Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on March 11, 2014

The EIA’s Drilling Productivity Report, Ghana and China

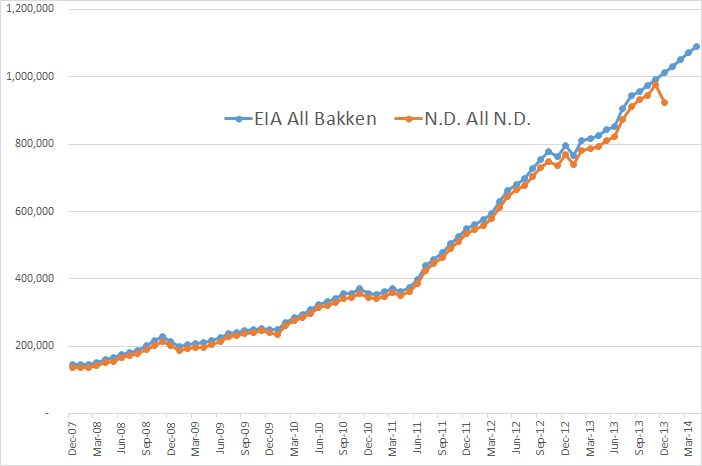

The EIA’s latest Drilling Productivity Report has been published. I found some strange things in the report. For the Bakken, their data does not jive with that posted by North Dakota. I have plotted the two together. The North Dakota includes all North Dakota but not the Montana part of the Bakken. The EIA data includes all the Bakken but not the non-Bakken part of North Dakota. Almost a wash but not quite. Montana produces slightly more than the non-Bakken part of North Dakota, but not very much. Anyway…

I thought for sure that the EIA would hear that Bakken Production was down about 50,000 barrels per day in December. But Nooooo… they have the Bakken up by over 20,000 barrels per day in December, a difference of 70,000 bp/d. But up until the last two or three months they follow the North Dakota data pretty close so we can hope they update their data in a few months.

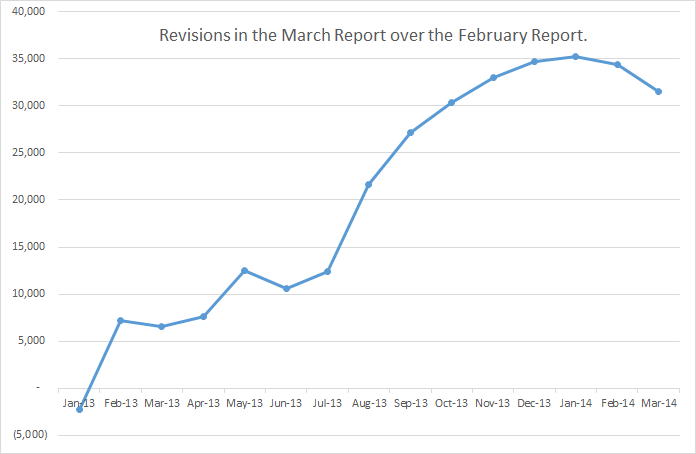

However all LTO production was revised upward in this last report. The chart below is the barrels per day that all tight oil was revised upward.

Doesn’t the strange shape of that chart raise suspicions? December production was revised upward by 34,672 bp/d when it actually should have been revised downward by perhaps twice that amount. January production was revised upward by 35,243 barrels per day. I doubt very much that this was the actual case.

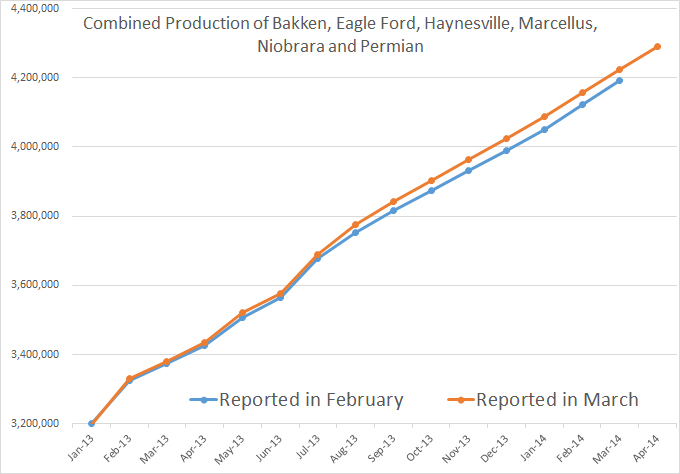

The chart below is total LTO as reported by the EIA’s Drilling Productivity Report. Of course it is not nearly that much because a lot of conventional oil is included, especially in the Permian.

