small, but when an oil exporter is depending on tax revenue from oil to fund government programs, even a small drop in production (without a higher oil price) is a financial problem.

We see in Figure 4 above that Saudi Arabia’s quarterly oil production is quite erratic, compared to oil production of Russia. Part of the reason Saudi Arabia’s oil production is so erratic is that it extends the life of its fields by periodically relaxing (reducing) production from them. It also reacts to oil price changes–if the oil price is too low, as in the latter part of 2008 and in 2009, Saudi oil production drops. The tendency to jerk oil production around gives the illusion that Saudi Arabia has spare production capacity. It is doubtful at this point that it has much true spare capacity. It makes a good story, though, which news media are willing to repeat endlessly.

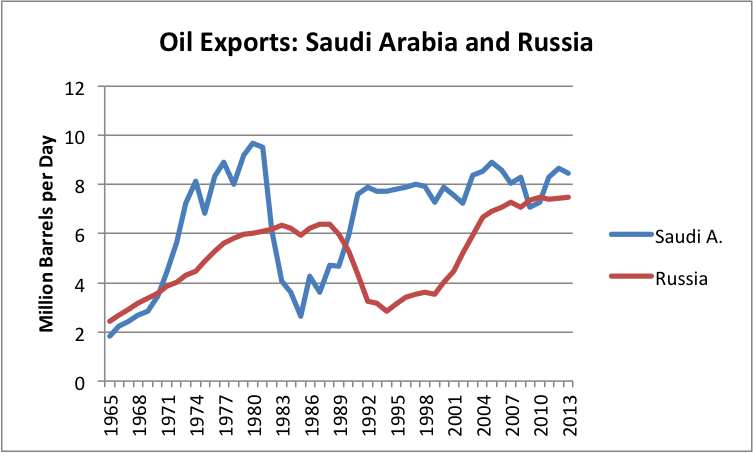

Saudi Arabia has not been able to raise oil exports for years (Figure 5). It gained a reputation for its oil exports back in the late 1970s and early 1980s, and has been able to rest on its laurels. Its high “proven reserves” (which have never been audited, and are doubted by many) add to the illusion that it can produce any amount it wants.

In 2013, oil exports from Russia were equal to 88% of Saudi Arabian oil exports. The world is very close to being as dependent on Russian oil exports as it is on Saudi Arabian oil exports. Most people don’t realize this relationship.

The current instability of the Middle East has not hit Saudi Arabia yet, but there is increased fighting all around. Saudi Arabia is not immune to the problems of the other countries. According to BBC, there is already a hidden uprising taking place in eastern Saudi Arabia.

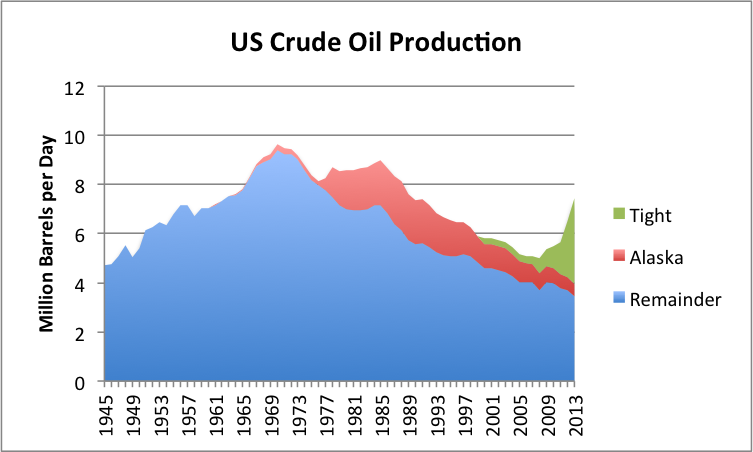

US Oil Production is a Bubble of Very Light Oil

The US is the world’s third largest producer of crude and condensate. Recent US crude oil production shows a “spike” in tight oil productions–that is, production using hydraulic fracturing, generally in shale formations (Figure 6).

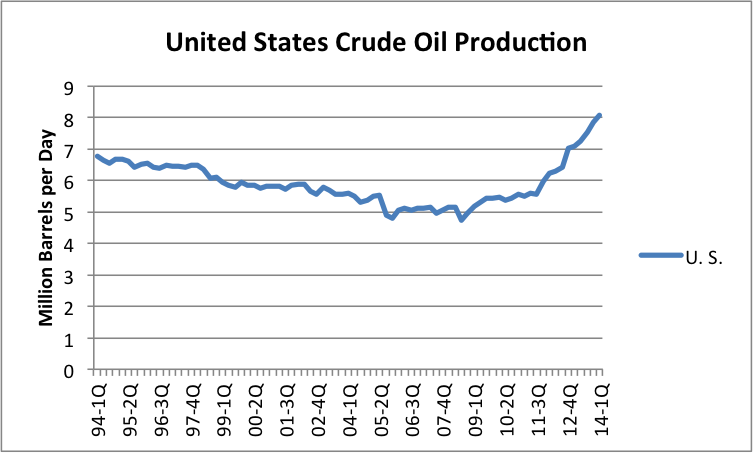

If we look at recent data on a quarterly basis, the trend in production also looks very favorable.

The new crude is much lighter than traditional crude. According to the Wall Street Journal, the expected split of US crude is as follows:

There are many issues with the new “oil” production:

- The new oil production is so “light” that a portion of it is not what we use to power our cars and trucks. The very light “condensate” portion (similar to natural gas liquids) is especially a problem.

