Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on March 6, 2014

Reasons for our Energy Predicament: An Overview

Quiz: What will cause world oil supply to fall?

- Too little oil in the ground

- Oil prices are too low for oil producers

- Oil prices are too high for oil consumers leading to recession, debt defaults, and ultimately a cut back in credit availability and very low oil prices

- Oil exporters are subject to civil unrest and overthrow of governments, due to low prices and/or depleting reserves

- Lack of money (and physical resources that might be purchased with this money) to pull oil out of the ground.

- Pollution related issues–too much smog in China; too many problems with fracking; too many problems with CO2.

- The financial current system fails, and can only be replaced by one that allows much less debt. Oil prices remain too low under such a system.

In my view, any answer other that the first one is likely to be at least partially right. Ultimately, the issue is that to extract oil or any fossil fuel, we have to keep the financial and political systems together. These systems can be expected to fail, far before we run out of oil in the ground. Most oil in the ground (as well as most other fossil fuels in the ground) will be left in the ground, in my view.

Basing estimates of future oil production on oil reserves is likely to give far too high an indication with respect to actual future production. Even more absurd numbers come from using “resource” numbers (which are higher than reserve numbers) to make estimates of future oil production. Coal and natural gas production is likely to fall at exactly the same time as oil, because the problems are likely to be financial and political ones, not “resources in the ground” problems.

Direct Application of M. King Hubbert Theory is Incorrect

M. King Hubbert is known for his estimates of future oil production (1956, 1962, 1976) based on reserve amounts. There are two things of importance to notice about his estimates:

(a) The oil reserve estimates used are of free flowing oil reserves of the type that geologists currently were looking at. Thus, they were restricted to “cheap to extract” reserves, and

(b) When Hubbert showed graphs of world oil production following a generally symmetric curve (so downslope looks like a mirror image of upslope), Hubbert showed some other source of energy supply (nuclear in his early papers, solar in later ones) rising to high levels, before world oil production ever dropped. He even talked about making liquid fuels using a huge amount of energy plus carbon dioxide and water–in other words, reversing combustion (1962). In order to ramp nuclear or solar up to these very high levels, they would need to be extremely cheap.

The assumptions that M. King Hubbert makes are effectively ones that would allow the economy to continue to grow and the financial system to “hang together.” If a person looks at today’s situation, it is quite different. We do not have an alternate fuel supply that will allow the economy to continue to grow, regardless of fossil fuel consumption. The published reserves include large amounts of oil in the ground that are not of the very cheap to extract type. Extracting such oil will be impossible if oil prices are very low, or if credit availability is lacking. It is tempting for observers to look at oil reserves and assume that all is well, but this is definitely not the case.

Basic issue: Future oil extraction and future substitution is uncertain

One basic issue is the “iffiness” of the reported reserve and resource amounts:

There is lots of oil in the ground, if we can actually get it out. Getting it out requires a combination of a financial system that allows us to do this (high enough prices for producers, adequate credit availability for producers, equity investment available if credit is not available, buyers who can afford the products) and political system that allows this to happen (citizens in countries with oil extraction not rioting for lack of food; banks open in countries trying to import oil; adequate trade connections among countries).

Likewise, substitution is possible among energy products, if it is possible to overcome the many hurdles involved in doing this. There are two cost hurdles: the higher ongoing cost of the substitute and the transition cost. The transition cost gets to be very high if there are a lot of “sunk costs” that are lost–for example, if citizens are forced to quickly change from gasoline powered cars to electric cars, so that the resale value of their gasoline powered cars drops precipitously. There is also a technology hurdle: we need to have the technology to enable using the different energy source.

If the cost of the substitute is higher than the cost of the original energy source, a change to the substitute will tend to make the economy shrink, because wages will “go less far”. If citizens need to pay a whole lot more for new cars, or if electricity is more expensive, citizens will cut back on discretionary expenditures. This cut-back on expenditures will lead to layoffs in discretionary sectors, and will make it more difficult for the government to collect enough tax revenue.

Another basic issue: Wages don’t rise as oil (or energy) prices rise

Economists would like us to believe that we just pay each other’s wages. Wages can rise arbitrarily high independently of actually creating goods and services using energy products.

Unfortunately, this doesn’t seem to be true in practice. Based on my research, in the US high oil prices are associated with flat wages, in inflation-adjusted terms. Wages do not rise as fast as oil prices. Instead, wages tend to rise when oil prices are low, making goods and service affordable.

Part of the problem with rising oil prices is that they radiate through the economy in many ways: in higher food prices, because oil is used to produce and transpire food; in higher metal prices, because oil used in metal production; and in higher finished products, such as automobiles and new homes, because they use oil in their production. With wages not rising sufficiently, as oil prices rise, workers find they need to cutback on discretionary goods. The result is recession and job layoffs. I document this issue in the article Oil Supply Limits and the Continuing Financial Crisis, published in journal Energy in 2012.

