There has been very little new data to report lately. The JODI, Joint Organizations Data Initiative, data for March came out a few days ago. JODI is very good as far as the data it reports goes. The problem is there is a lot of data they just don’t report. If a country does not report their production for a given month then JODI just leaves it blank. And some countries they can’t seem to get any data from, so JODI just gives them zero for every month. For those countries I just substitute EIA numbers.

As far as OPEC goes JODI is very political, reporting the inflated numbers that Iran and Venezuela report. I use instead the EIA data for those two countries. Anyway here is what I have from JODI. The Data is in kb/d, last data point March 2014:

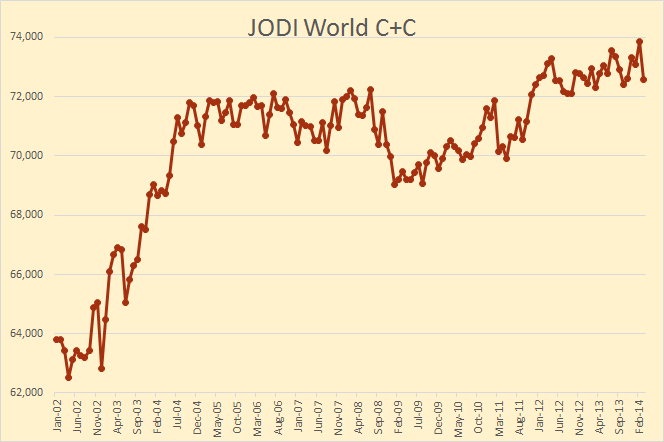

But for a few countries JODI is a pretty good data source. Russia is a good example.

JODI has Russia peaking, so far, in November at 10,127 kb/d and now about 100 kb/d below that point. Analysis have, for years, been expecting Russian production to decline but new fields in Siberia have kept inching up a little bit each year. But with over 60% of their production still coming from Western Siberia’s giant, largely depleted, fields it looks like that long overdue decline may have finally arrived.

This from 5 years ago: Russian Oil and Gas Industry Surprises Analysts

There are plenty of projects in Russia, both, new projects and existing brownfield projects. Russia is a very mature producer. If you exclude all the drilling activity taking place every year, then Russian organic decline in production is close to 19%. To compensate for that organic decline, Russia drills somewhere between 5,000 and 6,000 wells every year.

5,000 to 6,000 wells is a lot of wells. Most of that was just infill drilling. But they did bring on line their last giant in 2009, Vankor. Vankor is almost at full production of 500 kb/d. But with very little new oil coming down the pike, and infill drilling in their old giants beginning to peter out, it looks like the long expected decline in Russian oil production has finally arrived.

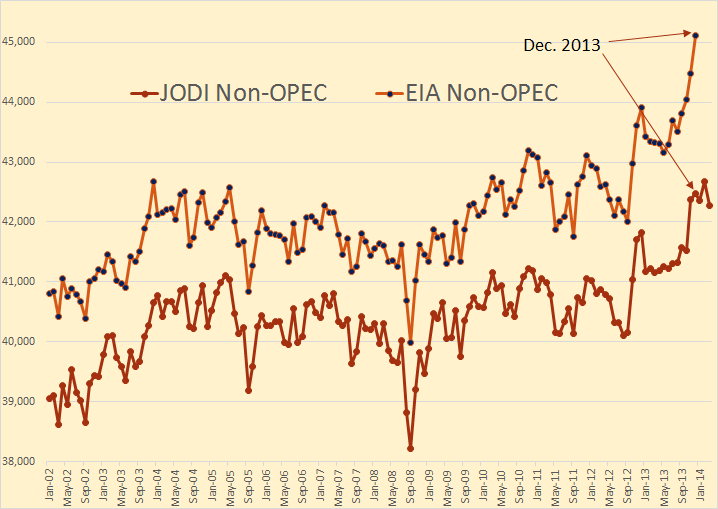

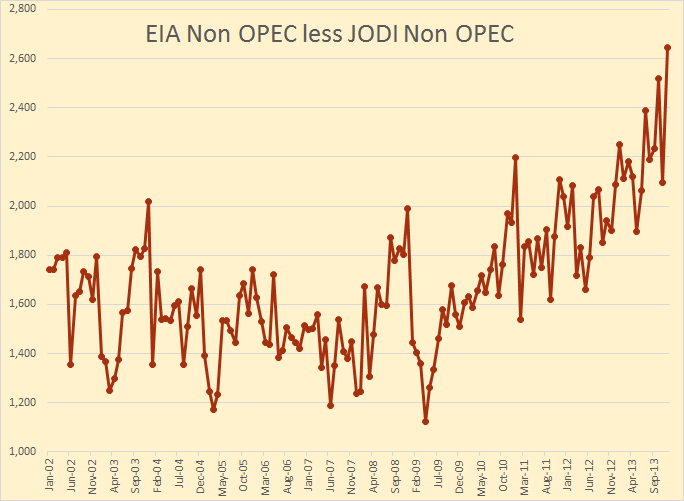

Here I have the EIA Non-OPEC C+C production versus JODI Non-OPEC production. Part of the huge difference between the two can be explained by a few very small producers that do not report to JODI. But only half a million bp/d or less can be explained because of that discrepancy. But…. this discrepancy is getting worse. The last data point here is December 2013:

Through 2007 the difference was averaging about 1,500 kb/d but since it has increased to around 2,400 kb/d. I don’t know if this is the EIA over reporting or Jodi under reporting.