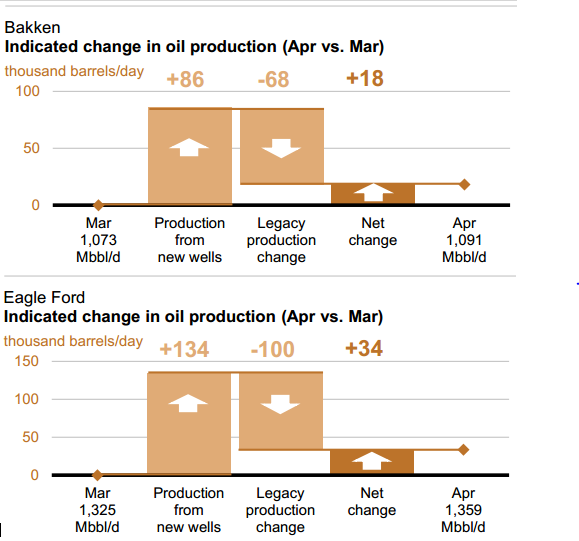

I had to include these decline charts published by the EIA.

They are saying that in April, in the Bakken, 86 kb/d of new oil will be produced but there will be a decline of 68 kb/d leaving a net increase of 18 kb/d. And as you can see they are predicting a similar pattern for Eagle Ford.

Oil Production Plunging in Ghana

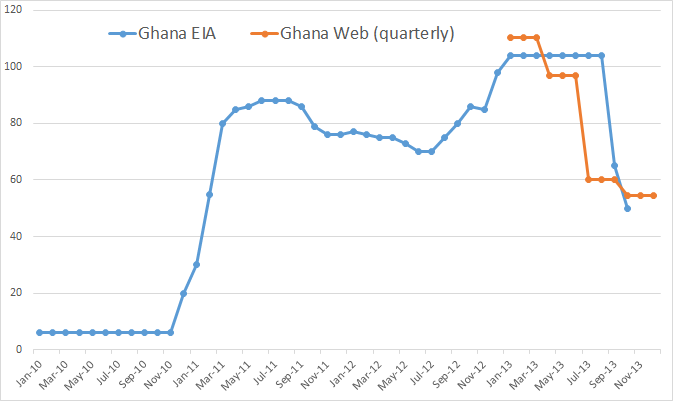

The third year of oil production in Ghana, precisely in the Jubilee fields, has ended and the economy of Ghana is reeling with the Cedi in a free fall. The economic consequences of this free fall are common knowledge, down to the common man in the street, because of the biting effects.

The Cedi is of course Ghana’s unit of currency. This shows what happens when a country has oil, then doesn’t, or doesn’t have nearly as much.

Tullow Oil Ghana, which owns 49.95 percent of the action in Ghana’s Jubilee field, denies this drastic drop in production but Ghana Web says they get their data from the quarterly per barrel royalties that the oil companies pay to the Ghana government. Apparently that’s where the EIA gets their information also, albeit a bit delayed. The EIA’s data is C+C where the royalties are apparently paid on “Barrels of Oil Equivalent”. That likely accounts for the difference.

What makes this development so alarming is the fact the Jubilee Oil Field was supposed to hold 2 billion barrels of proven reserves. It is yet to produce even 100 million barrels or one twentieth of that amount. What does this tell us? Likely two things, that early assessments of reserves are not to be trusted. These assessments are based, at least partially, on test well flow rates. And that the decline rate of these small deep water fields can be swift and sudden.

There was a lot of talk these last few days about the first ever China bond default. I am of the opinion that things are about to start popping in China.

Whistling Past The Graveyard After China’s 1st Ever Bond Default

If the economy continues to erode, there must be a series of defaults. Expect troubles soon, especially in the second half of this year. Haitong Securities, China’s second-largest brokerage, estimates that 5.3 trillion yuan of trust products will come due this year.

“In the U.S., it took about a year to reach the Lehman stage when the market panicked and the shadow banking sector froze,” the Bank of America Merrill Lynch note pointed out last week. “It may take less time in China as the market is less transparent.”

And it may have already started.

Disappointing China exports halt stocks, hammer commodities

Investors in Asia started the new week on a cautious note as China’s exports unexpectedly tumbled 18% year-on-year in February, swinging the trade balance into deficit and adding to fears of a slowdown in the world’s second-largest economy.