The flip side of this issue is that without wages rising as fast as the cost of oil extraction, it is hard for the selling price of oil to rise high enough to provide an adequate profit margin for oil producers. It is inadequate oil prices for oil producers that seem to be the current problem. I talk about this issue in two recent posts: What’s Ahead? Lower Oil Prices, Despite Higher Extraction Costs and Beginning of the End? Oil Companies Cut Back on Spending.

Economists don’t think that prices can remain too low for oil producers. It can happen, because their model of supply and demand is not correct in a world with energy limits. Even if prices temporarily rise again, recession hits again, and we are back to low prices again.

Another basic issue: Diminishing returns

Diminishing returns occurs when it takes more and more energy or other resources to produce the same amount of goods. In the case of oil supply, we reach diminishing returns because companies extract the easy-to-extract oil first. Thus, the price of oil rises because the oil that can be produced cheaply is mostly gone. If we want to obtain more oil, we need to extract the more expensive to extract oil.

One way to see what diminishing returns does is to think about an economy producing two kinds of goods and services:

- The goods and services the consumer really wants–such as food, fresh water, transportation that takes the consumer from door to door, electronic goods, and housing that meets the person’s needs.

- All of the intermediate “stuff” that goes into making the end products in (1).

What happens with diminishing returns is more and more of society’s physical labor and its resources go into intermediate products, leaving less and less to produce end products, and less to actually “grow” the economy. In some sense, it is as if we are becoming less and less efficient at producing final goods and services. In my view, this is a major reason why wages stop rising as oil prices rise, and as other energy prices rise.

Another basic issue: The rate of growth in energy supply is closely tied to the rate of GDP growth

We use energy to make goods and services, so it stands to reason that using more energy would lead to more GDP growth. Economists don’t necessarily agree. They are sometimes of the view that the connection has only to do with “Demand”–in other words, when the economy is growing rapidly it needs more oil and energy products to support it its growth. I discuss Steve Kopits’ talk on this subject in Beginning of the End? Oil Companies Cut Back on Spending.

Something that is perhaps not obvious is the fact that cheap energy supply tends to easier to ramp up than expensive energy supply. Cheap energy supply requires relatively less investment. Goods created using cheap energy supply tend to be inexpensive, making them easier to sell to consumers and more competitive in the world market. I talk about these issues in Oil Limits Reduce GDP Growth; Unwinding QE a Problem.

Another basic issue: The role of debt

Long term debt plays an extremely important role in the economy, because it allows consumers to buy expensive goods like houses and automobiles that they could not otherwise afford, and because it allows businesses to invest in projects before they have saved up sufficient profits from past projects to fund the new projects. It also allows governments to spend more money than they have in tax dollars. All of this purchasing power tends to prop up the price of commodities such as oil and metals, making it feasible to extract them.

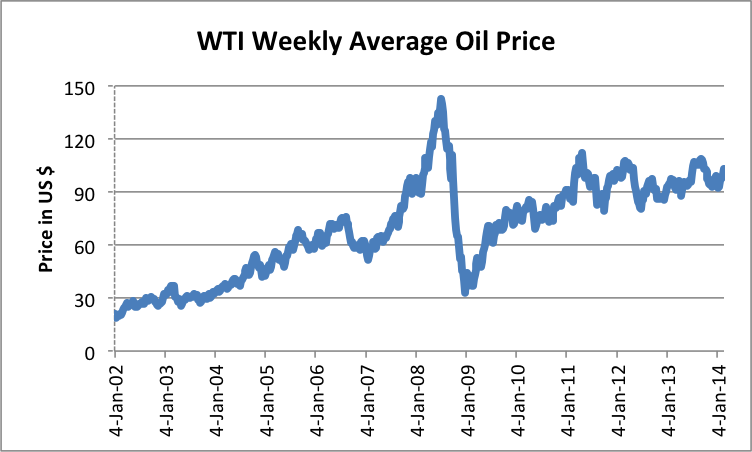

We had a chance to see how important a role debt plays in 2008, during the debt crisis in the second half of the year. During that period, the price of oil dropped from briefly hitting $147 barrel to the low $30s range. Major banks needed to be bailed out, and the insurance company AIG was taken over by the US government because of problems with derivatives.

Figure 1. Average weekly West Texas Intermediate “spot” oil price, based on EIA data.

The big drop in oil price in 2008 was due to a drop in oil demand because of lack of credit availability. I wrote an article in 2008 about the huge impact this decrease in credit availability had on energy prices of all kinds, even uranium.