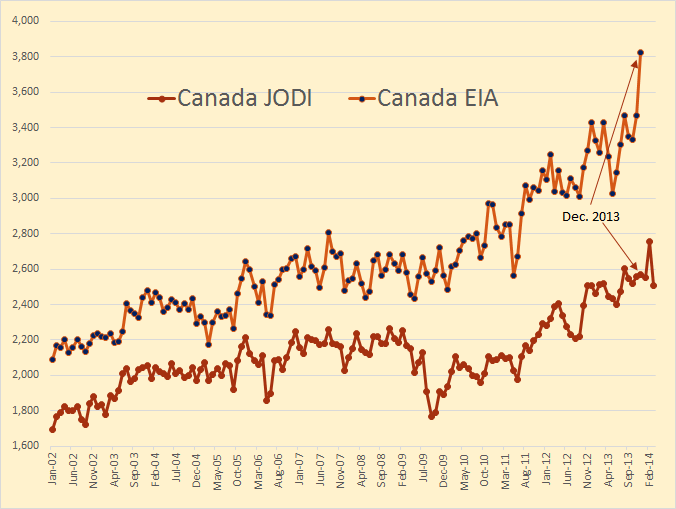

But the JODI data is two to three months ahead of the EIA data. The EIA data may be out next week with the January numbers. Then again those numbers may not be out next week. But one can get an idea of what some countries will do in the next three months. The last data point this and the next chart is March 2014.

The EIA has Canada up 133 kb/d in November and up another 354 kb/d in December. But JODI shows no such increase. Jodi shows Canadan production jumping in February then dropping back to even lower levels in March. Apparently there are some tar sands production that JODI does not count.

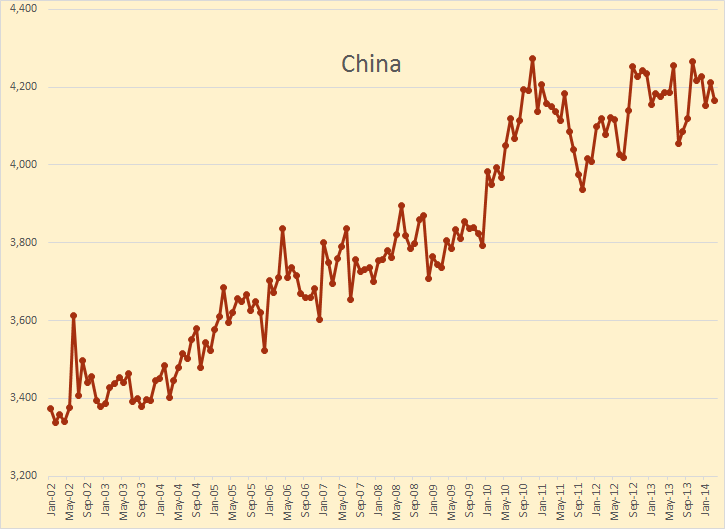

China appears to be on a plateau, not up and not down. But they are 110 kb/d below their peak in November of 2010.

shortonoil on Sat, 24th May 2014 8:35 am

Most of this data results from self reporting by the producing countries; but there are huge political, and economic consequences for a nation that is dependent on oil production to report a decline. For that reason we believe that the production data being reported is optimistic by several million barrels per day. Our model places conventional world crude production at 64 mb/d.

http://www.thehillsgroup.org

bobinget on Sat, 24th May 2014 11:03 am

In failed states (Syria, South Sudan or Libya), because oil exporting is constricted, PO is on temporary hold.

Eventually, either most combatants are dead or sicken of war, oil exports slowly resume. If the US had not invaded Iraq a decade ago, Iraq would by now have peaked. Sanctions place on Iran had similar effects.

Mismanagement in Venezuela is responsible for that great nation’s export decline. Unfettered corruption in Nigeria has forced oil companies to slow or stop on-shore production. My point, oil is still in the ground.

As it happens Iraq, Iran, Venezuela, China, Syria, Yemen, Qatar, Libya, Russia will constitute new cartels, currency baskets and trading partnerships.

Saudi Arabia will continue to be guardians of Mecca.

Others on Sat, 24th May 2014 12:23 pm

http://www.fool.com/investing/general/2014/05/24/chevron-corporation-backs-oil-price-projection.aspx

Chevron’s production in 2014-Q1 went down by 2%. Oil majors are struggling to maintain their production.

We don’t know as how they can match the rising Auto Sales and Oil Consumption from developing world.

Plantagenet on Sat, 24th May 2014 12:36 pm

@Others

Chevron and Exxon and other oilcos aren’t going to be able to match rising auto sales and oil consumption. Their oil production is going to continue to go down, not up.

Thats what peak oil is all about. Oil production is going down.