- Oil refineries are not necessarily set up to handle crude with so much volatile materials mixed in. Such crude tends to explode, if not handled properly.

- These very light fuels are not very flexible, the way heavier fuels are. With the use of “cracking” facilities, it is possible to make heavy oil into medium oil (for gasoline and diesel). But using very light oil products to make heavier ones is a very expensive operation, requiring “gas-to-liquid” plants.

- Because of the rising production of very light products, the price of condensate has fallen in the last three years. If more tight oil production takes place, available prices for condensate are likely to drop even further. Because of this, it may make sense to export the “condensate” portion of tight oil to other parts of the world where prices are likely to be higher. Otherwise, it will be hard to keep the combined sales price of tight oil (crude oil + condensate) high enough to encourage more tight oil production.

The other issue with “tight oil” production (that is, production from shale formations) is that its production seems to be a “bubble.” The big increase in oil production (Figure 6) came since 2009 when oil prices were high and interest rates were very low. Cash flow from these operations tends to be negative. If interest rates should rise, or if oil prices should fall, the system is likely to hit a limit. Another potential problem is oil companies hitting borrowing limits, so that they cannot add more wells.

Without US oil production, world crude oil production would have been on a plateau since 2005.

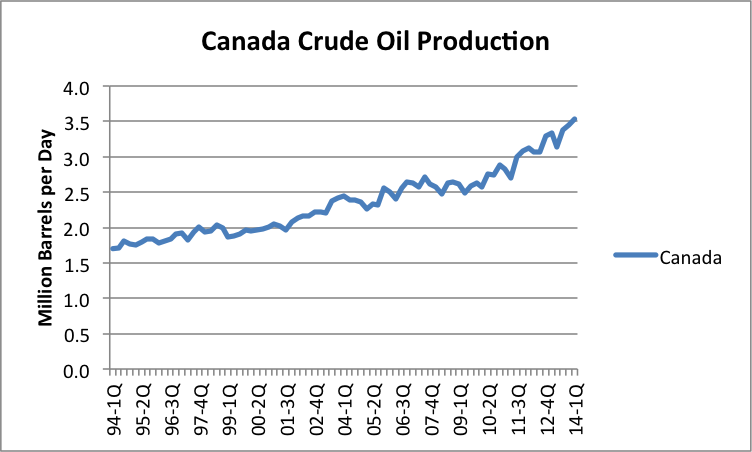

Canadian Oil Production

The other recent success story with respect to oil production is Canada, the world’s fifth largest producer of crude and condensate. Thanks to the oil sands, Canadian oil production has more than doubled since the beginning of 1994 (Figure 10).

Of course, there are environmental issues with respect to both oil from the oil sands and US tight oil. When we get to the “bottom of the barrel,” we end up with the less environmentally desirable types of oil. This is part of our current problem, and one reason why we are reaching limits.

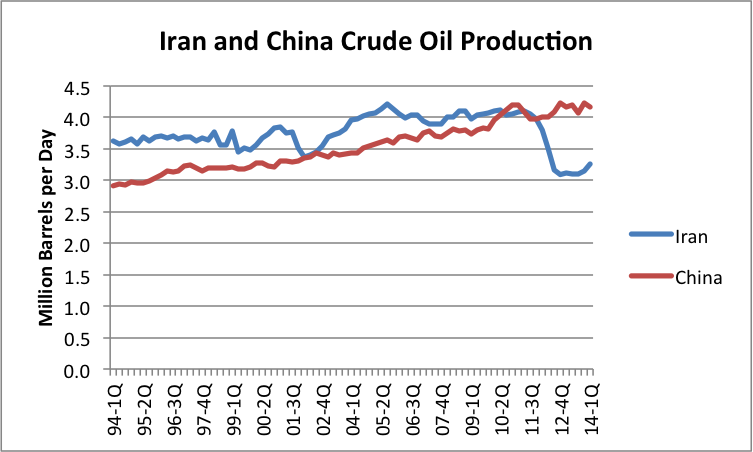

Oil Production in China, Iraq, and Iran

In the first quarter of 2014, China was the fourth largest producer of crude oil. Iraq was sixth, and Iran was seventh (based on Figure 2 above). Let’s first look at the oil production of China and Iran.

As of 2010, Iran was the fourth largest producer of crude oil in the world. Iran has had so many sanctions against it that it is hard to figure out a base period, prior to sanctions. If we compare Iran’s first quarter 2014 oil production to its most recent high production in the second quarter of 2010, oil production is now down about 870,000 barrels a day. If sanctions are removed and warfare does not become too much of a problem, oil production could theoretically rise by about this amount.

China has relatively more stable oil production than Iran. One concern now is that China’s oil production is no longer rising very much. Oil production for the fourth quarter of 2013 is approximately tied with oil production for the fourth quarter of 2012. The most recent quarter of oil production is down a bit. It is not clear whether China will be able to maintain its current level of production, which is the reason I mention the possibility of a decline in oil production in Figure 2.

The lack of growth in China’s oil supplies may be behind its recent belligerence in dealing with Viet Nam and Japan. It is not only exporters that become disturbed when oil supplies are not to their liking. Oil importers also become disturbed, because oil supplies are vital to the economy of all nations.