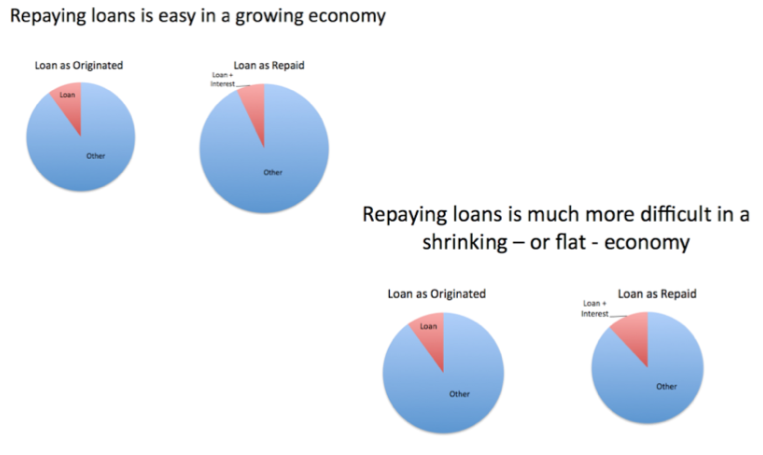

A related concern relates to the fact that “borrowing from the future” — which is what we do with long-term debt, is a great deal more feasible in a growing economy than it is in a shrinking economy. There are a lot more defaults in the latter case, because people keep losing their jobs and businesses keep closing.

Figure 2. Repaying loans is easy in a growing economy, but much more difficult in a shrinking economy.

The concern I have is that as economic growth slows, we will reach a point where long term debt becomes very hard to obtain. The lack of credit in 2008 has not been fully fixed. It was only with the help of Quantitative Easing (QE), which added more demand to the marketplace because of very low interest rates, that oil prices have been able to rise again after the drop in 2008. With the very slow economic growth we have been experiencing recently, it has been necessary to use QE to keep interest rates low enough that people can still afford to buy homes and cars.

If the economy shifts from adding debt to subtracting debt, we are likely to see a huge drop in oil prices, perhaps similar to the drop in oil prices in 2008 to the low $30′s range. If this should happen again, it is not clear that the Federal Reserve would be able to find a way to make the price rise again because is already using a huge amount of stimulus, and thus has fewer options left.

If oil prices drop to a low level and stay down, a large share of oil production will be discontinued. Very little new drilling will be done. Similar effects are likely to happen for other fossil fuels and for mining for metals as well. Such a drop in oil production is likely to be steep–at least as steep as when the Former Soviet Union collapsed. Oil production dropped by about 10% per year, and other energy use dropped rapidly as well. Customers such as the Ukraine and North Korea saw even steeper declines in their oil imports.

Another basic issue: Government funding

Governments are only possible because of the surpluses of an economy. Greater surpluses allow more government employees and more services. Mario Giampietro (2009) is one researcher who writes specifically about this issue. Furthermore, as an economy grows, rising tax revenue makes it is easy to add more programs and services.

As an economy reaches diminishing returns, studies of past economies show that inadequate government funding is one of the major bottlenecks. This occurs because falling resources per capita leads to increasing disparity of wages, with new workers finding it difficult to find good-paying jobs. Governments are called on to provide more programs at precisely the time when their ability to raise sufficient funds to pay for these programs is lacking. A major factor leading to collapse is the inability of governments to collect sufficient taxes from increasingly impoverished citizens.

The Two Way Escalator Problem

As I see it, the economy as it is currently constructed only gives us two options: up and down. The markers of the “up escalator” are

- Cheap energy

- Growing energy supply

- GDP growth

- Wage growth

- Debt growth

- Growing government programs

The markers of the “down escalator” are

- Expensive to produce energy supply

- Energy supply grows slowly

- GDP Growth lags or declines

- Wages lag

- Outstanding debt tends to shrink

- Increasing inability to fund government programs

The two deal-killers with respect to these two escalators are

- Moving from debt supply growth to debt supply shrinkage. This is like moving from Keynesian economics to the opposite. Or from getting a credit card with a large available balance, to having to pay back old credit card debt without adding new debt.

- Increasing inability to fund government programs

The above two reasons are why I expect financial and governmental problems to lead to the end of our current system. Diminishing returns is already leading to higher oil prices, and thus moving us from the up escalator to the down escalator.

I am doubtful we can reestablish very widespread use of long-term debt after a collapse because by that time, the economy will clearly be shrinking. A person often hears people talk about getting rid of the fractional reserve banking system because it requires growth to maintain, but in fact, having such a system has been very helpful in enabling extraction of fossil fuels and allowing the economy to use metals and concrete in quantity. The availability of bonds for financing has been helpful as well.