Note: I send out an email notification to about 110 people when I have published a new post. If you would like to be added to that list, or your name removed from it, please notify me at: DarwinianOne at Gmail.com

4 Comments on "The EIA’s Drilling Productivity Report, Ghana and China"

Northwest Resident on Tue, 11th Mar 2014 3:00 pm

Speculation on China’s financial implosion is rampant, and it seems to me, with very good reason. Chinese economic growth has been the primary engine of growth for the world economy these last few years, resulting in so many financial and stock market bubbles that the air is thick with them. Now we see one of those bubbles pop, and the financial/investment community freaks out — with good reason. Because that first bubble popping is a very good indicator of when the rest of them will start popping — it means those thousands of bubbles floating around are all going to start popping any moment now, and that IS something to worry about.

Northwest Resident on Tue, 11th Mar 2014 6:33 pm

A little more collaborating info on just how bad it is going to get in China:

“Magic” Collateral: A Frank Look At The Sheer Credit Horror About To Be Unleashed In China

While the world is terrified about what China – where corporate bond defaults are now permitted – may be about to unleash on the world, most are all too happy to remain in a state of delightful ignorance. We decided to take a peek behind the scenes.

Recall that as we have repeatedly shown in the calendar of coming Chinese bond default, on March 31, a borrower named “Magic” (no comment) is set to default on a CNY196 million Trust.

The default may or may not happen, as there is always a high likelihood it will simply be bailed out as has happened frequently in the past, but regardless of the final outcome, here is what is really going on behind the scenes. From Bank of America:

31 Mar 2014, Rmb196mn borrowed by Magic Property & arranged by CITIC Trust

Details: invested in an office building in Chongqing. The Chongqing developer ran into financial problems in mid-2013. CITIC Trust tried to auction the collateral but failed to do so because the developer has sold the collateral and also mortgaged it to a few other lenders.

Potential outcome: The developer and the trust company may share the repayment.

Reasons: 1) When CITIC Trust sold the product, it did not specify the underlying investment project. 2) The local government has intervened, fearing social unrest. A local buyer of a unit in the office building committed suicide as he/she could not obtain the title to the property due to the title dispute between the trust and the developer.

Please re-read that first part again:

CITIC Trust tried to auction the collateral but failed to do so because the developer has sold the collateral and also mortgaged it to a few other lenders.

So, “Magic” not only sold the collateral… but also mortgaged it to a few other lenders: lenders who count its as a perfectly performing asset when in reality they have zero claims to it. Did they steal that straight from the MF Global instruction manual?

Now add this:

“The local government has intervened, fearing social unrest. A local buyer of a unit in the office building committed suicide as he/she could not obtain the title to the property due to the title dispute between the trust and the developer.”

… and multiply by a few thousand for all the other shadow (and not so shadow) players who have engaged in precisely this kind of gross abuse of underlying collateral, which also happens to be the main reason why China can magically create trillions in debt out of thin air with zero collateral constraints, each and every year, no questions asked.

Well, the time to ask a question or two has finally arrived.

zerohedge dot com/news/2014-03-11/magic-collateral-frank-look-sheer-credit-horror-about-be-unleashed-china

GregT on Tue, 11th Mar 2014 8:18 pm

“means those thousands of bubbles floating around are all going to start popping any moment now, and that IS something to worry about.”

Or, perhaps all of those popping bubbles, is the solution to averting a runaway greenhouse event………..

Davy, Hermann, MO on Wed, 12th Mar 2014 12:19 am

Yeap, rehypothecation (twice posted collateral) is rampant in China. It is happening all over the world but in China it has been taken to new levels. In China collateral has been posted more than a few times. I have read that there are cases of 4 times posted collateral! Rehypothecation works great while the markets are up but just like margin calls when things go down it is ugly! The other financial problem with China is poor returns on investments. There has been far too many investment of all kinds that are not paying for themselves. This has been happening for some time and in the past it has been absorbed in the wider Banking system. China is a ticking time bomb for the global economy. Many Banks have exposure in China. Europe and Asia have the most exposure. The US much less but that does not matter because there will be cross contagions within the Banking system irregardless of where a bank is located. This also speaks of “moral hazard” so many bad deals were made in China because it was understood defaults would not happen so investments were ultimately protected by the state. Times have changed and expect some strange things to happen in China soon