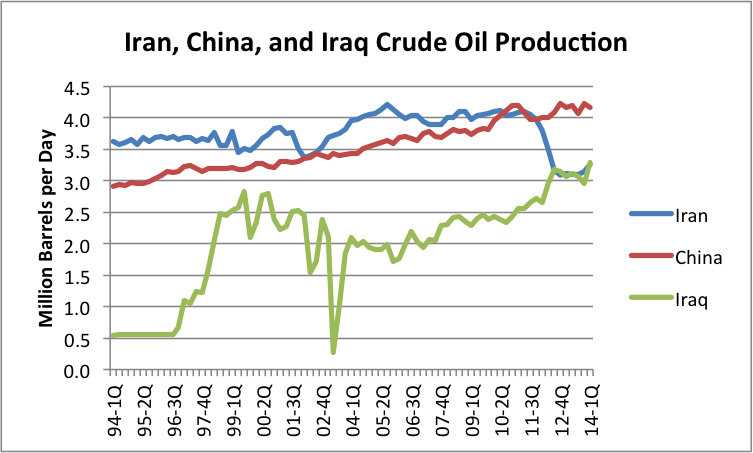

Now let’s add Iraq to the oil production chart for Iran and China.

Thanks to improvements in oil production in Iraq, and sanctions against Iran, oil production for Iraq slightly exceeds that of Iran in the first quarter of 2014. However, given Iraq’s past instability in oil production, and its current problems with ISIS and with Kurdistan, it is hard to expect that Iraq will be a reliable oil producer in the future. In theory Iran’s oil production can rise a few million barrels a day over the next 10 or 20 years, but we can hardly count on it.

The Oil Price Problem that Adds to Instability

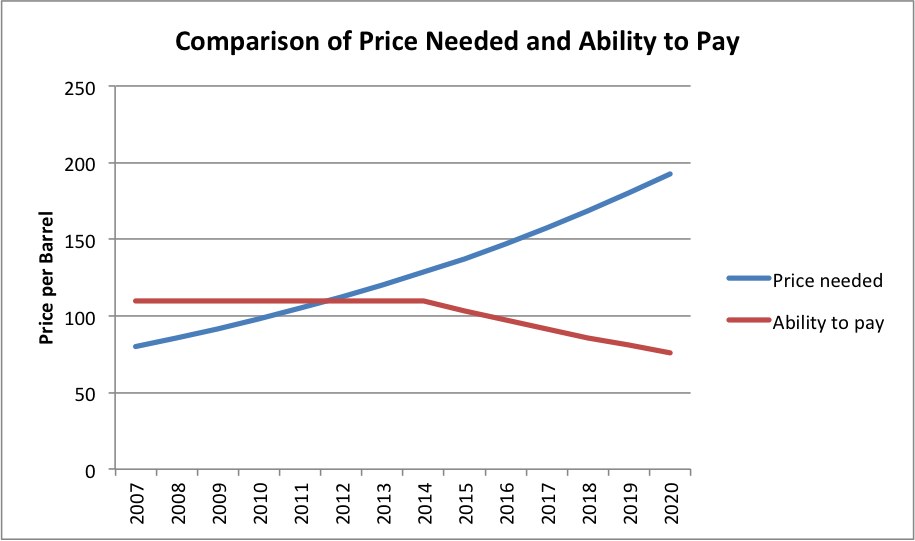

Figure 13 shows my view of the mismatch between (1) the price oil producers need to extract their oil and (2) the price consumers can afford. The cost of extraction (broadly defined including taxes required by governments) keeps rising while “ability to pay” has remained flat since 2007. The inability of consumers to pay high prices for oil (because wages are not rising very much) explains why oil prices have remained relatively flat in Figure 3 (near the top of this post), even while there is fighting in the Middle East.

When the selling price is lower than the full cost of production (including the cost of investing in new wells and paying dividends to shareholders), the tendency is to reduce production, one way or another. This reduction can be voluntarily, in the form of a publicly traded company buying back stock or selling off acreage.

Alternatively, the cutback can be involuntary, indirectly caused by political instability. This happens because oil production is typically heavily taxed in oil exporting nations. If the oil price remains too low, taxes collected tend to be too low, making it impossible to fund programs such as food and fuel subsidies, desalination plants, and jobs programs. Without adequate programs, there tend to be uprisings and civil disorder.

If a person looks closely at Figure 13, it is clear that in 2014, we are out in “Wile E. Coyote Territory.” The broadly defined cost of oil extraction (including required taxes by exporters) now exceeds the ability of consumers to pay for oil. As a result, oil prices barely spike at all, even when there are major Middle Eastern disruptions (Figure 3, above).

The reason why Wile E. Coyote situation can take place at all is because it takes a while for the mismatch between costs and prices to work its way through the system. Independent oil companies can decide to sell off acreage and buy back shares of stock but it takes a while for these actions to actually take place. Furthermore, the mismatch between needed oil prices and charged oil prices tends to get worse over time for oil exporters. This lays the groundwork for increasing dissent within these countries.

With oil prices remaining relatively flat, importers become complacent because they don’t understand what is happening. It looks like we have no problem when, in fact, there really is a fairly big problem, lurking behind the scenes.

To make matters worse, it is becoming more and more difficult to continue Quantitative Easing, a program that tends to hold down longer-term interest rates. The expectation is that the program will be discontinued by October 2014. The reason why the price of oil has stayed as high as it has in the last several years is because of the effects of quantitative easing and ultra low interest rates. If it weren’t for these, oil prices would fall, because consumers would need to pay much more for goods bought on credit, leaving less for the purchase of oil products. See my recent post, The Connection Between Oil Prices, Debt Levels, and Interest Rates.