One essential part of today’s economy is very long supply lines. These allow very complex products to be made, using supplies from all over the world. What we found in the 2008 credit crisis is that many businesses (both large and small) in these supply chains were hit hard by lack of credit availability. I see this issue as being very difficult to solve. If it cannot be solved, we will be faced with making goods locally using smaller companies and very much shorter supply lines. It would be a different system than we have today, and would likely support a smaller world population.

A lot of “peak oilers” would like to think that somehow it is possible to “get off at the mezzanine,” and have a viable economy similar to today’s with a small amount of expensive renewables, plus a continuing supply of fossil fuels. I have a hard time seeing this actually happen. One problem is the likelihood that fossil fuel supply will decline quickly because of low price. Another potential problem is a major cutback in credit availability making transactions difficult; a third issue is governmental problems, as taxes fall short of what is needed to fund programs.

We could in theory get back on the up escalator if we find alternative fuels that meet all of the required specifications–very cheap; available in huge quantity, expanding year by year; can be transformed to a liquid fuel similar to oil; and non-polluting. This seems unlikely right now.

Otherwise, what we do have is all the “stuff” we have today, for as long as it lasts. The economy won’t stop on a dime. We also have the ability to recycle things that we can no longer use, that might be more helpful in another place. Solar panels that people currently own will continue to function for a while (especially off-grid), and the grid will probably continue for a while. We know that many people lived in local economies, before we had fossil fuels, and it is likely to be possible again. We certainly live in interesting times.

26 Comments on "Reasons for our Energy Predicament: An Overview"

Makati1 on Thu, 6th Mar 2014 2:44 pm

Most of our modern world only exists because we had excess, cheap energy for the last 300 years to build it with. But, for the West, it is coming to an abrupt end as consumers are starting to be unable to consume. It will spread to the 3rd world eventually, but will be a lot less painful for those who never had anything to lose.

I take that back. It IS hurting the 3rd world because the West thinks all world resources are theirs and the rest of the world doesn’t count. It’s going to be a long, hot summer.

action on Thu, 6th Mar 2014 3:53 pm

The constraint on oil supply won’t allow the credit issuance that economists are trying to make. Spiking oil prices effectively block the effects on increasing debt. In other words, despite currency a plenty, the constraints on oil extraction block world GDP growth. There’s nothing they can do to prevent ultimate collapse, whether the price of oil is 30 or 300, spiking prices are indicative of the machine sputtering from lack of fuel.

rockman on Thu, 6th Mar 2014 3:59 pm

Again someone trying to mischaracterize Hubbert’s work to suit their agenda. Not that I disagree with his general tone but he is very wrong in one area:

“M. King Hubbert: There are two things of importance to notice about his estimates: (a) The oil reserve estimates used are of free flowing oil reserves of the type that geologists currently were looking at. Thus, they were restricted to “cheap to extract” reserves, and (b) When Hubbert showed graphs of world oil production following a generally symmetric curve (so downslope looks like a mirror image of upslope”

Hubbert clearly states that his prediction was only for those EXISTING TRENDS that his statistics were based upon. He specifically says his projection does not include future yet undiscovered trends. And one reason his projection was so accurate was the simple fact that the trends he analyzed were very mature and would have been producing for many decades by the time the peak arrived. The boom in Deep Water and shale production don’t contradict his projection because they weren’t a portion of his model. And those fields were not “cheap to extract” based upon the economics at the time. They were typically much larger than the remaining undiscovered fields left in the country today but not necessarily cheaper or easier to find. In fact today’s success rate is much greater than it was even 30 years ago. The problem is that there are few fields left to discover. BTW some of the fields Hubert used for his statistics were producing from unconventional reservoirs.

The backside of the curve: if one takes the time to read the original work you’ll see that Hubbert specifically said the curve would not be symmetrical. In fact, he tells why he’s hesitant to even make a guess. And it’s easy to understand why he took that position: virtually every production curve, from an individual well to an entire trend or even a country has never produced a symmetric production curve. Never. The tail end always declines much slower than production ramps up. IOW the second half of the recover takes significantly longer than the first half. When looking at a field, a trend or even an entire country there has never been a “cliff” experienced in oil/NG production rates. Of course since there is no specific definition for a “cliff” one could argue that point till the cows come home.

ghung on Thu, 6th Mar 2014 4:45 pm

@Rock – Part of what I get from Gail’s article is that Hubbert’s model relied on geological and technical factors, were as economic considerations have become more of a major player. In the big picture, it doesn’t matter if a play (or country) has a long or short production tail when the costs of replacing declining current production exceeds a market’s ability or willingness to do so.