Ron Patterson on Sat, 24th May 2014 12:46 pm

Shortonoil,

I cannot really agree with your assessment as most countries are showing a decline in production. World C+C, according to the EIA, was 76 million barrels per day last year. I fail to see how it could be 10 million barrels lower and no one really notice.

J-Gav on Sat, 24th May 2014 1:15 pm

Ron and Short – You have a point Ron, but then again the EIA has been notoriously out on their predictions/calculations over the years. Have they gotten better recently? Still, Short, 64 does seem like a pretty low number. We all know reserves data is widely skewed but production should be easier to track or am I missing something?

shortonoil on Sat, 24th May 2014 3:55 pm

What was quoted was conventional crude, not C+C. We do not use condensate in our calculations because the energy content of it (about 107,000 BTU/gal) is too low to make much difference in the powering of the economy. Even West Texas is quoted as putting conventional crude at 67 mb/d. We think that even that is a little high. With the US, and Russia mainstreaming condensate into their refinery input, 3 mb/d would be quite easy to hide.

http://www.thehillsgroup.org

northwestresident on Sat, 24th May 2014 8:38 pm

“With the US, and Russia mainstreaming condensate into their refinery input, 3 mb/d would be quite easy to hide.”

You can bet that one of the reasons so much effort and wasted money is being put into fracking is to produce enough “oil” so that when that “crude” is added to the total, it looks like we are maintaining or even slightly growing world production. It is all about maintaining the illusion that BAU is on solid ground from an energy standpoint. And why would they go through so much effort and subterfuge to keep everybody thinking that we’re doing just fine? Good question. It probably has something to do with not wanting the stock market to crash, trying to prevent credit from drying up up and trying to prolong the time before the world as we know it comes to an end.

shortonoil on Sun, 25th May 2014 12:56 pm

There are several practical reasons to keep the shale game going. One is the necessity to keep the pipe lines full. A barrel of oil traveling from the Canadian border to a refinery in Houston takes 35 days to make the trip. If volume falls transportation time would have to increase, thus cost would increase. The other is that shale, although only about half of it is suited to make transportation fuels, keeps the price of crude suppressed. We have calculated that this saves refineries about $76 billion per year in raw material costs. Even at a production cost of $1.67 to produce a $1.00 worth of product (our determination) it would pay the petroleum industry to subsidize shale if necessary. Finished product exports are very important to the general economy, and supply a large number of high paying jobs. Shale gives the US refinery industry an edge in the global finished product market.

Shale production provides significant benefits to the economy in the short term, but energy independence is not one of them! That was a little meme thought up to keep Joe Six happy while his water was getting polluted, roads destroyed, and climate heated up. There is nothing personal in all of this, its just business!

http://www.thehillsgroup.org

Davy, Hermann, MO on Sun, 25th May 2014 6:08 pm

Short, my thoughts also. As long as our economy can subsidize liquid fuels we must or the game is over. The game will be over anyhow but it would be nice to buy us a few more years to make some kind of transition effort.

northwestresident on Sun, 25th May 2014 6:36 pm

Davy — How long can they keep it going, that’s the only question.

shortonoil — Based on the info in your previous post, it looks like refineries and their well paid employees are profiting from the shale boom. But oil companies — the ones who actually get the oil out of the ground — are losing money, badly — or so I read. And I remember rockman pointing out in one of his posts that service companies are doing just fine with the fracking boom. I wonder if the losses being incurred on the fracking/extraction end get made up for or compensated by the profits earned in refining and service? Is somebody at the very top somehow making a little money on fracking (refining + service – extraction), or is it still net total a financial bust burning more money than it is making. Just curious…

Davy, Hermann, MO on Sun, 25th May 2014 6:59 pm

N/R, I feel the weak link is the financial system with its systematic implications. The liquid fuel subsidy probably can continue a few more years. There is just enough conventional crude in the market. The financial system is being forced through repression of the cost of money, repression of price discovery, and a herd of blind bulls believing fairy tales. This financial fantasy can continue until it can’t. Yet, it is anyone’s guess these days. We are entering uncharted territory with dysfunction, irrationality, and diminishing returns. Any of a number of tipping points are ready to break equilibrium. Once a serious break occurs many more tipping points are ready.

northwestresident on Sun, 25th May 2014 7:46 pm

Davy, when you write “There is just enough conventional crude in the market.”, I agree. For now. And yet, we read all these articles predicting increasing demand over the next few years, millions of barrels more than today’s total production. As demand increases, the oil companies I believe are going to have a very difficult time meeting that demand. Which means, most likely, demand destruction is the only solution — more people unemployed, higher prices for everything and food especially. Those demand destruction policies are probably in play right now, grinding away, making everybody but the highly invested 1% poorer by the day. You just have to wonder, how long can it drag out before something big happens. Maybe for a long time, maybe not. A few more years seems possible, but not likely to me. I guess all we have to do to find out is just hunker down and wait!

Davy, Hermann, MO on Sun, 25th May 2014 9:20 pm

I agree NR, demand destruction or in other words wealth transfer. I still think we have a few years but I am preparing for your “near term collapse” predictions. We both know this thing could blow any day or limp along 5 years!