Because of the expectation that Quantitative Easing will end by October 2014 and the pressure to tighten credit conditions, my expectation is that the affordable price of oil will start dropping in late 2014, as shown in Figure 13. The growing disparity between what consumers can afford and what producers need tends to make the Wile E. Coyote overshoot condition even worse. It is likely to lead to more problems with instability in the Middle East, and a collapse of the US oil production bubble.

Conclusion

I explained earlier that we live in a networked economy, and this fact changes the way economic models work. Many people have developed models of future oil production assuming that the appropriate model is a “bell curve,” based on oil depletion rates and the inability to geologically extract more oil. Unfortunately, this isn’t the right model.

The situation is far more complex than simple geological decline models assume. There are multiple limits involved–prices needed by oil producers, prices affordable by oil importers, and prices for other products, such as water and food. Interest rates are also important. There are time lags involved between the time the Wile E. Coyote situation begins, and the actions to fix this mismatch takes place. It is this time lag that tends to make drop-offs very steep.

The fact that we are dealing with political instability means that multiple fuels are likely to be affected at once. Clearly natural gas exports from the Middle East will be affected at the same time as oil exports. Many other spillover effects are likely to happen as well. US businesses without oil will need to cut back on operations. This will lead to job layoffs and reduced electricity use. With lower electricity demand, prices for electricity as well as for coal and natural gas will tend to drop. Electricity companies will increasingly face bankruptcy, and fuel suppliers will reduce operations.

Thus, we cannot expect decline to follow a bell curve. The real model of future energy consumption crosses many disciplines at once, making the situation difficult to model. The Reserves / Current Production model gives a vastly too high indication of future production, for a variety of reasons–rising cost of extraction because of diminishing returns, need for high prices and taxes to support the operations of exporters, and failure to consider interest rates.

The Energy Return on Energy Invested model looks at a narrowly defined ratio–usable energy acquired at the “well-head,” compared to energy expended at the “well-head” disregarding many things–including taxes, labor costs, cost of borrowing money, and required dividends to stockholders to keep the system going. All of these other items also represent an allocation of available energy. A multiplier can theoretically adjust for all of these needs, but this multiplier tends to change over time, and it tends to differ from energy source to energy source.

The EROEI ratio is probably adequate for comparing two “like products”–say tight oil produced in North Dakota vs tight oil produced in Texas, or a ten year change in North Dakota energy ratios, but it doesn’t work well when comparing dissimilar types of energy. In particular, the model tends to be very misleading when comparing an energy source that requires subsidies to an energy source that puts off huge tax revenue to support local governments.

When there are multiple limits that are being encountered, it is the financial system that brings all of the limits together. Furthermore, it is governments that are at risk of failing, if enough surplus energy is not produced. It is very difficult to build models that cross academic areas, so we tend to find models that reflect “silo” thinking of one particular academic specialty. These models can offer some insight, but it is easy to assume that they have more predictive value than they do.

Unfortunately, the limits we are reaching seem to be financial and political in nature. If these are the real limits, we seem to be not far away from the simultaneous drop in the production of many energy products. This type of limit gives a much steeper drop off than the frequently quoted symmetric “bell curve of oil production.” The shape of the drop off corresponds to (1) the type of drop off experienced by previous civilizations when they collapsed, (2) the type of drop-off I have forecast for world energy consumption, and (3) Ugo Bardi’s Seneca cliff. The 1972 book Limits to Growth by Donella Meadows et al. says (page 125), “The behavior mode of of the system shown in figure 35 is clearly that of overshoot and collapse,” so it tends to come to the same conclusion as well.

{kind=link}

{kind=link}

J-Gav on Fri, 25th Jul 2014 6:07 am

Interesting graphs as usual and I tend to agree with Gail that the traditional bell-shaped curve may not be what awaits us. I don’t know if her forecast (n°2 in the last paragraph) is on target but it’s a pretty scary one.

MSN Fanboy on Fri, 25th Jul 2014 6:32 am

“it is the financial system that brings all of the limits together”

WARNING SENECA CLIFF AHEAD

Be careful what you wish for:

Davy on Fri, 25th Jul 2014 6:50 am

It is funny for me I have related the Road Runner image I grew up with as a kid here on this forum and Gail used the Wile E. Coyote image. Oh, BTW, E stands for energy in this case. It is true Gav that this is scary. I have also related this as a “Korowicz moment” (systems theory) and “Minsky Moment” (economic theory) here on this forum. Korowicz is a strong influence on me as you all can see in my many postings (that are not Mak attack rebuts). We are near a systematic break to a lower level of economic activity. This is disequilibrium and like Gail mentions (n2 in the conclusion) the more disequilibrium the steeper the decline can be. I would also like to mention this follows the phase change of water in the laws of thermo dynamics. It takes significant energy and time for water to change phase but when it changes the change is sudden and quick. We see this in CC studies of past abrupt climate shifts. This is the danger for us humans in this highly complex, interconnected, and systematic disequilibrium we inhabit today. Our naked locals are exposed to a nourishing global ready to bifurcate in chaos and dysfunction to a lower level. There is really no way to tell how far, how quick, how long, and where the bottom is for reboot. With Wile we see what seems to be an endless fall for a kid then a far off thud.

rockman on Fri, 25th Jul 2014 8:38 am

I suspect my definition of a “bell shaped curve” differs somewhat from others. My bell shaped curves are rarely symmetric. If fact they are usually very skewed. In 40 years I’ve seen no oil patch curves of any metric that approached symmetry: well production rate, field production rate, trend production rate, country production rate, oil prices, NG prices, drill rig count, etc., etc. Hubbert’s curves were nothing close to symmetric. In his landmark paper he specifically said the backside of the production, though not very predictable, certainly wouldn’t be symmetric.