With so many other excessive claims on an ever more leveraged financial system, Gail’s position is that the overall decline could be steep indeed, as the complex systems required to bring oil to markets fall apart. As Kopits pointed out in his recent lecture, that seems to be happening now. I personally think that oil production, at a global scale, has a MOL, a point where things begin to fall apart and become more local; not a cliff perhaps, but a steep decline.

Nony on Thu, 6th Mar 2014 4:49 pm

I think part of the problem is that a country can have very different dynamics than a field. For instance: X barrels of cheap oil, 2X barrels of expensive oil. So when you look at the country, you will see a classic Hubbard peak for the initial cheap oil, followed by a decline. Then when WORLD price goes up, you’ll see production turn back up and go even higher than before.

Part of the problem is that many Hubbard enthusiasts hold out examples like Texas or USA as classic Hubbard peaks (to an extent Hubbard did this also). However, you can point to examples like Canada, where the shape was more like I discuss. Even the USA may repeak.

I actually think a “depletion advocate” should not be held to such a strict standard of wanting Hubbard peaks, of ignoring price, ignoring disparate resource types within a country, etc. But you can’t have it both ways. The classic Hubbard view (with linearization and all that) doesn’t work too good. A squishier, more moderate Peak Oil Dynamic works better.

Then again, I go back to Hoteling’s rule (for pricing of depleting resources) and the MIT paper that talks about the supply curve moving left with depletion and right with knowledge.

Reading the Wikipedia article (mostly written ~2005-2008) is kind of a hoot. They talk about how a field has a Hubbard peak, and then a basin, and then a country. And that the world will also. And hold out Texas and USA as examples and show those classic faux Gaussian curves. But when people update the numbers, they don’t fit the story.

@Rock: don’t be mad about people being mean to Hubbard. He was a great intellect for sure. But had his limits. You are a big talker about price and have seen some booms AND busts. He was weak on the integrated problem…a hardcore “what’s in the rocks” geologist, but not a thinker about technological evolution or about things like Hoteling’s rule.

Kind of a mean dude, too (I’ve been reading up on him.) He had a new young female colleague and the first thing he did was tell her not to have kids and make her calculate how long it would be until the Earth was shoulder to shoulder people. [He did not foresee the slowdown in pop growth rate that we have seen last few decades.] He made a great paper…not taking it away. But he was also affected by his personal bias. He was a Malthusian.

Davy, Hermann, MO on Thu, 6th Mar 2014 5:17 pm

I am in agreement with Gail on the tone of this article. The interconnectedness of the above and below ground factors in society’s growth engine are plenty evident now. I compliment these studies on the Peak Oilers for opening up the subject a decade ago. A healthy economy is as important as the products needed for economic growth. We are currently finding headwinds on the above and below ground factors in world growth. With these headwinds to growth we find systematic risk surfacing. Our complex global system is not constructed to accommodate decreasing growth. The whole basis of the financial system is debt based capital represented by money that when employed as capital with energy, labor, management, and equipment provides a return. This return covers the debt costs and allows growth of the money supply yet further leading to more growth. This is the fundamentals of our complex interconnected economic system. This whole equation is now distorted and dysfunctional. There is in fact negative growth if the net productive activity is looked at. You have to subtract parasitic economic activity and the biggest of these is the financial sector. It is far too big a percentage of the world economy and is in fact a wealth transfer mechanism bleeding the real economy. There are many other including the military, health care, education, and leisure. These pieces of the economic puzzle are fine in the right proportions but not in their current percentages. If the economic Ponzi scheme bubble were not enough we are also in the situation of limits to growth of the bellow ground factors. You have to admit we are reaching diminishing returns on the resources that are vital to our support system. The sweet spots have been used. We are beating the bushes and finding less quantity and quality sources. We are also in overshoot in our carrying capacity with respect to population. This limits our ability to control, educate, and provide for a growing population. If and when our social fabric develops serious failures it will spread systematically. This is most notable in regards to food and water. We are close to food water shortages in a wide range of countries. This reality can go on a few more years. The system is rigged and controlled from the top. There is much low hanging fruit. The wealth transfer can continue to cannibalize the bottom portions of the economic ladder. As long as confidence remains with those at the top the system can continue to build the house of cards. Time is not on the side of those at the top in the driver seat. All systems cycle in a finite world. We are seeing progressive damage to our global/local support systems the longer this dysfunctional situation continues. The destruction to our social fabric and economic structures multiplies with each passing month. There still may be a chance for a soft landing but this is fading quickly

Jerry McManus on Thu, 6th Mar 2014 5:51 pm

I agree with the previous comments about the “Hubbert bashing”.

I generally like Gail’s work, her analyses are usually pretty good, but for some reason she rarely misses an opportunity to “debunk” Hubbert. Not only is she wrong about Hubbert’s model, but it’s also pointless because it only detracts from her analysis. It’s kind of sad, really.

