Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on June 10, 2012

Tech Talk – Saudi Arabia and Natural Gas Liquids

The price of crude oil has been shown to have significant impact on the global economy, and in the current somewhat fragile state of the various parts of that economy the current lower prices help. Yet Stuart Staniford has commented that, given the Saudi need for income to hold off “Arab Spring” dissatisfaction, they are unlikely to let prices fall too far, before cutting production, since even a 10% reduction in output could raise prices 20%, thereby resolving their future income concerns. This well reflects the role of the Texas Railroad Commission back when it controlled US production in order to sustain an acceptable price for oil. But that role collapsed when overall US production was no longer able to spring to the rescue when demand rose, and US production could not, passing the control over prices to OPEC and more particularly the Kingdom of Saudi Arabia (KSA) who could, and have shown a willingness to, control output to ensure that it proximately followed demand and has kept prices within an acceptable range, for them. Their recent increase in production to offset possible Iranian sanctions, however, is likely to be transient, since – apart from annoying Iran, it has also driven prices below that benchmark.

It is relatively easy to return to a more acceptable price by curtailing production, and as Stuart noted, this can increase KSA revenue at a time of falling global demand. However, in the opposing case, where the global economy requires a “reasonable” price for oil, and will require them to increase production on a sustained basis, as they have done, transiently, to the limits of demand growth in the past year, that ability may be limited and of a shorter duration. It also occurs at a time that the internal use of crude is limiting the amount that the KSA can export. But while there is considerable discussion about this situation, there has been some increase in natural gas liquid production that is also important, and thus a main point of this post.

The increased production at Shaybah, however, also helps identify an additional source of increased production, since it is also increasing natural gas production to 2.4 bcf/day, with a concomitant production of 264 kbd of NGL. The increase in overall production of NGL from OPEC has, for some time, provided a significant volume of additional fuel. By the last quarter of 2011 OPEC as a whole was producing 5.42 mbd of NGL and NCF (non-conventional fuel), (up from 3.89 mbd in 2006)

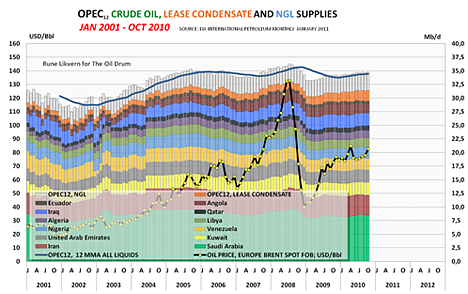

Rune has written about NGL production here and here with the relative importance of this supply perhaps best illustrated with this graph from the latter post.

There is also the development of the Karan field that will, with the other programs in development, collectively raise KSA natural gas production to 15.5 bcf/day from the 10.2 bcf/d it was achieving in 2010. Unfortunately the high sulfur content of the gas to be fed to Wasit is causing some problems and that project completion may now be delayed until 2015, though the problem (of sulfur freezing in the lines) is not yet solved.

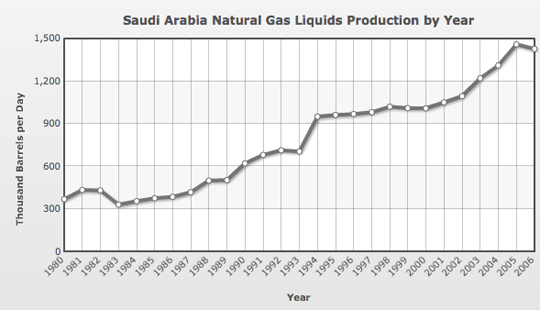

Saudi production of NGL’s has steadily grown over the years.

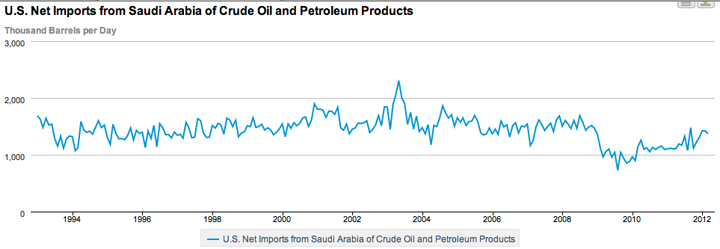

It should be also be noted that, following the drop in consumption caused by the recession, the United States has increased the amount of crude that it is importing from KSA over the last couple of years.

The Saudi market for NGL lies largely in Asia, with an export terminal at Yanbu. The terminal is connected to Abqaiq through a 1,170 km pipeline, and can handle exports of up to 2 mbd of NGL.

2 Comments on "Tech Talk – Saudi Arabia and Natural Gas Liquids"

BillT on Mon, 11th Jun 2012 2:37 am

Lots of chickens being counted here, and the eggs haven’t even been laid. lol

SOS on Tue, 12th Jun 2012 12:54 am

The indicated production areas in the USA are too small. The area in North Dakota is both gas and oil. Every county except one in North Dakota has proven commercial (economic to recover) reserves of natural gas.