“…the trend in oil production looks fairly benign, with the trend slightly upward…” So it’s benign…what ever that really means. But the graphs that follow, especially the price curves, are anything but “benign”. And then there’s:”The standard way to make forecasts of almost anything is to look at recent trends and assume that this trend will continue”. The chart shows oil prices swinging from $60/bbl to $145/bbl to $40/bbl in just 3 years. If one pulls up the NG price chart for the last 15 years one would find even greater volatility. So much for “standard assumptions”.

The cornucopians just love to spout off production numbers along with “standard” projections into the future. But when you try to draw them into the financial/political/military impacts of the recent energy trends they typically go silent.

shortonoil on Fri, 25th Jul 2014 9:23 am

“The cost of producing oil is rising much more rapidly than its selling price, as discussed in my post Beginning of the End? Oil Companies Cut Back on Spending.”

Glad to see that someone is listening to us; at least somewhat. That conclusion was extracted from the ETP model several years ago. I’ve posted it here repeatedly over the last year, and I commented on it at TOD a couple of years ago. That resulted in an avalanche of denials of: “that can’t be right!” We are past the energy half way point. It takes more of the energy that is in a unit of oil to produce it than what is delivered to the general economy. Consequently, production cost are increasing faster than what can be compensated for by the end consumer. The end game is afoot!

“Many people when looking at future oil supply concern themselves with the amount of reserves (or resources) remaining, or perhaps Energy Return on Energy Invested (EROEI). None of these is really the right limit, however. The limiting factor is how long our current networked economic system can hold together.”

This is putting the cart before the horse. How long our economic system will hold together depends explicitly upon those factors. The ERoEI of conventional crude is now 9.1:1. Its theoretical lower limit is 6.9:1. At which point the laws of physics says it has to stop. Of course, the increasing societal stress produced from a declining world economy is likely to bring on very self destructive responses.

“Because of the expectation that Quantitative Easing will end by October 2014 and the pressure to tighten credit conditions, my expectation is that the affordable price of oil will start dropping in late 2014, as shown in Figure 13.”

Oil prices are not likely to drop very far, or for very long. The reason is that the largest portion of petroleum production costs are societal costs. Roads, military, education, regulation, and etc. If oil prices decreased significantly every sovereign state in the world would very shortly be bankrupt.

http://www.thehillsgroup.org/

steve on Fri, 25th Jul 2014 9:33 am

Do you think Quantitative Easing is really happening? It is just talk they are still doing it more of the same the interesting thing is interest rates…when they go up I believe that is the endgame.

Davy on Fri, 25th Jul 2014 9:37 am

Exceptionally well put by Rock and Short. Both offer the spectrum of issues relating to energy descent. If these few words do not get through Cornucopians heads I guess it will take a Louisville slugger. Enjoy being Cornucopians but the mass Cornucopian movement is subject to the laws of thermo dynamics and a finite planet. It is a dated movement. 3-10yrs. The farther you go in time the the higher the net worth one must have to absorb the stresses from our Mega predicament. Eventually the high net worth ers may have to turn to private armies that is if the uncle allows it because mad max confiscation is probable.

forbin on Fri, 25th Jul 2014 9:42 am

shortonoil

question for you – I posit that oil will be produced even when past 6.9:1 ratio as such oil will be used to help extract coal.

Its the dynamic of coal and oil that will produce an interesting picture.

Of course do not expect we’d recognise the world as that happens….

forbin

Nony on Fri, 25th Jul 2014 9:57 am

1. I have no idea what a networked economy is. Is it like Amway? I think the economy or at least the principles of supply and demand, investment, etc. have not changed in last 50 years or so.

2. The comment about condensate usage capacity in the US and need to export is interesting. Same will apply with light oil also.

3. On a world basis, the new oil coming from the US is actually desirable. If we did an average (current) price of the grades, I bet it has increased over the years. Also, if we had produced a bunch of lower API oil, I’m sure the peakers would complain about that. In fact, that’s what they said we would only get…no more light sweet. And we are awash in it!

3. I’m not seeing the evidence for “Russia in decline”. It’s not on the curve, or in the geology. I don’t take a public pronouncement as meaning much. Russia is in cahoots with OPEC and wants to talk the price of oil up. Lot easier on them to talk about being in decline than to actually take their turn and withhold production.

4. Even one of y’all’s (Rune) looked at the shale oil producers and said that they are more and more self-funding drilling. Some debt loading of an asset play commodity production is normal and tax efficacious. The meme of “junk bond” kvetching is way over-rated. Those lenders know exactly what they are lending against and even have some big assets in the companies. Yes, if there is a price crash, they have a risk. I actually think the public equities is more the question of a bubble and even they have done well last few years. Drilling requires capital…have to get it from somewhere. If you’re growing, it’s hard to fund from cash flow.

5. Gail is a nice lady and writes a readable stick. But there’s a reason why she is in peaker circles vice an analyst at a bank or an oil company. This can make her feel important.

Davy on Fri, 25th Jul 2014 10:14 am

NOO, Noo, friggen get a life dude

NOO SAID – “1. I have no idea what a networked economy is. Is it like Amway? I think the economy or at least the principles of supply and demand, investment, etc. have not changed in last 50 years or so.!!!!!!!!!!!!!!!!!

I will not argue geology lacking the expertise but others here are going to wak you I am sure.