As Rockman pointed out, anyone who has actually read and understood Hubbert’s work knows that he went to great pains to stress that he was not making predictions about the shape of anything. His observation that the fossil fuel life cycle generally follows a bell-shaped curve should ONLY ever be seen as a “best possible case scenario, with all other critical factors functioning perfectly”.

And that’s not even his most brilliant insight, which routinely gets lost in the noise and which even the eggheads at the Oil Drum never really understood. Hubbert observed that, in the best case scenario, the area under the production curve eventually equals the area under the discovery curve. He never “predicted” what shape those curves would be.

Why is the area under the curves important? Because at some point the rising production curve crosses the falling discovery curve. At that point you can measure the time passed since the peak of the discovery curve and extrapolate the peak of the production curve after about the same amount of time has passed in the future, again in a best case scenario. This point also coincides with maximum reserves (actual backdated reserves, not politically reported reserves).

That’s it. No predictions. No obsession with the “symmetrical” shape of curves. Just a simple observation that when the production curve crosses the discovery curve you know enough about a mature producing region to make a pretty good guess about when the production curve will peak, all else being equal in a perfect world.

Hubbert used this observation to make a VERY good guess about the peak in mainland US production of conventional oil. He made a pretty good guess about world production a few decades later, but then the Iranian revolution followed by the Arab oil embargo put a huge crimp in world production and significantly flattened the curve from the “ideal” trajectory.

That unfortunate turn of events in no way whatsoever proved Hubbert “wrong”. It only delayed the inevitable peak in production by a decade or two. Right about now, as a matter of fact.

Nony on Thu, 6th Mar 2014 6:20 pm

I’m going to read those Hubbard papers (linked). I’ve read The PRize (20 years ago). Am reading The Quest (quite good, even if you are a Yergin hayter, just read it as a history of the oil industry last 20 years). REad The Frackers. Have seen a lot of good panel discussions from Rice and such. And I’ve hung around these peaker websites as well as Seeking Alpha, Google searches, Million Dollar Way blog, Drilling Info articles, USGS reports, etc.

There is a lot of good info out there. Not all just in this reposting site.

shortonoil on Thu, 6th Mar 2014 7:43 pm

Our projections put transportation fuels at about $10/gal by 2025. That same model gives petroleum prices between 1960 and 2009 with a $0 average deviation. At $10/gallon world trade will slow to a trickle of its present amount. Export nations like China, with 37% of their GDP dependent on exports will see their economies contract to a small percentage of their present size. Only the wealthiest of societies will be able to transport essential commodities like fuel, food and medical supplies any appreciable distances. It is reasonable to assume that financial systems, as we know them now, will no longer exist.

http://www.thehillsgroup.org/

Northwest Resident on Thu, 6th Mar 2014 7:46 pm

Gail may not have hit the nail directly on the head with her analysis of Hubbard’s analyses, but I think she did make one highly relevant and accurate point in regards to Hubbard’s predictions. That is, “The assumptions that M. King Hubbard makes are effectively ones that would allow the economy to continue to grow and the financial system to hang together.”

I’m no expert on Hubbard’s work, but as far as I can tell, Hubbard did not include the status of the global economy in his predictions. If it was ONLY about how much oil there is remaining in the ground and the technical ability to extract that oil, independent of finance and debt required, then it would be a different story. But Hubbard did not predict, and probably could not have predicted the dire financial situation that the world is in today. But it is that dire financial situation that is much more likely to impact “Hubbard’s curve” than the mere availability of oil and the ability to extract it.

Hubbard also did not include analyses of climate change/global warming in his predictions. When that generally symmetric downslope equates to pumping so much CO2 into the air that we set ourselves up for brutal punishment at the hands of mother nature, it might be a good idea to revisit that gently downsloping curve and re-compute based on new and urgent facts that affect it.

rockman on Thu, 6th Mar 2014 8:00 pm

All great points. But again I’ll emphasis that Hubbert’s prediction has not been proven wrong. In fact, just the opposite. He only predicted the future production curve of the EXISTING US producing trends he analized…despite any claims that he predicted future production rates from other trends. And if one looks at where those trends are today he was right on the money. He did not offer a model of future US oil production rate. He put forward a model of the future production from those trends that comprised his statistics.

Again, not taking away anything from the man, but who here would like to draw a graph of future Bakken or Eagle Ford Shale production? It really wouldn’t be that difficult…if you wait until most of the wells had been drilled and 70% of their URR has already been produced. Which is pretty much what Hubbert did. If Hubbert had tried to make his prediction 20 to 30 years earlier I doubt he would have been close. Just as it would have been difficult for someone predicting future oil production from the shales a dozen years ago when oil was selling for 1/3 of today’s price.