JuanP on Fri, 25th Jul 2014 10:37 am

I think it is highly improbable that the decline phase of oil production could be even in any way. It is more likely to be an irregular line with ups and downs, trending down in general. So in a way it is similar in that we will still have economic cycles, but we will be cycling down not up. Cliffs and plateaus is how I think it will play out. That’s my best guess right now.

JuanP on Fri, 25th Jul 2014 10:47 am

Short, please help understand the relationship here:

“If oil prices decreased significantly every sovereign state in the world would very shortly be bankrupt.”

I don’t understand why one thing implies the other. Do you mean because oil production would fall as a consequence of lower prices bringing down the global economy?

If so, that is a great point.

Davy on Fri, 25th Jul 2014 10:56 am

No doubt Juan. I often think about the PO dynamics of the interaction of production destruction and demand destruction. How will these two play out? They are symbiotic conditions. The one in control will dictate different economic outcomes. Yet, they are both an economic descent function. One influences supply while the other influences demand both causing inverse price reactions. Yet, both inevitably leading to the other in a downward spiral of the coming descent down the energy gradient. Am I just babbling Short and Rock? Sometimes I wonder if I know what I am talking about. It sounds good though.

JuanP on Fri, 25th Jul 2014 10:56 am

I also found an historical detail I was not aware of in the graph showing KSA’s and Russia’s oil production histories. After the collapse of the USSR, you can see an obvious symetric, complimentary line going in opposite directions. This means KSA made up for oil production decline in Russia in the nineties all by its lonesome by incerasing production very significantly. I don’t think KSA could save our bacon like that today.

Plantagenet on Fri, 25th Jul 2014 10:59 am

Gail purports to discuss oil production around the world, but nowhere does she mention fracking starting up outside the US. Fracking is just getting started in China, Russia, Australia, and the EU, not mention KSA. This could delay the peak for a while longer.

Northwest Resident on Fri, 25th Jul 2014 11:06 am

shortonoil — It seems to me that IF/WHEN oil prices drop very far and for a very long time (couple of weeks or so), that moment will be in synch with sovereign states either going bankrupt or in the beginning stage of going bankrupt (much like a banker who has just jumped off a tall building would be in the “beginning stage” of certain death during the first hundred or so feet of his plunge toward the concrete below).

Does that sound right? In other words, I am guessing that if/when we see those oil prices plunging, that will be the lead up to TEOTWAWKI.

JuanP on Fri, 25th Jul 2014 11:10 am

Davy, A downward spiral is an image I consider, irregular, kind of like a roller coaster at some points, maybe.

Going from demand destruction caused by high costs and prices that lead to lower prices that cause lower investments in E&P leading to lower future production that increases costs and prices leading to demand destruction. Rinse and repeat. All the way down in the long run.

Northwest Resident on Fri, 25th Jul 2014 11:16 am

Plantagent — You must not have read the articles and posts that explained clearly why fracking in other countries is not likely to ever get going to any significant degree. Here’s a few of the reasons for your review:

1) Unfavorable land use laws as opposed to private ownership in America which enables leasing of large tracts of land to fracking oil companies

2) Significantly denser populations in some countries

3) Inadequate or NO infrastructure (roads, pipelines, service companies)

4) Lack of investment funds required

5) Social instability in many countries

6) Lack of adequate water where fracking might otherwise be possible

There’s a few others that I missed. But that’s most of them, I think.

Give it up Plant — and let your friend Nony also know. Fracking is a blip in time, and that blip is fading out fast.

Davy on Fri, 25th Jul 2014 11:32 am

NR, I like the Wilie E. Minds eye better. The suicide banker minds eye has allot of blood and gore at the end of that fall. The cartoon just has road runner pooting and the great music. Why can’t life be like that after all?

eugene on Fri, 25th Jul 2014 11:48 am

All of this makes me think of a drunk who wildly denies any problem exists and has many stories of how all is well. Meantime, his/her life is sliding into oblivion as the person increasingly lives in a fantasy.

Northwest Resident on Fri, 25th Jul 2014 12:17 pm

Davy — Yeah, if only life was like a cartoon, no matter how far or how hard the fall, after the smoke clears we just stand up, brush it off and pick right up where we left off. If only.

Actually, I do theorize sometimes that life IS like that. As in, one day when I die, I’ll wake up (like waking up from a dream in the movie Inception), unplug myself from the dream machine having just thoroughly enjoyed (or not) the experience of living the life I am living right now, grab a smoke and a beer and start contemplating my next most excellent adventure. Maybe kind of like what happens in the move Total Recall also. It is a common theme/speculation — even Star Treck the Next Generation uses that idea when they step into the “fantasy room” (can’t remember real name) and just kind of teleport into a totally different life experience — except in that one, they know they are just living a fantasy.

Maybe it is really like that when we die? Maybe we just turn into worm food and that’s the end of it, period. I doubt the worm food part thought — doesn’t make logical sense to me, but I guess there’s only one way to find out for sure, and I’m going to try to wait a while before that happens!

Davy on Fri, 25th Jul 2014 12:29 pm

Yea, NR, quantum fantasy dream. We are right now living out an infinite number of lives or something. I think when you die your friggen dead. Like cold and lifeless. It is in the eternal moment of no beggining and no end only the now where the creative force exists and always has and always will. I am amazed how us Little more then erect monkeys put a human face to creation. Actually I will tell you after I am dead if possible. So NR if you hear noises some night I will signal 2 short taps and 1 long and you will know it is me.

Northwest Resident on Fri, 25th Jul 2014 12:48 pm

Davy — You’ll have to come up with a new signal — that one’s already being used. 🙂

In case you haven’t noticed, one of my favorite pastimes is speculation. I like to think of it as “informed and/or fact-bases speculation” — but others may disagree.