Jerry McManus on Thu, 6th Mar 2014 9:33 pm

Again, I agree with Rockman. How many times do we have to repeat before people get it?

No predictions. No obsession with the “symmetrical” shape of curves. No “analysis” of the global economy, of climate change, of nuclear war, of asteroid strikes, or who will win “American Idol”

Just a simple observation that when the production curve crosses the discovery curve you know enough about a mature producing region to make a pretty good guess about when the production curve will peak, all else being equal in a perfect world.

C’mon people, it really could not be any simpler.

MSN fanboy on Fri, 7th Mar 2014 12:28 am

People really should stop making predictions…

So here is mine… We all going to die.

But seriously no more. We know what is coming (against a back drop of a great many who don’t) and should consider ourselves lucky we are able to understand sites such as these.

Just be happy 🙂 You and I are privileged to watch a ‘superior’ species (lol) crash and burn from our retreats.

Davey on Fri, 7th Mar 2014 12:55 am

Msn, eventually you work your way up the ladder but there is no safety at the top just occasional piece of mind. This piece of mind is acceptance. In any case death will visit regardless of what happens outside. It is happening slowly with my mind and body. My youth is gone! What I can’t get over and may never is the thought of my 6 1/2 year old boys suffering or dying. That is what keeps me vigilant and prepared.

Makati1 on Fri, 7th Mar 2014 1:29 am

Back and forth we go … and no one still knows what tomorrow will bring.

@NWR, You are correct. The curve did NOT take into account finances or climate. Both are now about to take down the whole shooting match, perhaps overnight and without warning.

There are more and more articles about petro corporations investing less and less and selling off assets to pay off investors so they will not abandon the sinking petrocarbon ship and to convince new investors that they can still get rich if they just send their retirement money to the appropriate company.

Sorry! If I had a thousand to throw away, I would go to the casino here and at least get a nice evening’s enjoyment for my money. Anyone in the stock market must have ulcers by now with the huge bubble on Wall Street getting closer and closer to the pin. About like 1929 only there will be no recovery on the other side.

Hubble warned us.

President Carter warned us.

Rachel Carson warned us.

Many others warned us, but we decided to party on, assured by the wealthy elite’s propaganda that all will be well and we will have a perfect future if only we keep consuming wildly.

And … here we are…

dashster on Fri, 7th Mar 2014 1:37 am

“But he was also affected by his personal bias. He was a Malthusian.”

What are you if you are not a Malthusian? Infinitarian? Or is Cornucopian also used for someone who doesn’t believe in limits to population growth?

Nony on Fri, 7th Mar 2014 1:42 am

https://www.youtube.com/watch?v=m5LX16zia2k

GregT on Fri, 7th Mar 2014 6:34 am

“What are you if you are not a Malthusian? Infinitarian? Or is Cornucopian also used for someone who doesn’t believe in limits to population growth?”

Captain of the Starship Enterprise?

“Beam me up Scotty, there’s no intelligent life on this planet.”

GregT on Fri, 7th Mar 2014 7:12 am

“Our projections put transportation fuels at about $10/gal by 2025. At $10/gallon world trade will slow to a trickle of its present amount.”

A trickle? More like a dribble. The world’s economies will have collapsed long before then, and the cities will have long since exploded into violence and chaos. Food would be unaffordable for most. One in six Americans are already on food stamps.

ulenspiegel on Fri, 7th Mar 2014 10:39 am

A good discussion on Hubbert and the misinterpretzation of his work is found on Tad Patzek’s blog “LifeItself”.

However, as economist, and here I would include the author of this article, you need a thick skin. 🙂

rockman on Fri, 7th Mar 2014 12:31 pm

U – I was not aware of Patzek…thanks. He does have a rather sarcastic tone which, of course, immediately endeared him to me. As you say he goes into great detail about those misinterpretations. But he did remind me of a point I had forgotten about: timing of global peak. While he may have been off by a factor of two regarding the daily oil production rate (thanks to all those trends he did not know would develop) Hubbert’s timing of global production plateau seems amazingly accurate. But, to be painfully honest, I’m not sure that was brilliance or just luck on his part. No doubt Dr. H was very clever but still the lack of knowledge of future oil trends that made his daily production level inaccurately should have done so for the timing.

Of course we need to run the numbers another 20+ years to see if this plateau holds. My guess it will since it would take a significant jump in inflation adjusted oil prices to create another big ramp up in production. A price increase the global economies have already clearly signaled would bring about another global recession which would drive down consumption and prices.

Davy, Hermann, MO on Fri, 7th Mar 2014 12:51 pm

Rock said – Of course we need to run the numbers another 20+ years to see if this plateau holds. My guess it will since it would take a significant jump in inflation adjusted oil prices to create another big ramp up in production. A price increase the global economies have already clearly signaled would bring about another global recession which would drive down consumption and prices.

Rock, I think it is entirely possible to maintain a plateau but a plateau will not be enough to maintain a growing economy so the results will be a further stressed global financial system. The financial system is the key to the above ground variable with oil production dynamics. My bet is the system will hold a few more years but that is it. There are so many minefields the market must navigate. The biggest is the bubble inflation itself. Look over these bubble indications. Bubbles don’t last!

1. Debt is cheap. 2. Debt is plentiful. 3. There is the egregious use of debt. 4. A new marginal (and sizeable) buyer of an asset class appears. 5. After a sustained advance in an asset class’s price, the prior four factors lead to new-era thinking that cycles have been eradicated/eliminated and that a long boom in value lies ahead. 6. The distance of valuations from earnings is directly proportional to the degree of bubbliness. 7. The newer the valuation methodology in vogue the greater the degree of bubbliness. 8. Bad valuation methodologies drive out good valuation methodologies. 9. When everyone thinks central bankers, money managers, corporate managers, politicians or any other group are the smartest guys in the room, you are in a bubble. 10. Rapid growth of a new financial product that is not understood. (e.g., derivatives, what Warren Buffett termed “financial weapons of mass destruction”).

shortonoil on Fri, 7th Mar 2014 2:12 pm

“Rock said – Of course we need to run the numbers another 20+ years to see if this plateau holds.”

We hardly need 20 years to get a very good picture of what’s happening. 60% of the world’s petroleum production comes from 1% of its fields, and those fields now average more than 60 years in age. Shale, in over 30 years of massive investment, still accounts for less than 2% of the world’s petroleum production. Its growth rate is less than half the decline rate taking place in the major fields. The shale industry is now spending $1.50 in drilling costs to produce $1 in product. Shale is nothing more than lip stick on the depletion pig. Waiting around to see if the pig changes the color of its lip stick is not much of a Plan B.

Robelius, and many others have predicted that the giants will be coming off their plateau later on this decade. Our studies strongly support that appraisal. Conventional crude has powered world economic growth for the last century (see graph# 25 at our site), it has set average world energy prices, and it is (so far) an irreplaceable fuel for powering the world’s transportation fleet. Modern civilization as we know it, would not exist without conventional crude.

The simple fact is that the world’s petroleum reserve is now in an advanced stage of depletion; every quantitative and qualitative indicator available to us supports that determination. Whether or not our civilization will continue to exit for much longer, in any recognizable form, is now in serious doubt!

http://www.thehillsgroup.org/

rockman on Fri, 7th Mar 2014 4:41 pm

Davy – I fully agree. The plateau picture isn’t the entire story. As pointed out before it isn’t important to the global consumers of oil how much is produced but how much they can purchase and at what price. The important (though very difficult chart to create) in the future import curve for each country. Consider that US imports are not on a plateau. But why is easy to explain by increased domestic production. But that’s only part of the reason: we’ve also reduced consumption from 21.5 million bopd.

And yes: one can debate the positive and negative aspects of that change. Conservation: good if done for the environment…bad if a result increased inability to afford that oil. But however one wishes to rate it the US is not on an oil import or consumption plateau. So as ELM and Chindia consumption increases there will be less oil available for the rest of the consumers to acquire. And that curve will have a far greater effect on the US economy than the current global production curve plateau IMHO.

And that’s what we really care about and not how much oil Saudi Arabia will be producing in the future.

Northwest Resident on Fri, 7th Mar 2014 5:21 pm

rockman — There was an article posted here not long ago that made the point that with projected population growth and increased requirements for oil production, we would need an additional 55 million bpd by 2025. I did some complicated math and realized that in the next ten years, that means we will have to increase worldwide oil production by 5.5 bpd each year. Do you see that as being realistic?

shortonoil on Fri, 7th Mar 2014 7:31 pm

“I did some complicated math and realized that in the next ten years, that means we will have to increase worldwide oil production by 5.5 bpd each year. Do you see that as being realistic?”

NonOpec production peaked several years ago, and eight of Opec’s members have peaked. The rest are keeping production stable through massive in-fill drilling programs. McKenzie county is the only area in the Bakken that is showing any increase, and their wells are now over 11,000 feet deep and increasing as they follow the oil seam Southwest. Shale oil in this country will probably peak within a year of two.

500 extra barrels extra may be hard to come by with conventional crude world wide in decline by about 5% annually. With China and India’s economies contracting rapidly (there was another major corporate bond default in China today) their demand will probably fall next year. We probably won’t see shortages, just increasing price as production costs only have one direction to go.