Here’s my speculation on life.

Life, like gravity, is something that exists everywhere. In order for gravity to do its thing, just a little mass is required and gravity immediately exerts its force on that mass. As with gravity, life is omnipresent just waiting for a chance to animate an otherwise inanimate cluster of biological material with life. For example, deep in the ocean trenches where chemistry is a churning cauldron of activity, eventually and randomly over a very long time there will be produced a structure that life can take hold in and wallah! A living organism is the result. I further speculate that a “life” is never destroyed, same as you can’t destroy gravity. It simply leaves the physical biological structure it has existed in and reverts back to “waiting mode”, depending on random chance to find another biological structure that it can “attach to” and so give that biological structure life. And finally, my speculation on this subject is that a life retains its individuality, it grows and learns and expands (or can go the other way too), and that the goal of all life is to achieve every greater forms to animate and give life to. Yes, I do believe in reincarnation — that is exactly what I am talking about.

Hey, I’m waiting for my test results to complete, so I have time to write this crap.

steve on Fri, 25th Jul 2014 1:14 pm

Short you may be right but you may be wrong…it is very difficult to predict economics and human behavior and if you do this…well then x will happen…We just don’t know! In 1971 Nixon put a cap on oil prices and rental prices to get re-elcted…did this help? I don’t know but he did get re-elceted….I wish I knew what is going to happen…..then I would stop kicking myself for wasting so much time on here and get out and live my life!

Davy on Fri, 25th Jul 2014 1:22 pm

NR, just like reading Chinese coin tosses that is as plausible as the bibles view because like as we may you are not going to describe totality with linear language. I mean hell we can’t even figure out the climate how the hell do we think we can have a corner on the sacred. Ok, as the old Indian said the dogs are going to sleep. I am done preachin

Steve, I agree short term but as Short always says the laws of thermo dynamics rule

bobinget on Fri, 25th Jul 2014 2:23 pm

Pemex Predicts Lowest Production in More Than Two Decades

Petroleos Mexicanos cut its output forecast to the lowest in at least 24 years as mature fields are shrinking faster than it had previously expected.

The forecast was lowered to 2.41 million barrels of oil a day from a prior projection of 2.5 million, said Gustavo Hernandez, Pemex’s head of exploration and production. This will be the Mexico City-based company’s lowest annual output since at least 1990, when it produced 2.55 million barrels a day, according to the oldest available government output data.

“We have been working to review the declines of each of our fields that contribute to national production,” Hernandez said today on an earnings call. “In the recent review, we obtained a better idea of the declines of the fields and have adjusted the production expectation downward.”

Pemex is counting on a landmark law enacted last year that opens Mexico’s energy industry to private competition for the first time since 1938 to help stem declining output. The entrance of foreign oil producers such as Exxon Mobil Corp. (XOM) and Chevron Corp. (CVX) will bring in $50 billion of annual private investment by 2020, according to Gabriel Casillas, chief economist at Grupo Financiero Banorte SAB.

“We want to reverse the decline in our oil production and need to invest more money in some of our projects,” Pemex Chief Financial Officer Mario Beauregard said in a July 9 interview in Mexico City. Pemex, which has identified potential partners, plans to move “very fast” in establishing joint ventures once additional energy legislation is approved, he said.

The passage of secondary legislation that sets a framework for oil and natural gas contracts is being debated this week by lower house committees after being approved by the Senate on July 21. The final bill will be sent to President Enrique Pena Nieto to enact it.

‘Biggest Challenge’

“We must redefine our future strategy as a value generating operator and not as a state monopoly,” Beauregard said on today’s call. “As CEO Emilio Lozoya has mentioned previously, Pemex faces the biggest challenge in its history” as the company transitions from a government monopoly to a competitive entity.

Pemex’s 2015 capital expenditures budget will be an estimated $29 billion, up from this year’s $27.7 billion, Beauregard said on the call.

The company’s net loss of 52.2 billion pesos ($4.02 billion) widened from a 49 billion-peso loss a year ago, the producer said earlier today in a statement. It is the company’s seventh consecutive quarterly loss. Sales increased 4.1 percent to 409 billion pesos.

Untapped Crude

The legislation will allow outside oil companies to help produce an estimated 113 billion barrels of untapped Mexican crude. Output from the third-largest crude exporter to the U.S. has fallen nine consecutive years because the company lacks sufficient funding and infrastructure to tap the biggest proven oil reserves in Latin America after Venezuela and Brazil.

The company produced an average 2.45 million barrels a day in the second quarter, Hernandez said on the call.

Pemex’s preliminary monthly crude production fell to 2.44 million barrels a day in June. Preliminary month-to-date output slid to 2.38 million barrels a day, below the new company’s forecast for the 2014 average.

To contact the reporter on this story: Adam Williams in Mexico City at awilliams111@bloomberg.net

To contact the editors responsible for this story: Carlos Caminada at ccaminada1@bloomberg.net Robin Sapona

bobinget on Fri, 25th Jul 2014 2:39 pm

Go, ask China, Mexico.

The US has so much oil we will soon be exporting the stuff. Who needs Mexico?

Mexico’s falling production, BTW, was the burning force behind Keystone XL.

Things are about to get more interesting before Christmas. Tired of Iraq already, our attention spans already frightened down to three minute sketches on YouTube, we can’t chew and walk thinking about

finding distraction.

You’ve heard about Friday ‘news’ drops?

http://finance.yahoo.com/news/why-us-oil-may-join-163430309.html?l=1

Keep moving folks, nothing to see.

rockman on Fri, 25th Jul 2014 3:00 pm

Juan/Davey – Jumping back to the earlier discussion re price drops vs production. Everyone understands the dynamics of new drills vs prices. Drop oil prices 30% for a significantly long period of time and a significant drop in new wells/new production is easy to predict. OTOH production economics of existing wells is ruled by two metrics: oil/NG prices and LOE…Lease Operating Expense. We haven’t talked much about LOE: it varies greatly from well to well. As little as $40,000/year or less for a dry NG well flowing on it’s own. At the other end an oil well that requires pumping and producing a high water cut might run $400,000/year. Getting rid of 200 bbls/day of salt water can cost $300k/year. That NG well might be generating $100,000/year cash flow so even if NG prices fell 30% it’s still netting a positive cash flow ($70k – $40k = $30k). But if that oil well is creating $500,000/year ($500k – $400k = $100k net income)? Now drop oil prices 30%: $350k – $400k = a $50k loss.

Actually many operators will suffer a small negative cash flow for a while. If they stop producing the well not only does the lease expire (usually in 30 days) but they’ll also have pay to plug and abandon the well: up to $50k or more. So they’ll foot the bill for a while.

And that’s a potential huge problem for the new Bakken and Eagle Ford Shale. Their initial flow rates might be high but within a few years the rates drop very lower. The LOE quickly eats up a significant amount of cash flow. Drop oil prices just a fair bit and thousands of such older wells, which may still be producing combined significant amount of oil, quickly become economical and are abandoned.

Some folks thought operators should have reduced the flow rates back when NG prices collapsed. In reality it’s more likely for most companies to do whatever possible to increase production: cash flow often becomes dominant over return on investment.

Thus the production from the new shale plays could fall much quicker in the face of lower prices then conventional wells from both a decrease in new wells and the abandonment of many producing wells.

JuanP on Fri, 25th Jul 2014 4:16 pm

Thanks, Rock. Once those wells are abandoned, they get plugged, and can never be used again, right? I haven’t seen LOE mentioned much at all since TOD days. Perfect reminder!

Nony on Fri, 25th Jul 2014 5:25 pm

1. How do you increase the flow of a NG well? Isn’t it unchoked after the first 6 months or so? [Honest question.] Would think you have to take what you can get…is there really an option to increase flow for an already completed well?

2. If dropping prices causes Bakken/EF to produce less, I don’t care. Don’t care if it is from less drilling or less flowing. What I want is lower prices. Not the #$%^ size bragging rights for production. Having LTO has helped prevent 150/bbl oil. But if peace breaks out in the ME and price crashes, I say to heck with Harold Hamm.

3. I don’t quite get, Rock, how the shale wells are more likely to be turned off from operating costs than conventional ones. The water cut in the Bakken is not that high. 30-50% OWR. Do you expect more or less water in a shale? (I would think less, since it’s not oil floating on water in a trap, but I don’t know, honest question.)

Davy on Fri, 25th Jul 2014 5:39 pm

Rock, I appreciate the significant details because we often talk in generalities. You have a way of grounding us like a rock foundation.

Makati1 on Fri, 25th Jul 2014 9:54 pm

Talking about peak oil is like talking about the weather. No one knows for sure what tomorrow will bring in either. You can guesstimate from past experience, but there are unknowns that can throw it all off. All you can do is prepare for the storm and hope it is a mild shower instead.

rockman on Sat, 26th Jul 2014 10:10 am

Davey – IT really isn’t that difficult. The trick is to not get drawn into debates about how many bbls are coming out of the ground. Instead just stay focused on the costs of oil and the damage it’s doing to the world’s economies.

Such as “Current oil price doesn’t seem too high”. Gave me a good laugh. Can you imagine any necessity you require daily increasing 300% and then saying the new price “doesn’t seem too high”? This is how the cornie propaganda tries to strengthen their argument. It really is a bush league ploy IMHO. LOL.

Davy on Sat, 26th Jul 2014 10:15 am

Yea Rock ask any CEO that price question especially one reliant on transport!

Davy on Sat, 26th Jul 2014 10:43 am

Then ask a CEO what he thinks about it personally? He won’t give a rat’s ass.

shortonoil on Sat, 26th Jul 2014 12:54 pm

“question for you – I posit that oil will be produced even when past 6.9:1 ratio as such oil will be used to help extract coal.”

6.9:1 is for the “average” barrel of oil. It is the point when the higher ERoEI sources can no longer subsidize the lower ones. The distribution of ERoEI’s for various fields (there are 48,000 of them) is not well know, so the amount that will be shut in is in question. It will be at least 50%, and could reach 75% of existing fields. Since there is a 1:1 correlation between oil production for the last century, and the economy it is definitely not going to be a good situation.

It is generally assumed that production will taper off gradually. It will for a few years, but sometime around 2030-2035 we hit what we call a “Point of Criticality”. That is the 6.9:1 point. It is where lower ERoEI fields will be shut in. Up until that point we will see a lot of lower quality fields being subsidized by higher ones. Shale is a good example of that happening today. Most of it is not full life cycle energy positive.

Up until the 6.9:1 point we will witness a continuing degradation of the world’s economy. The energy delivered to the general economy from petroleum is declining. That could produce a complete breakdown of the present system before the 6.9:1 point is reached. Our model does not extend into that area, so I can’t say for sure. What I can say for sure; we have some pretty rough waters ahead.

http://www.thehillsgroup.org/